Which Denomination of Gold is Your Parachute?

Treesdale Partners, portfolio manager of the AdvisorShares Gartman Gold/Euro ETF (GEUR), AdvisorShares Gartman Gold/British Pound ETF (GGBP), AdvisorShares Gartman Gold/Yen ETF (GYEN) and AdvisorShares International Gold ETF (GLDE), share their thoughts about the gold space.

We continue on the theme of gold as a defensive asset in this week’s discussion by examining the performance of gold priced in dollars (USD), European euro, British pound and Japanese yen through a number of different periods which were characterized by a sudden rise in investor risk aversion.

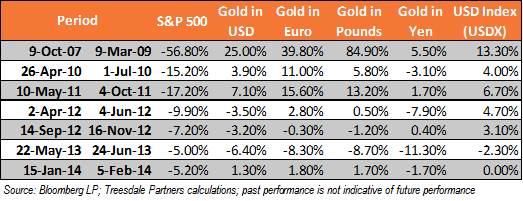

In the current environment with gold showing some signs of increased sensitivity to the news flow, in particular the geopolitical events in Gaza and Ukraine, it is timely to look at the performance of gold priced in the most liquid currencies during periods in which a news event causes a sharp, negative reaction in the markets. For the purposes of the discussion we define a “rise in risk aversion” simply as any period from and including the 2007 credit crisis in which there was a peak-to-trough fall of 5% or more in the S&P 500 index. The results are presented in the table above.

There are two main patterns that we observe. Firstly, in every period other than the May-June 2013 period, gold priced in euro and gold priced in pounds outperformed gold priced in dollars. This was likely driven by the fact that the US dollar showed broad based strength. When an investor buys gold priced in dollars they are expressing the view that they expect the price of gold to increase relative to the dollar - the investor is said to be long gold / short dollar. Therefore when the dollar shows strength on currency markets the price of gold in dollars would be expected to show weakness. In contrast gold priced in euro and gold priced in pounds avoid dollar exposure and were less impacted by dollar strength during the stress period. Historically the dollar has been viewed by investors as a “defensive currency” and during periods of high volatility, they have tended to move assets into dollars thereby pushing up the value of the dollar. In the last column in the table a measure of the value of the dollar is shown using the Intercontinental Exchange Trade Weighted Dollar Index (USDX) as a proxy. As expected, in every period other than May-June 2013 the dollar as measured by USDX strengthened. Conversely in the period in which the dollar was weak we see that the gold price in dollars outperformed the other currencies.

The second main pattern that can be observed is that gold priced in yen terms has tended to underperform versus gold priced in all the other currencies, during the stress periods. The reason is similar to why gold priced in dollars underperformed. Historically the yen has also been viewed by investors as a defensive currency. When an investor buys gold priced in yen they are expressing the view that they expect the price of gold to increase relative to the yen - the investor is said to be long gold / short yen. Therefore when the yen has shown strength on currency markets the price of gold in yen has also tended to show weakness. To sum it all up, historically gold priced in euro, in an environment in which the dollar is strengthening, has had the most positive reaction to negative market news.