Treesdale Partners, portfolio manager of the AdvisorShares Gartman Gold/Euro ETF (GEUR), AdvisorShares Gartman Gold/British Pound ETF (GGBP), AdvisorShares Gartman Gold/Yen ETF (GYEN) and AdvisorShares International Gold ETF (GLDE), share their thoughts about the gold space.

In this discussion piece we discuss the rationale for why investors looking to buy gold as a defensive asset during these uncertain times should consider buying gold in euro terms. When an investor buys gold in dollars they are expressing the view that they expect the price of gold to increase relative to the dollar. Similarly when an investor buys gold in euro, they express the view that they expect the value of gold to increase relative to the euro. We believe that a number of macroeconomic and geopolitical factors currently make both owning gold and in particular owing gold in euro terms an attractive trade.

Looking first briefly at the recent performance of gold in both dollar and euro terms we see that year to date gold in euro terms has returned 9.1% versus 7.8% for gold in dollars, its performance reflecting both the strength in the gold price and the weakness in the euro versus the dollar. A number of different factors lead us to expect this outperformance to continue:

1. The divergence between US and European monetary policy as the Federal Reserve comes to the end of its asset purchase program this year and as the European Central Bank struggles with persistently low GDP growth and disinflation is likely to weigh on the value of the euro versus the dollar and more generally lead to dollar strength on currency markets. Investors that wish to have an allocation to gold therefore face a conundrum in that in an environment where for macroeconomic reasons they may now expect the dollar to strengthen this would tend to put downward pressure on the price of gold in dollar terms. One way to address this conundrum would be to use an alternative financing currency other the dollar with which to buy gold thereby reducing the investor’s short exposure to the dollar as a result of holding gold. With such a strong and growing divergence in the relative stances of monetary policy between the US and European Union and with the European Central Bank have begun to explicitly highlight its concerns about the impact the strength of the euro is having on the recovery, the euro would appear to be a strong candidate with which to make gold purchases. Indeed with short term euro interest rates having now moved back below short term US interest rates, there is a small financing benefit to owning gold in euro terms versus owning gold in dollar terms.

2. Economic stresses within the Eurozone which came to the fore during the debt crisis remain largely unresolved but had faded from investors’ view since the European Central Bank’s historic “whatever it takes” commitment in 2012. However these have come into focus again triggered much to the markets’ surprise by concerns over the solvency of Banco Espirito Santo of Portugal. Rising economic tensions not just in the European periphery but in the core as the European Union as a whole struggles with falling prices and low GDP growth may again work to lower the value of the euro versus the dollar hence making owning gold in euro terms (i.e. long gold / short euro) a potentially more attractive investment than owning gold in dollar terms.

3. Another factor why we favor gold in euro terms over gold in dollar terms is that during credit crises, the dollar has tended to be “gold’s enemy”. Historically when we have seen sharp spikes in risk aversion the dollar has tended to be the main beneficiary as both domestic and foreign investors swap assets into US t-bills in a classic “flight to quality” asset rotation. Gold has also tended to perform well during these periods of rising risk aversion but during those particular instances when the dollar has risen rapidly in value at the same time this has tended to work against the defensive qualities of gold. Even as investors buy gold priced in dollars, ironically, sharp rises in the value of the dollar by definition lower the price of gold in dollar terms thereby working against the benefit of owning gold as a defensive asset. One way for investors that wish to hold gold as a defensive asset might be able to reduce this effect is to use an alternative financing currency other than the dollar with which to buy gold. Taking into consideration some of the macroeconomic considerations discussed above, any significant jump in risk aversion in Europe might be expected to reduce the value of the euro versus both the dollar and gold and as such holding gold in euro terms might perform better defensively relative to gold priced in dollars, in the event of a sudden jump by investors into dollar denominated assets.

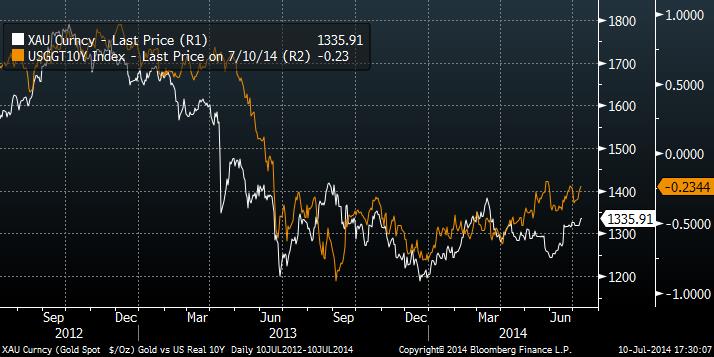

4. More generally the past year has seen a trend of lower real interest rates in the US (interest rates adjusted for inflation) which has been supportive for the price of gold. In the chart below we plot the price of gold in dollars with 10 year US inflation adjusted interest rates (inverted) and see that there has been a strong relationship between US inflation-adjusted interest rates and the price of gold - in fact this relationship has been fairly well established for the last 5 years. Should the softer tone of real interest rates continue which appears to be the case with the Federal Reserve’s favored measure of inflation, the core PCE deflator staying stubbornly below its 2% target level, we would expect the price of gold to be well supported at current price levels.

5. Finally we would also expect that rising geo-political tensions in Israel, Iraq and Ukraine will continue to lend support more generally to the demand from investors to hold gold.