Summary

Bond Investors have had a great run so far in 2014. It's time to take some profit.

Inflation expectations are rising, should we be worried?

Why has the Japanese Yen been strengthening against the USD?

Take Profits on Bonds

Most bond investors have had a surprisingly good year so far. Yields have fallen across the board in the U.S., most of Europe including the peripheral markets of Spain, Italy and Greece and even in Japan. Sector performance has been equally impressive. Broad market indices are up (ETF AGG +2.74% YTD) with long duration products boasting of double digit returns after just seven months. Vanguard's Extended Duration Treasury (ETF EDV) is up close to 15%. Corporate bonds, High Yield, U.S. Agency and MBS, Tax Exempt and Global Government Bonds, including emerging markets all have positive YTD total returns. None of this was supposed to happen. Of course, not much of whatever is supposed to happen in the markets, actually happens, or at least not during the period you are expecting it to happen. That's why successful investing is so difficult. It almost requires one to be a constant contrarian, at least as it concerns following so called expert advice, and at the same time, huddling with the momentum, growth or value crowd.

There are competing theories on why bond yields are so low:

- Yields reflect future growth prospects and in this regard, future GDP growth will be anaemic

- An aging populations in advanced nations are naturally inclined to favour bonds

- We are in the midst of a vicious circle where the "search for yield" actually forces rates lower across most fixed income sectors

- Inflation expectations are well contained or maybe low yields are signalling an upcoming deflationary environment

- Bonds are benefiting from a quiet, yet strong safe haven demand, as geopolitical risks rise

- Bonds of advanced economies are aggressively accumulated by mercantilist nations such as China and Japan eager to keep their currencies undervalued

- Global Central Banks have artificially manipulated rates lower

- Global Bank Regulators have forced financial institutions to hold outsized bonds positions in a liquidity portfolio, driving yields lower

Just about everyone can agree with or take exception to every factor listed above. The point is that the magnitude or force and direction of each factor can suddenly change. Please note that not a single factor that we have listed above is "data dependent" and none are directly observable. That means an investor is obligated to heavily rely on heuristics when thinking about analysing interest rates. Here at CGA, we have had a good run with bonds so far in 2014 and we are not tempted to get greedy. We use U.S. 10y Notes as our signal to initiate changes in our overall allocation to bonds. Between 2.40% and 2.50% we lighten up. Between 2.85% to 3.00% we reload. It is time to lighten up. What do we do with the cash? Move some of it into (ETF SPY), which at a current P/E of 19.6, offers an earnings yield of about 5%.

Rising Inflation Expectations

Using U.S.Treasury Inflation Protected Securities (ETF: TIP) to extract inflation signals is notoriously difficult. Briefly, the TIPS market is not all that liquid and their prices reflect various risk premiums, such as a liquidity premium, in addition to information about future inflation. The Chart below shows that inflation expectations, as measured by the FEDs, preferred measure 5y5y forward breakeven rate (now 2.61%) looks to have meaningfully broken above the 2.40% -2.50% range that has held since earlier this year. Sure this gauge of inflation expectations has been as high as 2.80% as recently as December 2014. However, the U.S. unemployment rate was 6.7% back then and now it's just 6.1%. Plus risk markets are higher across the board. So the FED has to take notice.

Granted the data is noisy as Ms. Yellen famously has pointed out. But broader measures of inflation in the real economy are all up as well. The CRB Index is about 7% since the start of the year, although it has recently fallen due to dramatic decline in oil prices. The JOC-ECRI Index of industrial prices is up close to 6% year over year. To be clear, we do not see an inflation scare. In fact, longer term, the forces of deflation are more powerful than inflation in our view. However, it would be breathtakingly naïve on our part to ignore the threat that rates may be headed higher, at least near term.

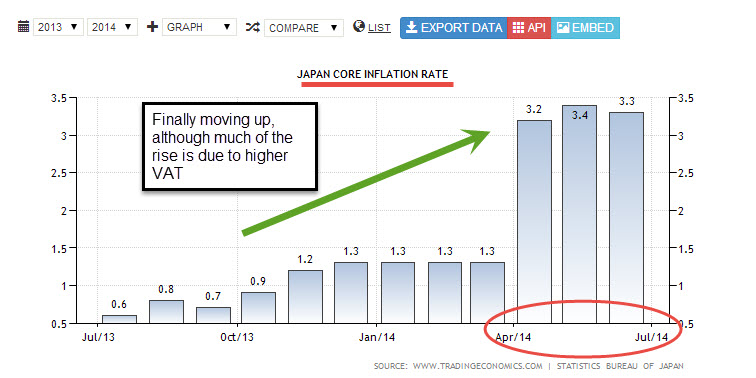

The Japanese Yen

The Japanese Yen has strengthened about 3.50% against the USD so far this year. Meanwhile Nikkei tracking funds (ETF EWJ) are flat for the year. This is not surprising given that the Yen depreciated against the dollar by 17.65% last year and the Nikkei Stock Index was up a whopping 57%. This year, Japan is starting to finally see headline price indices rise after years of near zero or negative readings. Shouldn't a rising Consumer Price Index in Japan, relative to the CPI registered in the U.S. weaken the Yen? Apparently not. Are not Japanese Government Bonds (JGBS) supposed to react negatively to a rise in actual inflation? Apparently not either. JGBs are as steady as a rock and the 10y yield has actually dropped by 21 basis points so far this year. So what's going on?

We don't really know to be completely frank. What we do know is that a strengthening Yen can at times herald a very rough road ahead for global risky assets. We also know for sure that the Japanese stock market will not rise if the yen continues to strengthen. Japanese bonds certainly will not sell off. A few years ago, the Yen used to be the funding currency choice leading to the infamous carry trade. Now just about every currency in advanced countries is funding currency due to abnormally low borrowing costs. So the damage or fallout from a rising Yen may not hit risky assets in the same manner as in the past. But it may. Watch the JPY/USD cross rate. A break below 100 may signal that Japan's most recent attempt at reflation is a failure. That is definitely not good for any risky assets.

Conclusion

Bond investors have had a good run in 2014 and should take some profit and reduce exposure. Inflation expectations and actual inflation readings are beginning to rise and will definitely be noticed by the FOMC. The Bank of England is hinting at an early rate rise. The BOE is widely considered an early mover- both at cutting and raising interest rates. Lastly, the Japanese Yen has been strengthening recently, which historically has meant some bad news for risky assets. We follow a host of Metrics That Matter on our Website, which is updated weekly.

Best regards and please share this mail with colleagues and friends.

Edward Talisse

Copyright 2014. Chelsea Global Advisors. All Rights Reserved

The author is solely responsible for the content of this mail- not any current or former organization or employer that the author belongs to. Any content posted in this mail or on the website is solely intended to provide general information, observations and ideas rather than specific advice. All the views here are solely the expression and opinions and personal experiences of the writer. This mail and the website are updated regularly and any information contained herein should be considered dynamic rather than static. Hence the content changes over time as the topics change. The information published herein might not be valid or accurate two weeks or two years from now. Content, sources, information and links change over time, and therefore, the writer makes no claims of accuracy of such information as the mails and website and its content evolves over time.