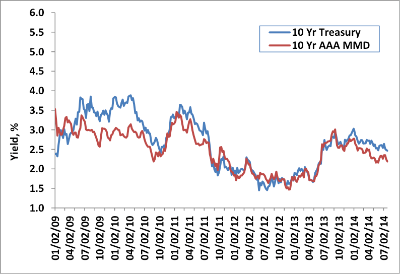

Increasing geopolitical tensions, mixed economic data, low volatility, and little directional bias in interest rates; sound familiar? Last week produced more of the same in fixed income, as prices across the entire maturity spectrum remain in a well-defined (and very narrow) trading range. With a yield of 2.48%, the ten year US Treasury note has been oscillating within a twenty basis point band since May 1st: 2.65%- 2.45%.

Perhaps this week can finally generate some excitement in fixed income, as we are expecting a full slate of economic data, supply, and a two day meeting of the Federal Reserve Open Market Committee (FOMC). As for the FOMC, many members have voiced concern of late for the widespread complacency that exists across all asset classes—despite it being largely of the FOMC’s doing. Investors are anxious to see if this week’s meeting heats up the debate among committee members over the eventual increasing of short interest rates. Castleton is of the view, however, that Fed Chair Yellen will do little to rock the boat during the depths of summer. We view the annual Kansas City Fed conference in Jackson Hole next month as a more likely time period to reveal any future directional bias in monetary policy.

As for the data, we get our first glimpse at second quarter GDP on Wednesday, followed by the June payrolls report on Friday. Expectations are for growth to rebound to around +3%, with another 230,000 jobs added.

Weekly Change: 10Y Treasury Yields vs. 10Y AAA MMD

Source: Bloomberg, Thomson Reuters and Castleton Partners

Ratio of 10Y Muni Yield to 10Y Treasury Yield

Source: Bloomberg, Thomson Reuters and Castleton Partners

Tax-Exempt

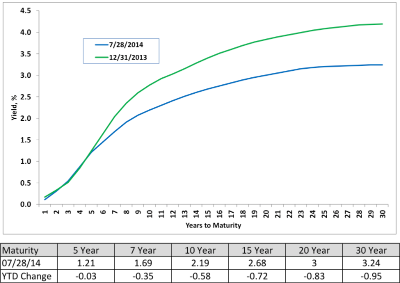

Much like taxable markets, the song remains the same in municipals. Last week was yet another characterized by low supply and strong fund flows. Over the course of the week, intermediate and long-dated tax exempts continued to grind higher in price, outperforming taxables, as the favorable technical backdrop supporting the market shows no signs of abating. Municipals now rest at levels last seen in May 2013, with 10y yields registering their best consecutive two week yield drop since January (-16bp). Benchmark ten and thirty year tax exempt yields now rest at 2.19% and 3.24%, a decline of 4 and 5 basis points respectively. The ten year Muni/ Treasury ratio now stands at 88%.

Despite ongoing uncertainty regarding Puerto Rico credits, and particularly the power authority (PREPA), investor sentiment remains high in tax exempts and their superior tax adjusted yields. With prices on PR GO and COFINA debt rebounding of late, the much- feared negative impact from Puerto Rico on the asset class has so far been limited. This view is best reflected in fund flows, which recorded their highest weekly figure in nearly three months: $688 million in new cash, with high yield funds receiving $308 million of it. Valuations continue to be supported by strong fund flows and record amounts of maturing bonds, in an environment where supply continues to underwhelm relative to prior years. Only $4 billion of new debt is slated to price this week, with a $750mm loan for the California State University system (Aa2/ AA-) being the largest issuer.

Following recent similar actions from Moody’s and Fitch, Standard and Poor’s (S&P) raised their credit rating on the state of New York to AA+ from AA. Citing the demonstrated ability of Governor Cuomo to keep spending in check and closing budget deficits, New York now has its highest S&P rating since 1972. Conversely, Moody’s reduced Pennsylvania’s credit rating one notch to Aa3, citing rising pension costs and “growing structural imbalances.”

AAA Municipal Market Data (MMD) Yield Curve

Source: Thomson Reuters

Weekly Municipal Mutual Fund Flow Data

Source: Lipper AMG Data

Taxable

Investment grade spreads were unchanged over the course of the week, holding to pre- financial crisis levels. Despite an earnings season that has exceeded expectations, and thereby providing relief to an asset class with elevated prices, we continue to exercise caution on high grade debt. We maintain the view that high grade corporate spreads have limited upside from current levels, believing that increasing risks—namely, interest rate and geopolitical risks—will limit any material improvement in spreads.

With most of the larger, money-center banks and brokers having reported, we reiterate our preference to overweight banks within taxable portfolios. Across the board, loan growth, asset quality, and investment banking revenues were strong—offsetting a decline in trading volumes. Another area we continue to favor in taxable mandates are taxable municipals. Taxable munis, which are Federally taxable, often provide generous spreads relative to traditional and similarly rated corporate credits.

© 2014 Castleton Partners, LLC. All rights reserved.

THE FOLLOWING NOTES AND DISCLOSURES ARE AN INTEGRAL PART OF THIS REPORT: Past performance is not a guarantee of future results. Different investments involve varying degrees of risk, including the risk of illiquidity and the risk that you could lose part or all of your investment. There can be no assurance that the future performance of any specific investment, investment strategy, or product (including those discussed herein or recommended or undertaken by Castleton Partners, LLC) will be profitable, equal any corresponding indicated historical performance, be suitable for your portfolio or individual situation, or prove successful. Charts, graphs and indices are included herein only for reference and do not constitute forecasts of the past or predicted future performance of any investment. Indices are not investments. Due to changing market conditions and other factors the content herein may no longer reflect Castleton Partners, LLC’s current opinions or positions. Nothing discussed herein is or is intended as tax, legal, accounting or personalized investment advice from Castleton Partners, LLC. Should you have any questions regarding the applicability of any specific issue discussed herein we encourage you to consult competent advisers of your choosing. Nothing herein is or is intended as an offer to sell or a solicitation of offers to buy any security. Castleton Partners, LLC’s current written disclosure statement including discussion of our advisory services and fees is available upon request.