It seems there is a growing disconnect between what the financial markets are discounting and the reality of what is transpiring in the domestic and global economies. While economic growth has the potential to increase during the second half of the year we are not expecting a dramatic acceleration since there are still structural problems in the economy. The result is slow private credit expansion, a lack of fixed investment and a slow rate of business formation. Five years after the Financial Crisis corporate management still believes that there is too much economic and political uncertainty and they are not compensated to take risks in their business. As we talk to institutional investors around the country, the consistent theme is that there is no place to go to earn a reasonable return in the fixed income sector except the short end of the curve. In this issue, we discuss our investment strategy for the second half of the year.

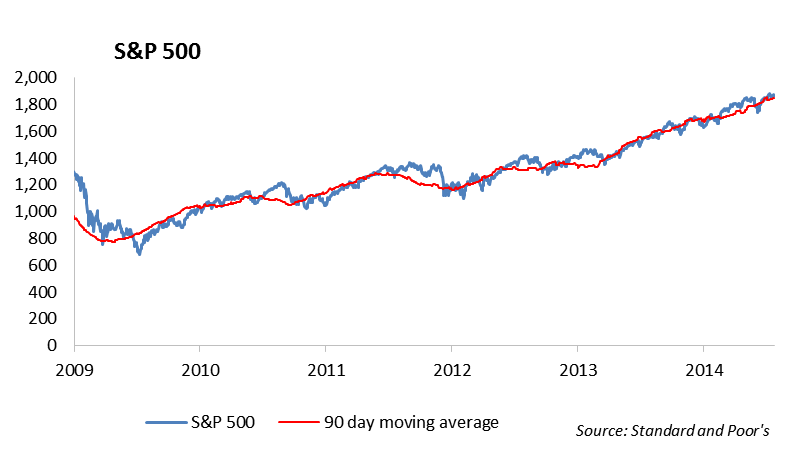

There are a growing number of inconsistencies in the domestic capital markets that are troubling. First, asset prices continue to move higher in spite of the slow growth economic reality. The U.S. market appears euphoric as stock prices hit another all-time high with the Dow Jones Industrial Average clipping 17,000 last week. At the door step of second quarter earnings season, we expect to see another lack luster quarter of corporate earnings. Similarly, real estate prices in the U.S. are near lofty levels not seen since 2007. The equity market seems more focused on continued liquidity support from the Federal Reserve than any negative news coming through corporate earnings.

Second, as equity prices climb higher, bond prices remain persistently high as well. In spite of strong signals from the Federal Reserve that they will eventually raise interest rates, interest rates actually declined during the quarter. This is incongruous with the current economic recovery and stated intentions of the Federal Reserve. Recently released data from the U.S. Treasury Department reveal rapid large scale purchases of U.S. Treasuries by China’s central bank this year, which may explain the drop in U.S. interest rates. During the first five months of the year China purchased over $100 billion in U.S. Treasury notes in an attempt to weaken the yuan and drive their exports higher. This is in contrast to most other central banks which have indicated that they would be net sellers of U.S. Treasury securities once the Federal Reserve ends its bond buying program and indicates that it will raise interest rates.

Third, in its recently published annual report, the Bank for International Settlements (BIS) warned of risks brewing in the emerging markets and set out early warning indications of possible banking crises in a number of regions, most notably China. We have already seen problems with banks in Spain and Portugal. In addition, the rally in both stocks and corporate bonds does not reflect the growing geopolitical risks around the globe. The current level of U.S. equity prices currently ignores the escalation in conflict in the Ukraine, the Middle East and China. In addition, our inability to deter Iran from manufacturing a nuclear weapon will ultimately alter the balance of power in the Middle East.

Finally, there is no meaningful leadership in Washington DC that is helping to address issues that are critical for our country. The implementation of the Affordable Healthcare Act has been costly and difficult and issues such as social security, Medicare, and tax policy have gone unaddressed. The result is a growing debt burden that will be difficult for the country to absorb as we continue to spend on social programs that we cannot afford in their current state.

