Geopolitical Headlines Kick Up Volatility

Despite a volatile week for equities, the S&P 500 and Dow ended the week up 0.5% and 0.9%, respectively. Small stocks continued their decline from the previous week with the Russell 2000 falling 0.7%.

Retail sales kicked off a week occupied with geopolitical headlines. Sales for June came in below expectations as auto sales surprised to the downside. Retail sales increased 0.2% from the prior month, coming in well below the 0.6% forecast. Excluding the 0.3% decline in auto sales, sales gained 0.4%. Retail sales for May were revised up to 0.5% from 0.3%.

Similar to retail sales, industrial production figures came in soft for June. Following an increase of 0.5% in May, industrial production slowed to a rise of 0.2% as auto production slipped. Excluding motor vehicles, manufacturing rose 0.2% with durable goods increasing 0.4%. Nondurable good production fell 0.3% with declines in the output of petroleum & coal products and apparel. The index for food, beverage, and tobacco products also fell 0.6%.

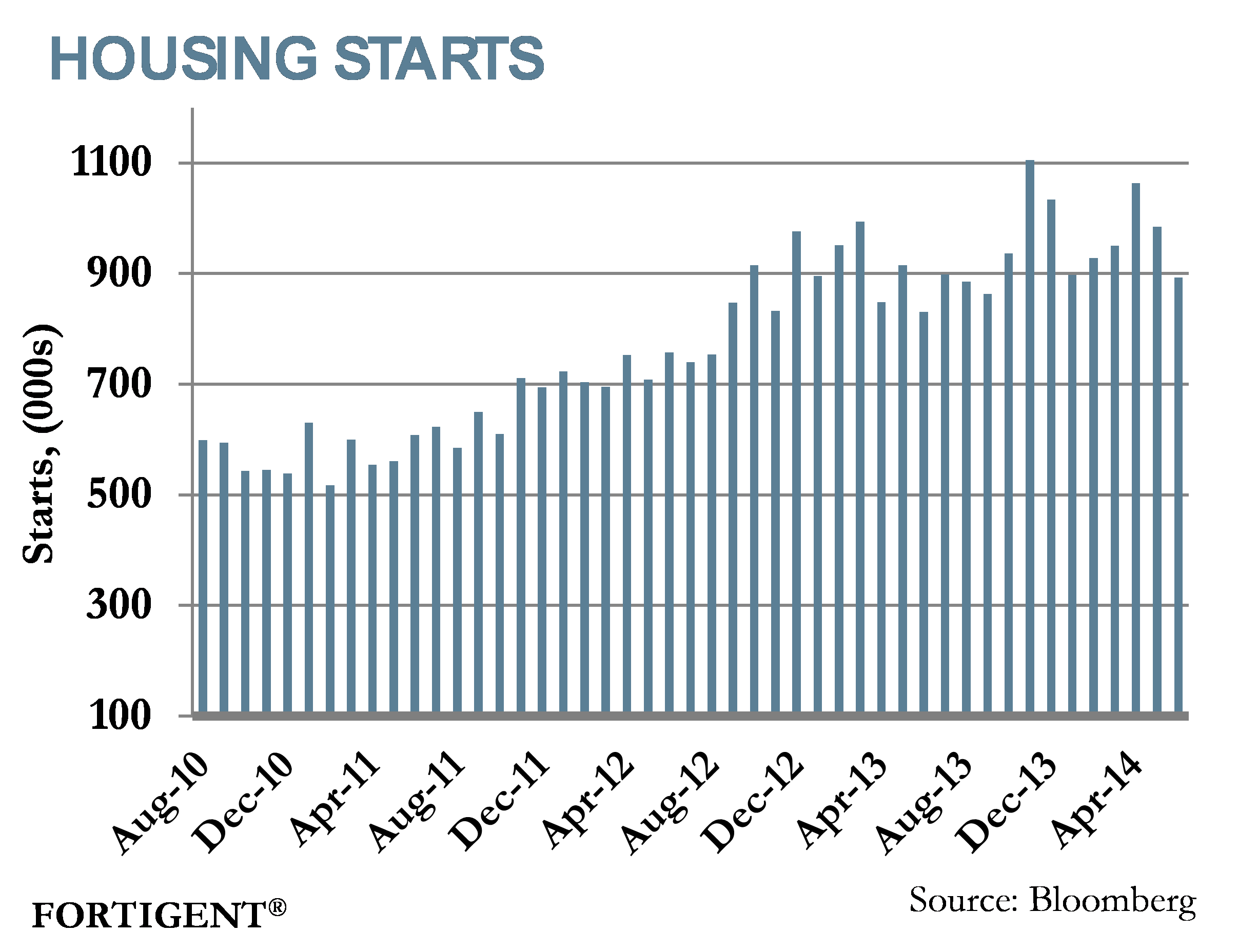

Housing market data came in mixed. The NAHB Housing index, which is a broad based survey on housing market conditions, jumped to 53 from 49. This came in above consensus forecasts for 50. Strength was seen in sales expectations and current sales. Housing starts, however, disappointed as starts fell 9.3% in June. This came after a 7.3% decline in May. Multifamily starts fell 9.9% while single-family starts dropped 9.0% with the South experiencing a record decline.

