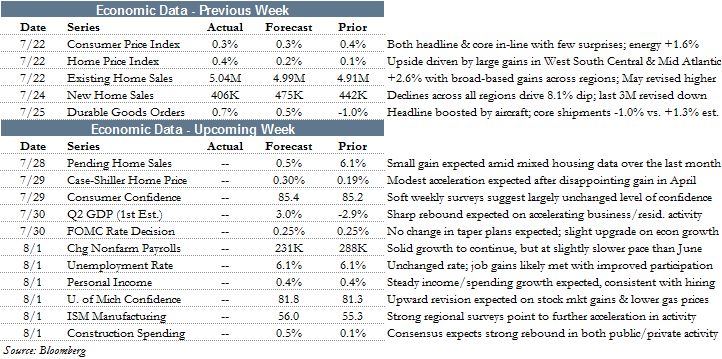

HOME SALES DIP

Equity markets were mixed to negative last week as the Dow fell 0.8% and the Russell 2000 declined 0.6%. The S&P 500 ended the week flat while the NASDAQ gained 0.4%.

Despite being a lighter week in terms of quantity of economic releases, the data that did come out warranted attention. Inflation measures kicked off the week with the monthly release of the Consumer Price Index (CPI). Matching consensus forecasts, inflation rose 0.3% month-over-month, as gasoline jumped 3.3% in the month. Despite coming in 0.1% below May’s reading, the year-over-year rate remains above the Federal Reserve’s target of 2.0% at 2.1%.

While overall consumer prices increased, the core reading, which excludes food and energy increased just 0.1%. Year-over-year the rate is unchanged at 1.9%. Gains came from drugs, tobacco and apparel. Apparel experienced an outsized gain of 0.5% in the month. Other readings were mostly flat.

Other noteworthy data came out of the housing market with the release of home sales and price data. The FHFA’s House Price Index rose 0.4% in May surpassing consensus estimates of 0.2%. Despite rebounding from April’s reading of 0.1%, housing prices slowed 0.6% year-over-year to 5.5%. Gains occurred in the West South Central and Mid-Atlantic. Weakness was experienced in the East South Central and East North Central regions. Lower price growth should give a boost to home sales, albeit at the expense of homeowner wealth.

Existing and new home sales painted a mixed picture. Existing home sales increased 2.6% in June to 5.04 million, beating expectations of 4.99 million. Single-family sales rose 2.5% with condo sales up 3.4%. All regions showed gains in June with the Midwest up 6.2%. On the other hand, new home sales data came in weak at an annual rate of 406,000 in June. This was well below consensus expectations of 475,000, as all regions showed declines - particularly the South, which dipped 9.5%. May was also revised down 62,000 to 442,000. Pending home sales and the Case-Shiller Index, which come out Monday and Tuesday, should provide a bit more color to the housing market picture.

