Dynamic and Durable Growth Part 2: The Enormous Implications of Shale Energy

This is the second in a four-part series examining dynamic and durable growth themes that affect the US economy and may present opportunities for investors. The first post explored the biotech revolution, and the third and fourth posts will discuss the massive changes in mobility.

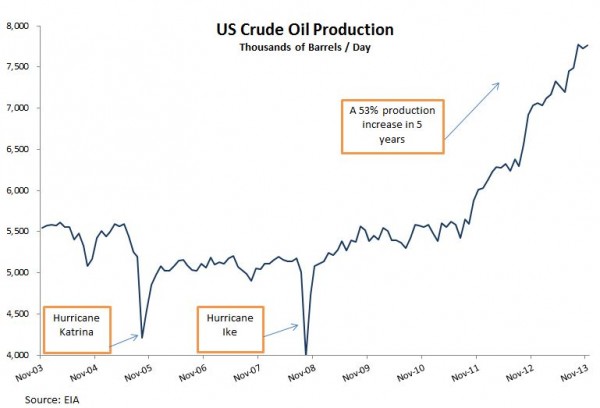

With the shale boom now the largest driver of US economic growth, investors will likely remember the period from 2010 to 2014 as the beginning of the shale revolution that enabled the US to increase oil production by 50%,1 decrease OPEC imports by one-third2 and become more energy independent.

And that’s just the beginning.

Fracking and other innovations

This energy cycle started, like all others, with engineering and innovation. When Howard Hughes introduced a new type of drill bit in 1908, it transformed oil exploration. Wildcatters and oil companies used his innovation to drill deeper to find oil for the next four decades.

Similarly, several technologies have come together to spark the current revolution. Hydraulic fracturing, a process that fractures underground rock formations to release the oil and gas trapped inside, has made horizontal drilling not only viable, but also very prolific. The number of horizontal rigs drilling in the US has increased to 1,250 from only 48 in 2000.3 In addition, adoption of “pad drilling” has reduced drilling times and made rigs much more efficient by strategically placing multiple wells within a single drill site, or pad.

US Shale Boom

Shale boom impacts

These innovations have already led to a land grab for leases by exploration and production (E&P) companies and a massive increase in capital spending using this new technology. In our view, however, the shale revolution has enormous implications for the US for years to come, including a reduction in the budget deficit that we’ve already seen. But more significant is that lower consumer and business costs are increasing job growth, both directly and indirectly. For example:

- The US is developing a global advantage in natural gas — 20 years ago US supply was estimated at 70 years, but today supply estimates have grown to nearly a century. This bounty can serve as a power source, as well as a cheap input for industrial manufacturing and chemical commodities.

- The boom in fracking has given the US a sustainable price advantage in producing petrochemical feedstocks used in manufacturing plastics and petrochemicals. These feedstocks from natural gas liquids are cheap relative to more expensive oil-based feedstocks elsewhere, and the reduced cost for US manufacturers is having a profound impact on the chemical industry globally.

- More jobs in the oil- and gas-producing states will potentially lead to higher retail sales, housing turnover and state revenue.

- Infrastructure development to capture, transport and harness our new energy resources is just beginning, but it is already creating a significant number of jobs in the US as we build pipelines, trucking and rail cars to support this energy boom.

- Cheaper energy costs — combined with higher labor costs in Asia — are encouraging companies to relocate back to the US.

Implications for investors

We believe this time of tremendous change offers opportunity for investors. A few observations:

- Keep in mind that the new technology behind the boom has been used primarily in the US so far. As other regions begin taking advantage of these advances, certain service providers may offer attractive opportunities.

- Because the land grab in the US is largely over, E&P companies need to be more selective and focused on returns. Companies in the largest and cheapest oil shale plays will have the advantage.

- The profits of refiners, chemical manufacturers and some industrial companies have soared over the last two years because of cheap feedstocks and the ability to sell their products globally at very competitive prices. As these companies — and their competitors — build more chemical plants and refineries to take advantage of their outsized profits, engineering and construction firms will benefit. In our view, this coming construction wave may be much larger than investors and Wall Street anticipate — the market has yet to recognize the potential scale of this opportunity.

The direct and indirect effects of the shale boom have far-reaching implications for the US and global economies. For that reason, we believe it’s an exciting time for growth investors.

To find out more, watch this video on shale energy from the Invesco US Growth team.

1 Source: US Department of Energy

2 Source: BP Statistical Study, 2013

3 Source: US Department of Energy

Important information

Businesses in the energy sector may be adversely affected by foreign, federal or state regulations governing energy production, distribution and sale as well as supply-and-demand for energy resources. Short-term fluctuations in energy prices may cause price fluctuations in an energy fund’s shares.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. The opinions expressed are those of the author(s), are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is a US distributor for retail mutual funds, exchange-traded funds, institutional money market funds and unit investment trusts.

Invesco unit investment trusts are distributed by the sponsor, Invesco Capital Markets, Inc. and broker dealers including Invesco Distributors, Inc. These Invesco entities are indirect, wholly owned subsidiaries of Invesco Ltd.

©2014 Invesco Ltd. All rights reserved.