The intensifying geopolitical backdrop of Ukraine/ Russia, Israel/ Gaza, and Iraq/ ISIS continued to influence market activity and investment flows last week. As a result, intermediate and longer-dated Treasury rates were able to revisit their low yields of the year, last touched in May. However, the one thematic constant that continued unabated last week was the persistent flattening of the yield curve—the one trend that we are unwilling to fade. Officially, the yield difference between the 5 year and 30 year Treasury narrowed another 10 basis points last week, to +160bp: its flattest point in over five years.

From a fundamental perspective, longer dated rates found additional relief from Federal Reserve Chair Janet Yellen’s semiannual testimony to Congress. Stressing that long-term inflation expectations remain “well anchored”, she underscored the Fed’s desire to keep rates lower than it had in the past—even after targets for employment and inflation have been reached. Despite these remarks, which are supposed to reflect the opinions of the entire FOMC, the “hawks” in the Fed are starting to become more vocal. With the end of quantitative easing near, we suspect the frequency and intensity of dissenting FOMC members’ voices may start to become potentially market moving events, especially in an environment where financial volatility is virtually non-existent. Dallas Fed President Richard Fisher, a known “hawk”, had a particularly entertaining speech last week comparing current monetary policy to “beer goggles” for the markets. Click here to read that speech.

Notable economic releases this week include CPI, existing home sales, and durable goods.

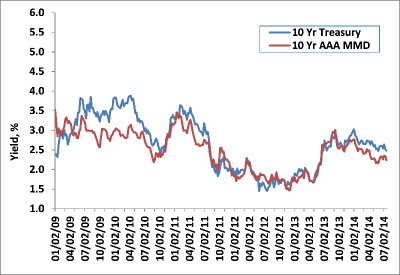

Weekly Change: 10Y Treasury Yields vs. 10Y AAA MMD

Source: Bloomberg, Thomson Reuters and Castleton Partners

Ratio of 10Y Muni Yield to 10Y Treasury Yield

Source: Bloomberg, Thomson Reuters and Castleton Partners

Tax-Exempt

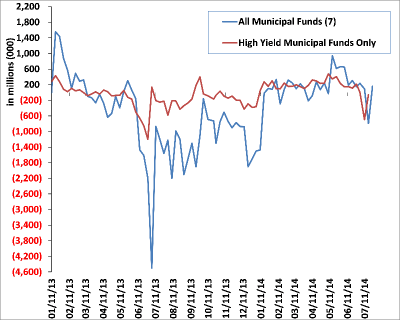

Despite intense asset class-wide focus on Puerto Rico—most notably on its utility provider PREPA and whether it will have the means to pay down credit lines in coming weeks, the municipal market was able to register strong price gains, recovering fully from its substantial underperformance relative to taxable markets two weeks ago. With fund flows returning to positive territory (+$158mm) amidst a modest calendar, primary deals were well received with bids reemerging in secondary markets, depleting dealer inventory in the process. Unlike the August/ September period of last year, it appears the contagion effect of Puerto Rico and its rapidly deteriorating agencies has been limited (thus far). Fund flows have been fairly stable, while high grade tax exempts have been experiencing a flight to quality bid—similar to developments in the Treasury market.

On the week, benchmark ten and thirty year yields were able to rally by 11 and 8 basis points respectively, with five year muni yields rallying 5bp. The flattening muni yield curve—where long dated maturities outperform shorter dated instruments—also continued in force last week. The 5y-10y tax exempt yield spread has now fallen to +99bp, well off of the +153bp level at the start of 2014. Muni/ Treasury ratios rebounded as well, with the 10y Muni/ Treasury ratio falling to 90%, a near 4 point decline in favor of tax exempts from the prior week.

Another high profile municipal issuer receiving heightened investor concern of late is the State of New Jersey. Credit spreads in NJ issuers have widened of late, as burdening pension issues, high unemployment relative to the national average, and a stagnant housing recovery weigh on New Jersey. Negative developments in Atlantic City last week further pressured credit spreads, as it was announced that as many as four casinos may close by this fall. As the only NJ city under state supervision, Atlantic City continues to experience a sharp decline in its finances, chiefly due to lost revenue from increased gambling competition from nearby casinos in Pennsylvania, New York, and Connecticut.