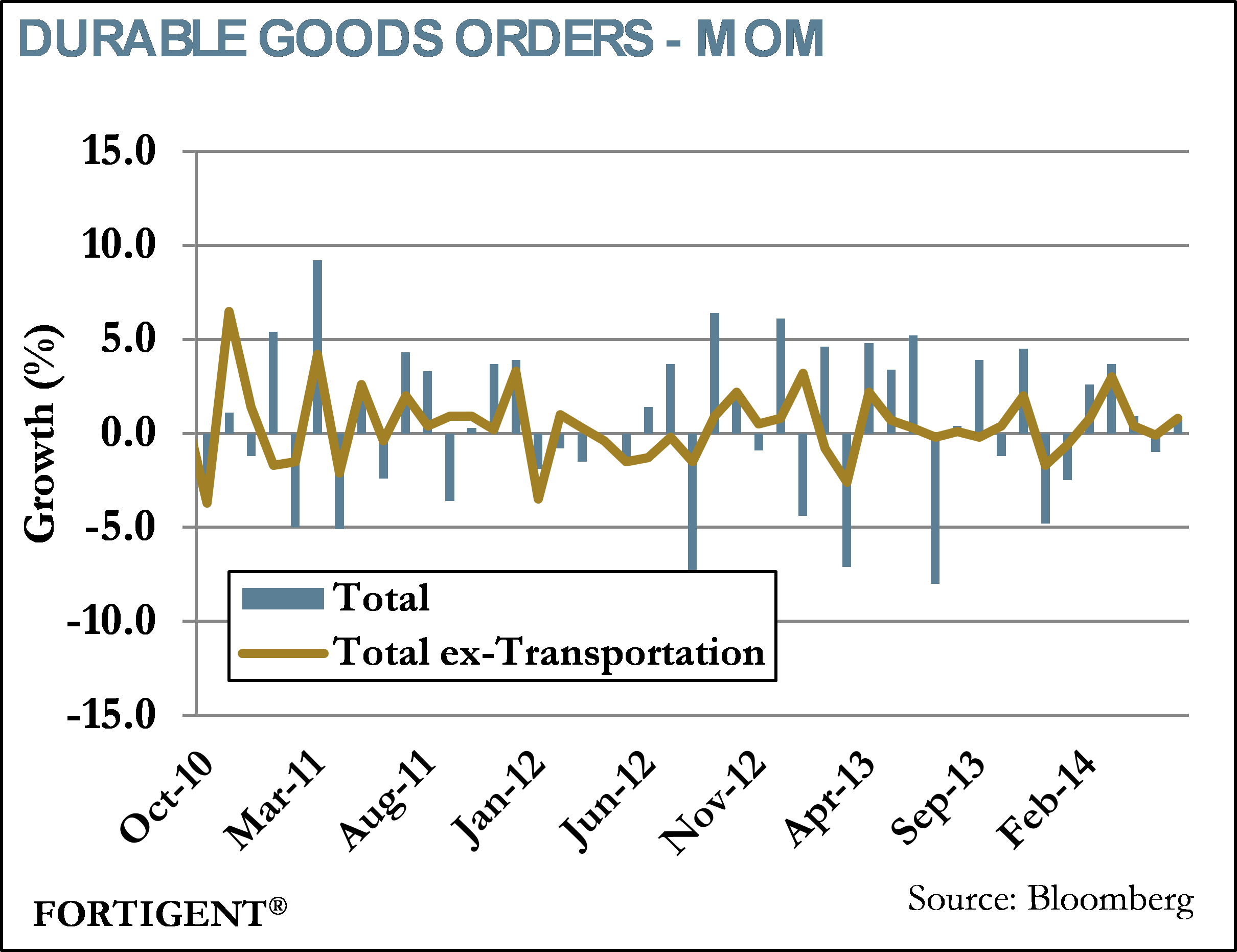

Durable goods orders, which wrapped up the week, painted a rosier picture as the headline reading showed a 0.7% gain. This represented a rebound from May’s 1.0% decline. Transportation led the way with a 0.6% gain, boosted by defense and nondefense aircraft orders. Motor vehicle orders declined. Outside of transportation, primary metals, machinery, and computers & electronics posted solid gains. Investors will be eyeing ISM’s release of manufacturing data later this week in order to gain more insight on the recent uptrend in manufacturing.

CORPORATE EARNINGS SEASON UPDATE

As the so-called punchbowl provided by the Federal Reserve is slowly withdrawn, $10 billion at a time, investors are increasingly looking to corporate fundamentals to see what might drive equity markets higher in the quarters ahead. Now three weeks into second quarter earnings season, market participants have a better idea of just how the most recent cycle is shaping up.

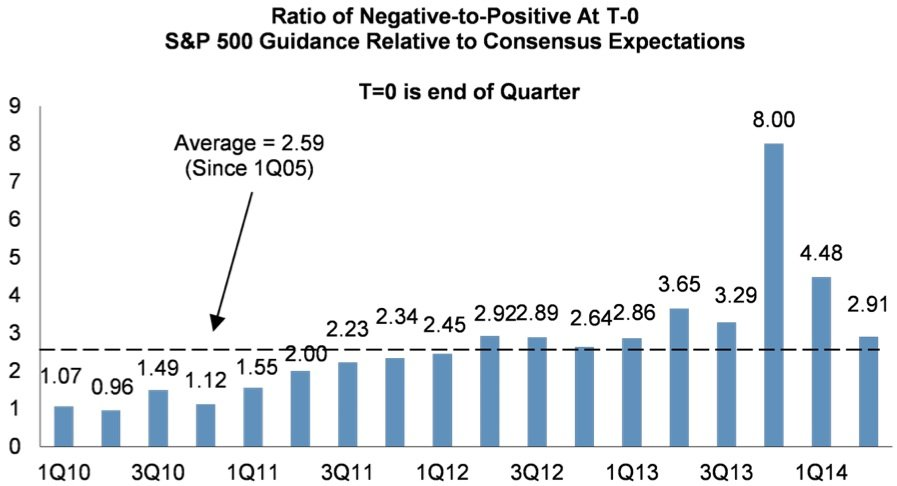

Coming into the quarter, expectations were fairly strong following a soggy first quarter that was weighed down by weather-related slowdowns. Thomson Reuters data indicated expectations for a 6.2% increase in earnings growth as of July 1. Negative revisions were shallower this time around, as negative guidance issued by companies receded in the lead up to this reporting season.