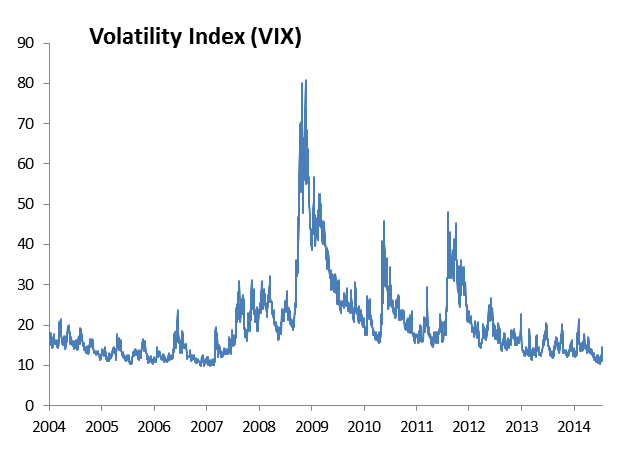

In all of this, it is striking how low volatility is in the capital markets. The low volatility reflects the aggressive monetary programs the Federal Reserve has implemented to push interest rates down. The low volatility, which has acted like an anesthetic and numbed investors to risk and return, is not consistent with the level of risk investors are incurring. The result is that there is way too much money sloshing around in the financial system; however, at some point volatility will increase and we expect that will provide a jolt to our capital markets and allow for the repricing of risk.

The Economy

The Commerce Department reported a surprising first quarter revised growth in GDP of -2.9%. This revised GDP report represents the largest single quarterly decline since the last recession and the largest drop recorded since World War II that wasn’t part of a recession. We believe the first quarter downturn was largely due to weather disruptions, lower adjustments in inventories and weak demand overseas. While the severity of the drop in first quarter output calls into question the underlying strength of the economy, the economy is still on track to show the marginally undramatic growth we expect for the year.

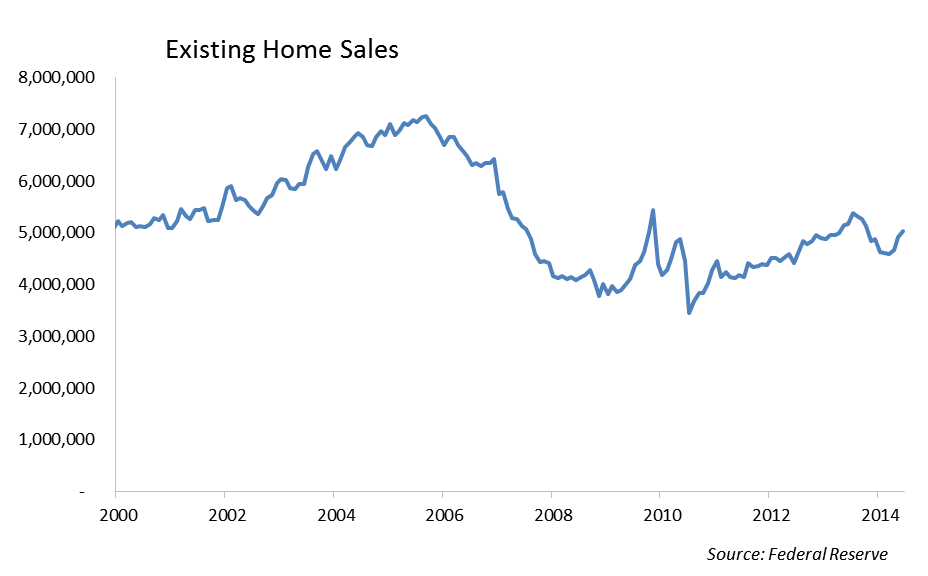

For the second quarter, we expect the U.S. economy grew by over 2.0% largely benefiting from the demand shift from the prior quarter’s weather anomalies. Sales of new homes surged to a six month high this past quarter, while existing home sales rose to their highest level since October. With more disciplined mortgage lending from the banks and less leverage in home builders, we do not believe the housing market will be the juggernaut for the economy that it was from 2000 to 2007.

In addition, the job market continues to show improvement. Job growth increased by 288,000 in June as the unemployment rate dropped to 6.1%. This represents the fifth straight month of employment gains over 200,000 which is the first time in 14 years the U.S. economy has experienced that strength. While much of the growth in employment has been concentrated in low paying jobs in the service sector, evidence is growing of increasing demand for skilled labor. With rising demand for skilled labor, we should see some modest pressure on wages.