Price indexes came in somewhat mixed as import prices fell short of expectations while producer prices accelerated from last month’s decline. Import prices rose just 0.1% as food/feeds/beverage prices fell 1.7%. Export prices also declined as agricultural prices fell 1.8% on the month. Producer prices bounced 0.4%, rebounding from a 0.2% decline in May. The outsized jump was the result of rising energy prices. Excluding food, energy, and trade services, the PPI rose 0.2%.

The Philadelphia Fed Survey, which gauges manufacturing conditions within the Philadelphia Federal Reserve district, crushed consensus forecasts for 16.0 as the index surged to 23.9. The index rose to its highest reading since March 2011 as new orders, shipments, and unfilled orders soared. Despite covering only the mid-Atlantic region, the survey is often used as a broader indicator for US manufacturing activity.

The Conference Board’s Leading Economic Indicators index wrapped up the week. The index continued its rise, albeit at a slower-than-expected pace. The index increased 0.3% in June, but came in below consensus forecasts of a 0.5% jump. The report was mostly positive with seven of 10 components posting gains. Housing sector struggles were the largest drag on the index’s acceleration.

2014 another Ho Hum Year For Hedge Funds

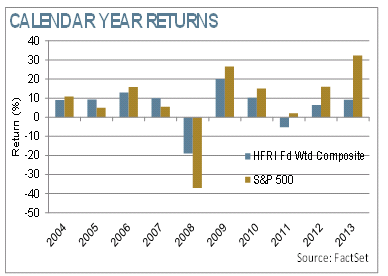

Through the first six months of the year, hedge funds have generated a positive, albeit somewhat modest return. According to data compiled by Hedge Fund Research, the Fund Weighted Composite of hedge funds in their universe had generated a 3.2% return, compared to the S&P 500’s 7.1% gain. While not terrible on a standalone basis, many investors had greater hopes for the asset class following five straight calendar years of underperformance versus the broad equity markets.

By most accounts, it should be a more ideal environment for alternative strategies. Equity market correlations are declining, organic growth is picking up, corporate activity is increasing, and central banks (at least the Fed) are slowly taking a step back from financial markets. Despite these developments, long/short stock picking remains difficult, and macro strategies are finding themselves consistently on the wrong side of trades.

Source: Credit Suisse

Entering the year, three of the most prevalent macro trades across many hedge fund portfolios were: Japan reflation (long equity/short currency), short interest rates, and short euro. Many managers were caught flatfooted by sharp reversals in the Japanese trade and bond yields that started in January and have persisted through 2014. The short Euro trade, meanwhile, befuddled many investors as the ECB was expected to engage in more accommodative measures amid accelerating disinflation in the region. As a result of these misreads, the average macro manager is up less than 1% year-to-date in 2014.

Struggles by equity strategies have been more surprising, given the aforementioned improvement in stock correlations. Long/short strategies, represented by the HFRI Equity Hedge Index, are up 3.3% YTD, while the market neutral sub-set of that group is up just 1.5%. March and April were a period of much publicized difficulty for many hedge fund managers, as heavy crowdedness in a cluster of high momentum stocks caused steep losses as those securities experienced a deep reversal.

Research by Credit Suisse, however, suggests that lower correlations are just one factor when examining alpha generation by managers. They found that volatility-adjusted alpha is indeed higher in lower correlation environments (illustrated in chart below), but increased volatility is also necessary in generating high levels of absolute alpha. Compressed volatility levels at present may therefore be contributing to lower overall performance by equity-centric hedge fund managers.

Source: Credit Suisse

Indeed, the lack of volatility not only in equity markets but other asset classes has made for a difficult environment for active managers. With less dispersion between securities, the spreads through which many strategies operate are narrower and, thus, less profitable. Lower volatility has also meant less premium generation for those in the business of explicitly selling those instruments as a means of income generation and return enhancement.

Another more basic observation about the 2014 environment is the dominance of the domestic blue chip market across the market spectrum. While hedge fund performance is generally compared to the S&P 500, the reality in 2014 is that most hedge fund portfolios are highly diversified by market cap and geography. To that end, small cap and international stocks have underperformed, with the Russell 2000 was up just 3.2% through the first six months of the year and the MSCI EAFE index up 5.1%.

Not much appears to have changed through the first three weeks of July, despite some recent turbulence in equity markets. Using the Morningstar Fund Category Indices as a daily proxy (HFRI indices are reported monthly), diversified alternative Funds were actually slightly negative through last Friday. Long/short equity mutual funds were up just 11 basis points, relative to the S&P 500’s 1% climb.

While this analysis applies to the broad universe of hedge funds, there are certainly individual products that are performing better. And as the number of hedge funds has grown, it may be possible that the generally accepted proxies investors use to evaluate hedge fund performance may be getting increasingly diluted. Still, the industry must hope that relative performance improves soon lest they permanently lose their mystique as all-weather return generators (and be relegated to a status as expensive downside protectors).

The Week Ahead

Economic data slows this week. The Consumer Price Index comes out Tuesday. Additional guidance on the direction of the housing market arrives via the Home Price Index and existing and new home sales. The week wraps up with durable goods orders.

Earnings season continues with reports from Halliburton, Apple, Coca Cola, Comcast, McDonalds, AT&T, Boeing, Visa and Caterpillar amongst others.

Central bank policy announcements are due from Hungary, New Zealand, and Russia.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value