Source: Morgan Stanley

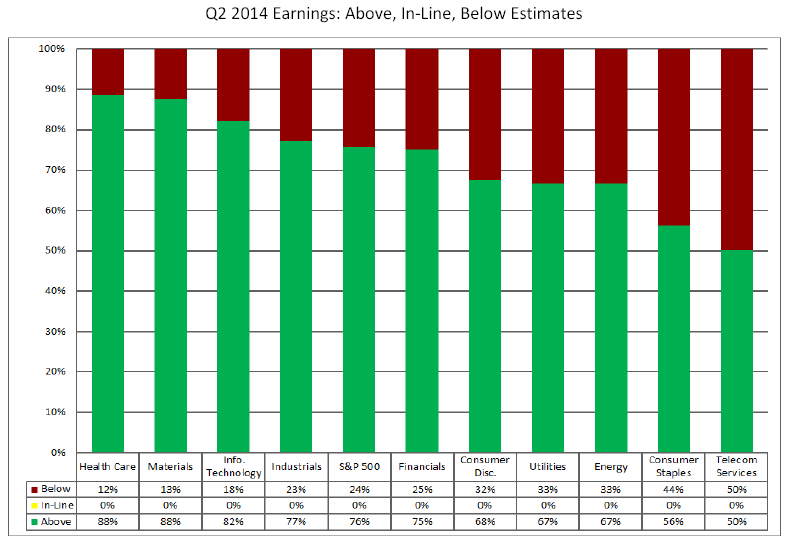

Through last Friday 230 companies in the S&P 500 had reported (46% of the index) operating results. According to FactSet, 76% of those companies reported earnings that exceeded consensus expectations, well above recent averages. Particular strength has been observed in health care, materials, and technology stocks, where more than eight in 10 companies have posted upside surprises.

Source: FactSet

Earnings growth itself was also impressive, with the blended rate for reporting companies now at 6.7%. That strength has been broad-based, with every sector but financials in positive territory. Although outliers such as Goldman Sachs and Bank of America were very strong in the period, other index stalwarts like J.P. Morgan and Citigroup saw earnings contract amid poor trading revenue and litigation costs. FactSet notes that on an ex-financials basis, the S&P 500’s current 8.5% earnings growth rate is the highest since 2011.

Market observers have taken notice. As noted by Zacks, the investment research firm, “growth rates are better, more companies are coming ahead of estimates, and there is even some modest improvement on the guidance front.” They believe the pickup in guidance, in particular, is already spilling over into expectations for the third quarter. Thomson Reuters indicates that expectations for third quarter growth is currently 10%, boosted by a rebound in financial company profits after two negative quarters.

Source: Thomson Reuters

It remains to be seen whether this stronger than expected earnings period will be enough to fuel equity markets higher. Stocks have faltered recently after reaching all-time highs, perhaps just a momentary pause in an upward trend or the start of a correction. Against the backdrop of benign credit conditions and increasing economic growth, one could logically conclude the former. However, with geopolitical issues once again hitting headlines, potential negative catalysts remain. The rest of the second quarter earnings season should indicate how well the markets can absorb any future trouble spots.

THE WEEK AHEAD

The Federal Reserve takes center stage this week with their regularly scheduled FOMC meeting on Tuesday and Wednesday. The group is expected to cut an additional $10 billion from its quantitative easing program and to place an explicit end date on QE for October, contingent upon economic data. No change to the Federal Funds rate is expected at this time.

Economic data picks back up this week with the first estimate of second quarter GDP, the unemployment rate, and the release of FOMC minutes being highly watched. As mentioned previously, more clarity on the direction of the housing market will come with the release of pending home sales and the Case-Shiller Home Price Index early in the week. Other data includes consumer sentiment indices, change in nonfarm payrolls, ISM Manufacturing index, personal income, and construction spending.

Earnings season continues with reports from BP, Pfizer, Barclays, ExxonMobil, Chevron, and Proctor & Gamble.

Central bank policy announcements are due from Israel, the Czech Republic, and Columbia.

ABOUT FORTIGENT

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value