The favorable technical backdrop in tax exempts is expected to remain in place this week, supporting prices as only $5 billion is expected in new supply. The largest transactions are a $780mm State of Maryland (Aaa/AAA) general obligation loan and a $720mm loan for the New Mexico Energy Acquisition Authority (Aa3).

AAA Municipal Market Data (MMD) Yield Curve

Source: Thomson Reuters

Weekly Municipal Mutual Fund Flow Data

Source: Lipper AMG Data

Taxable

With Q2 earning season in full swing, last week was an unsurprisingly subdued week in investment grade corporate debt. New issue volume was the third lowest so far in 2014, with just over $10 billion priced. After trading flat for most of the week, spreads widened 2bp across most sectors once word of the cause of the Malaysian plane crash hit the tape. Confirming demand for income with any excess spread relative to Treasuries, high grade funds received over +$1.6b of net new cash last week. Taxable high yield funds, conversely, registered their largest weekly outflow since August 2013: -$1.7b.

Earnings releases will continue to dominate market activity this week, as high profile issuers such as Apple, Google, McDonalds, and Coke are reporting.

The Word of the Year?

Referenced many times by Chair Yellen and other FOMC members over the last several weeks is a word that, frankly, we knew little about—failing to recall its use during our (long ago) economics classes: Macroprudential. Referenced as a (new?) tool by Chair Yellen in monetary policy, we thought we would pass along the meaning, courtesy of Bloomberg, as we suspect its use (and confusion) may only grow...

Macroprudential

A method of economic analysis that evaluates the health, soundness and vulnerabilities of a financial system. Macroprudential analysis looks at the health of the underlying financial institutions in the system and performs stress tests and scenario analysis to help determine the system’s sensitivity to economic shocks. Macroencomic and market data are also reviewed to determine the health of the current system. The analysis also focuses on qualitative data related to financial institutions’ frameworks and the regulatory environment to get an additional sense of the strength and vulnerabilities in the system.

Investopedia Says…

When looking at the health of the underlying financial institutions in the system, macroprudential analysis uses indicators that provide data on the health of these institutions as a whole including capital adequacy, asset quality, management performance, profitability, liquidity and sensitivity to systematic risks. Macroeconomic data used includes gross domestic product (GDP) growth rates, inflation, interest rates, balance of payments, exchange rates, asset prices and the correlation of markets within the system. Finally, macroprudential analysis looks at key components of the financial markets, including prevailing credit ratings and the yields and market prices of financial instruments.

Scenario analysis and stress tests are major components of this analysis. For example, the analysis may look at how the system would cope with a steadily declining currency value and its impact on GDP, interest rates and underlying institution profitability.

© 2014 Castleton Partners, LLC. All rights reserved.

THE FOLLOWING NOTES AND DISCLOSURES ARE AN INTEGRAL PART OF THIS REPORT: Past performance is not a guarantee of future results. Different investments involve varying degrees of risk, including the risk of illiquidity and the risk that you could lose part or all of your investment. There can be no assurance that the future performance of any specific investment, investment strategy, or product (including those discussed herein or recommended or undertaken by Castleton Partners, LLC) will be profitable, equal any corresponding indicated historical performance, be suitable for your portfolio or individual situation, or prove successful. Charts, graphs and indices are included herein only for reference and do not constitute forecasts of the past or predicted future performance of any investment. Indices are not investments. Due to changing market conditions and other factors the content herein may no longer reflect Castleton Partners, LLC’s current opinions or positions. Nothing discussed herein is or is intended as tax, legal, accounting or personalized investment advice from Castleton Partners, LLC. Should you have any questions regarding the applicability of any specific issue discussed herein we encourage you to consult competent advisers of your choosing. Nothing herein is or is intended as an offer to sell or a solicitation of offers to buy any security. Castleton Partners, LLC’s current written disclosure statement including discussion of our advisory services and fees is available upon request.