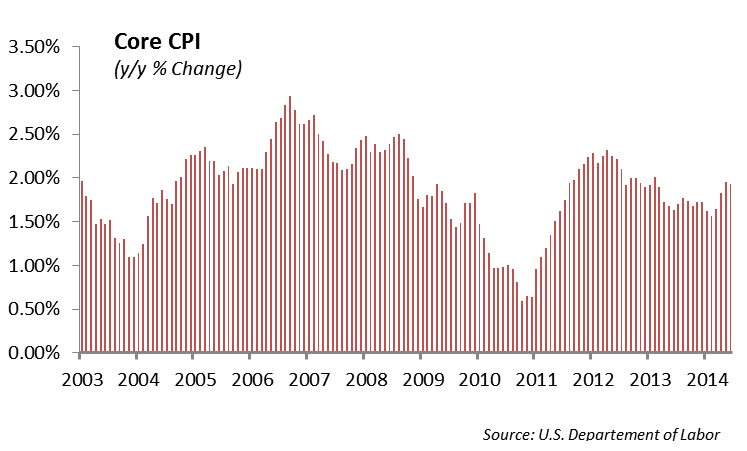

U.S. inflation, measured by the Core Consumer Price Index, accelerated by 2.0% in May representing its highest level in more than a year and half. This is actually welcomed relief for Fed officials who have been more concerned about deflation over the past three years. The recent pickup in inflation during the quarter was largely across food prices, gas prices and utility bills and is consistent with the incremental tightening in the labor markets. Since 1958, price gains measured by Core CPI have averaged 3.82% a year. However, since the Financial Crisis began in August of 2008, the Core CPI has averaged a mere 1.68% a year. Inflation can be both a good thing and a bad thing in an economy. Inflation may signal a rise in wages and increased spending. On the other hand, if wage growth is stagnant, as the general price level rises each unit of currency buys fewer goods and services.

As a result, inflation reflects a reduction in the purchasing power per unit of money. This loss in purchasing power is a negative effect of inflation.

When prices rise, it can have a negative impact on consumer spending if wage increases do not keep up. Since the recession, job growth has been slow and largely focused in low level service jobs with low pay. As a result, wage growth has been slow. This is one of the reasons that we see so much focus on increasing the minimum wage across state and local government.

Geopolitical Risks appear to be Growing

There appears to be growing instability around the globe and exuberant asset prices in the U.S. capital markets appear to be ignoring much of it. After invading Crimea after hosting the winter Olympics, Russia attempted to annex Ukraine. After intense lobbying to take a leadership role in peace talks and heavy economic sanctions, Russia has still not backed down from backing the Separatists. One of the key takeaways from Russia’s invasion is that European defenses are pathetically weak and European businesses, particularly in Germany desire to continue to sell goods and services to Russia. We expect that Europe will take a more conciliatory tone with respect to sanctions than the United States. In the European banking sector, Portuguese bank Banco Espirito Santo SA indicated that it would not be able to meet its short term obligations sending the European markets reeling.

Friction in the Middle East has escalated as Israel renewed bombing of Palestinian territories. At the same time, Iraq and Syria are facing their own civil wars. Iran remains belligerent about bowing to Western demands and curtailing its nuclear weapons program. On the other side of the world, China has shown its growing military arsenal as it enforces its territorial claim on an increasing swatch of the South China Seas and recently stretched its defenses over to Vietnam. With the continued growth of China’s military and disproportionate male population, we are concerned with the heightened level of China’s aggressive initiatives. As the Fed moves to reduce its stimulus, we expect that volatility may increase. Any random global act of aggression or banking problem may act to amplify that volatility.

