I’ve often pondered the continuing headlines over the lack of progress in the area of mathematics in the United States relative to our peers and think the issue may lie in one area. The rest of the world has adopted the metric system, while we are only peripherally aware of it. As such, when standardized scores are compared, maybe translating from the metric system is needed and we may score higher. Though said in jest, we are fixated on numbers and the dissection of them (of which I am to blame and apologize henceforth). Last week brought about a barrage of key economic data that had the markets on “DEFCON 4” (assuming “DEFCON 5” meets the Fed’s concern of investor apathy that it almost single handedly created) after recent geopolitical events in Ukraine and Israel. This only amplified with Argentina’s roughly five-year cycle of habitual default (see 2005 and 2010).

In the last week we saw U.S. GDP’s second quarter beta release come out at a robust 4.0% with expectations of 3.0%. Though a large headline number, everyone who didn’t have a political agenda was aware that a large chunk of this was making up for a weather-induced slowdown from the first quarter which was revised upward from a -2.9% to a -2.1%. So, the more lucid investor might take the longer view to see how both exacerbated measures looked on a longer term and one finds the 2.40% year-over-year change is right at the 20-year average of 2.50%.

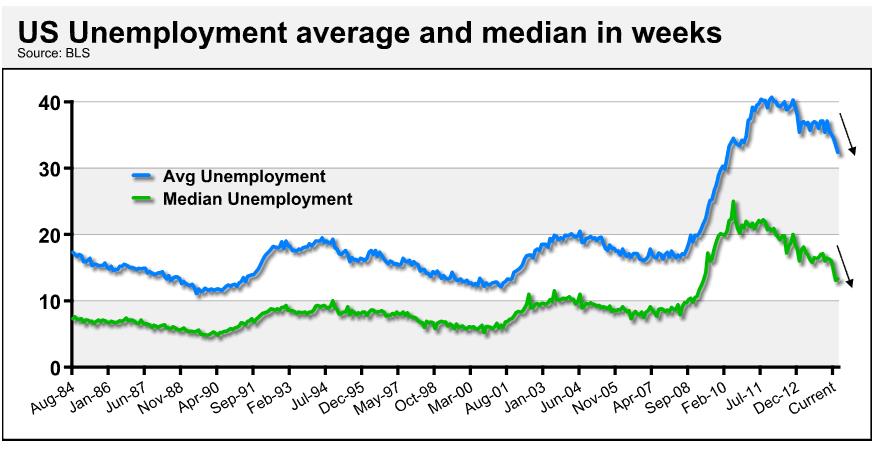

We then had the next big thing which was the unemployment report from July. Again, the beta release showed continued growth, albeit not as shocking as GDP. The headline numbers and the multitude of headlines all worked out to be close to in line and revisions were nothing to fret or cheer about. There was one particular undercurrent that needed a bit more analysis than given and is beginning to detail the precipice we find ourselves at with employment headline numbers actually beginning to show a declining slack that has hung over the validity from the numbers. Below is the average duration and median duration in weeks for the unemployed in the United States. At its peak, the average number stood three standard deviations wide – an event that occurs only 0.3% of the time. Recent declines should not be discounted nor should they be interpreted that the slack is gone and wage pressure is eminent. Wages growing at 2.0% are okay, but still well below what the Federal Reserve would classify as troubling for a cyclical inflationary movement.

To sum up, the economy keeps chugging along and the employment number continues to suggest marginal wage pressure which propels the Federal Reserve to maintain their trajectory with ending quantitative easing and ultimately raising interest rates.

The earnings situation through August 1, 2014 continues to point to an improving outlook for equities even in light of the rise so far in the indexes and recent sell off. According to Fact Set, with 75% of the S&P 500 reporting so far for second quarter 2014:

- 74% have reported earnings above estimate; the four-year average is 72%

- 65% have reported revenue above estimate; the four-year average is 57%

- A ratio of 2.3 companies has reported negative EPS (earnings per share) guidance versus positive guidance. The 10-year average number is 2.61, so slightly better than the historic average, according to Morgan Stanley.

While the revenue and earnings-per-share estimates are rising steadily, the amount of stock reduced by buybacks continues. In fact, the interesting component of nearly 1% of stock outstanding being removed quarterly due to stock buybacks (according to Insider Score), the clamoring from fund managers for increased CapEx spending is at all-time highs. Nearly 65% of fund managers surveyed for the Merrill Lynch Global Fund Manager Survey which not only is an all-time high since 2002, it is four times more important than the next most favored action by companies in returning cash to shareholders.

While we continue to become numb to an onslaught of numbers being released, taking a slight pause to weigh the multitude of small incremental gains continues to point to higher asset prices, improvements in the economy and a Federal Reserve pushing toward normalizing the system with higher rates.

CRN: 2014-0801-4343R

This commentary is for informational purposes only. All investments are subject to risk and past performance is no guarantee of future results. Please see the disclosures webpage for additional risk information.