After months of record low volatility and little directional bias in price, fixed income markets were finally awoken from their summer doldrums, driven by a string of robust economic data. Not to be outdone, equity markets sold off sharply on the data, with the DJIA recording a 317 point drop on Thursday, its largest such decline since March. The Federal Reserve has long articulated to the markets that monetary policy is tied to the data. With quantitative easing (QE) set to end in October, a little data-driven volatility should be welcome to most market participants—likely more so for fixed income markets. With the high yield and equity markets recording poor absolute returns in July, markets appear to be in the early stages of testing the pricing and valuation of risk assets. Rising volatility and policy uncertainty are clearly themes on investors’ agenda for the balance of 2014.

Of particular importance last week was the conclusion of the FOMC’s two day policy meeting, acknowledging a rebound in the economy during the second quarter and inflation closer to their 2% target. In contrast to recent language, the FOMC specifically stated “the likelihood of inflation running persistently below 2% has diminished somewhat.” Committee member Charles Plosser, a noted policy “hawk”, was the lone dissenter on the Fed’s position on forward guidance, feeling the timing of the first rate hike should be related to data and not some “predetermined time” after QE has ended. Coupled with Dallas Fed President Richard Fisher’s recent rhetoric, the hawks on the FOMC are becoming a little bolder. The Fed will meet next in September.

Friday’s jobs report—despite recording a rise of +209k jobs—was only mildly supportive of economic growth. With GDP growing at a mere 1% rate in the first half of 2014, the economy will require a healthy and vibrant consumer to be self-sustaining. Income and spending data depict a clear picture of a consumer, who—when factoring in inflation over the last year—has realized 0% wage growth in real terms.

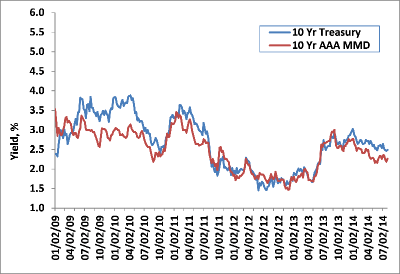

Weekly Change: 10Y Treasury Yields vs. 10Y AAA MMD

Source: Bloomberg, Thomson Reuters and Castleton Partners

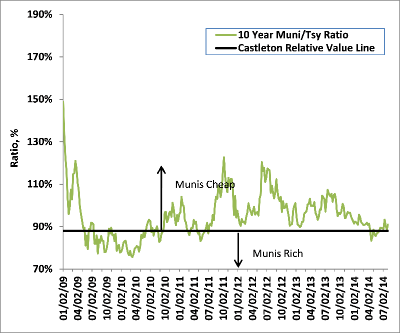

Ratio of 10Y Municipal Yield to 10Y Treasury Yield

Source: Bloomberg, Thomson Reuters and Castleton Partners

Tax-Exempt

Despite a mild sell-off in muni yields last week, July was yet again another positive month for the asset class, extending its best yearly start since 2009. With gains of +6.18% (per Barclays) so far in 2014, tax exempts remain the top performing sector in US fixed income—besting treasuries, agencies, corporates, mortgages, and high yield. Owing to the superior tax adjusted yields, increased demand and net negative supply, we suspect August will be another favorable month for tax exempt investors. Simply put, we remain constructive on both absolute and relative value in muni land.

On the week, five year, ten year and thirty year tax free yields rose by 4, 8, and 15 basis points respectively—a rare steepening of the yield curve. With ten year benchmark yields now at 2.27%, the Muni/ Treasury ratio now rests at 90%. With a yield of just 1.23% in five years, and a ratio relative to Treasuries at 70%, we continue to favor intermediate municipals over bonds in the 2-5 year range. The first week of August will be much like the preceding 31 weeks—namely, limited supply, with just over $5 billion expected to price. The largest is a $575 million loan for the University of Chicago (Aa2/AA).

As for Puerto Rico, all eyes continue to focus on the power authority (PREPA) and its ongoing liquidity concerns. Facing a July 31st deadline with Citibank over a $146 million expiring line of credit, PREPA was able to receive a two week extension, until August 14th. PREPA has another $500 million outstanding line with Scotiabank, which is set to expire on the same date. Per a recent report from noted municipal utility analyst Gary Krellenstein, PREPA spends nearly 63% of its operating and maintenance budget on fuel costs, versus an average rate of 23% for utilities on the mainland. Despite over $8 billion of debt outstanding, the reliance on oil to generate electricity—and the failure to convert to natural gas or other means—has been the single biggest contributor to PREPA’s rapidly declining balance sheet.

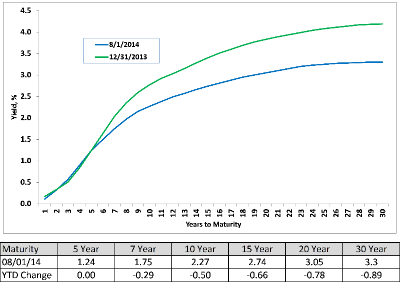

AAA Municipal Market Data (MMD) Yield Curve

Source: Thomson Reuters

Weekly Municipal Mutual Fund Flow Data

Source: Lipper AMG Data

Taxable

Investment grade spreads recorded their worst week of July, widening 5-7 basis points. The energy sector was the worst performer. For the month, high grade corporate debt returned -0.06% (Barclays), making July the first negative total return month of 2014. With the taxable high yield sector off -1.33% in July (Barclays) and the S&P Index also negative (-1.55%), one can say performance was fairly resilient in spite of the recent widening in spreads and “risk off” sentiment. With spreads at historically tight levels relative to Treasuries—and minuscule absolute yields—we have long viewed the asset class susceptible to underperformance in any material interest rate sell off.

With volatility and geopolitical risk noticeably rising last week, it was not surprising to see a sharp drop in supply. Only $7 billion of new debt was priced; the lowest supply week of 2014. Fund flows into investment grade funds remained positive at +$952 million, versus the prior week’s +$1.7 billion figure. Of note, taxable high yield funds recorded net withdrawals of -$1.5 billion—the largest such level so far this year, extending a three week trend.

© 2014 Castleton Partners, LLC. All rights reserved.

THE FOLLOWING NOTES AND DISCLOSURES ARE AN INTEGRAL PART OF THIS REPORT: Past performance is not a guarantee of future results. Different investments involve varying degrees of risk, including the risk of illiquidity and the risk that you could lose part or all of your investment. There can be no assurance that the future performance of any specific investment, investment strategy, or product (including those discussed herein or recommended or undertaken by Castleton Partners, LLC) will be profitable, equal any corresponding indicated historical performance, be suitable for your portfolio or individual situation, or prove successful. Charts, graphs and indices are included herein only for reference and do not constitute forecasts of the past or predicted future performance of any investment. Indices are not investments. Due to changing market conditions and other factors the content herein may no longer reflect Castleton Partners, LLC’s current opinions or positions. Nothing discussed herein is or is intended as tax, legal, accounting or personalized investment advice from Castleton Partners, LLC. Should you have any questions regarding the applicability of any specific issue discussed herein we encourage you to consult competent advisers of your choosing. Nothing herein is or is intended as an offer to sell or a solicitation of offers to buy any security. Castleton Partners, LLC’s current written disclosure statement including discussion of our advisory services and fees is available upon request.