Investment Strategy

Valuations in the bond market are lofty across all the major fixed income sectors. For those investors that believe in mean-reversion and that investment returns follow a normal bell-curve distribution pattern, we would suggest reviewing the past 20 years of data in the bond market. The average annual return of the Barclays 7-10 year U.S. Treasury Index from 1994 to 2014 was 6.72%. In order to achieve those same average returns over the next three years it would require a dramatic downward shift in rates. If you purchased and held the current 10 year U.S. treasury for three years, that would require a downward shift in the yield of roughly 64 basis points a year. This would put the yield at roughly 0.54% at the end of the holding period. We simply do not believe this is sustainable. With the Federal Reserve preparing to exit its asset purchase program, we would tend toward caution in our fixed income allocation. While low yields have been a huge boon for corporate borrowers, it has become the bane for investors. Fixed income is still an important asset class for asset allocation and risk management of a portfolio since it is one of the major noncorrelated asset classes to equities. However, in the face of potentially flat to negative returns, we are choosing a more conservative approach to our fixed income allocation. As a fixed income portfolio manager, this is the time to shorten duration and move up in quality since the cost is so cheap with the spread compression we’ve experienced.

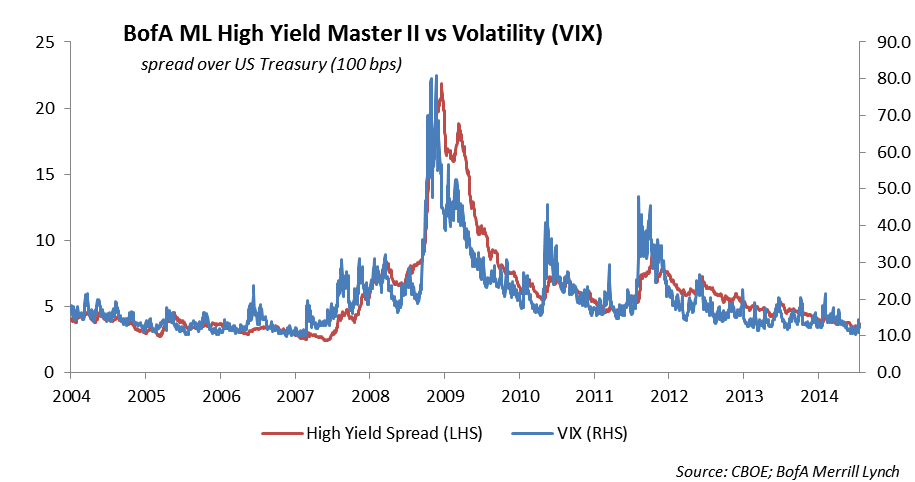

The high yield market is trading at levels never seen before. The weighted average yield of the BofA Merrill Lynch High Yield Master II Index hit an all-time low of 5.2% in June as the weighted average spread crept in to 335 basis points over U.S. Treasuries. One of the more concerning aspects of the high yield markets is that deals are getting done with little or no covenant protection for bond investors. Typically, when the volume of “covenant light” deals increase in the market, default rates increase in two to three years. According to Moody’s default rate study, the second quarter 2014 trailing 12-month U.S. speculative-grade default rate was 1.9%, compared to 3.0% just a year ago.

The Barclay’s U.S. Aggregate Index has produced a total return of 3.93% year-to-date. What is remarkable about that figure is that the weighted average yield to worst was at a 2.22% at the end of June. The spread over U.S. Treasuries is at the lowest level since 2007. The municipal bond market, measured by the Barclays Municipal Bond Index produced a total return of 6.00% so far this year. With a weighted average yield to worst for the index of 2.36%, it is the same story as the rest of the bond market – spreads are tight and interest rates are low.

The high yield market is trading at levels never seen before. The weighted average yield of the BofA Merrill Lynch High Yield Master II Index hit an all-time low of 5.2% in June as the weighted average spread crept in to 335 basis points over U.S. Treasuries. One of the more concerning aspects of the high yield markets is that deals are getting done with little or no covenant protection for bond investors. Typically, when the volume of “covenant light” deals increase in the market, default rates increase in two to three years. According to Moody’s default rate study, the second quarter 2014 trailing 12-month U.S. speculative-grade default rate was 1.9%, compared to 3.0% just a year ago.

The Barclay’s U.S. Aggregate Index has produced a total return of 3.93% year-to-date. What is remarkable about that figure is that the weighted average yield to worst was at a 2.22% at the end of June. The spread over U.S. Treasuries is at the lowest level since 2007. The municipal bond market, measured by the Barclays Municipal Bond Index produced a total return of 6.00% so far this year. With a weighted average yield to worst for the index of 2.36%, it is the same story as the rest of the bond market – spreads are tight and interest rates are low.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2014 Winthrop Capital Management