Markets Preparing for a More Volatile Summer

- Strong performance across all asset classes

- Barclay’s Municipal Index up 6% in first half

- More volatility likely in second half

- Puerto Rico news overshadowing the market

- Near-term municipal market weakness could be an opportunity

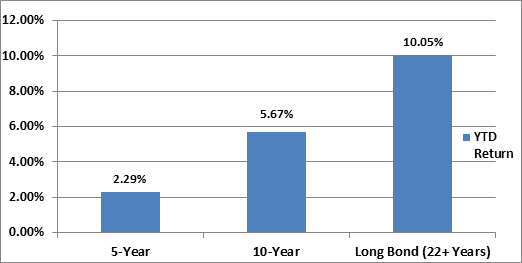

Financial market conditions were as good as could be expected during the first half of the year, as evidenced by positive investment performance across all asset classes. Stocks recorded their sixth consecutive quarterly advance, commodities moved higher, and bonds defied the consensus prediction of rising rates and registered some very impressive gains. Municipal securities were among the best fixed income performers. The Barclay’s Municipal Bond Index rose 6%, and gains across the municipal yield curve were strong, especially for the longest maturing bonds, which returned in excess of 10%.

Municipal Market Performance: First Six Months of 2014

Source: Barclay’s

The markets had little time to rest on their first half performance laurels. The June monthly employment report provided further confirmation of an improving economy. The combination of a fifth consecutive month of at least 200,000 jobs being created and a drop in the unemployment rate to 6.1% would normally be good for stocks, but not for bonds. However, global equities have been weakening since the start of the third quarter, while U.S. Treasury yields remain close to their lows for the year. The sustainability of global growth is being questioned. Investors are again worried about possible contagion effects in the Eurozone, highlighted by a recent report of banking problems in Portugal. Market conditions in Europe look a bit more precarious today. Disappointing June export news from China underscores slowing world demand. While the consensus of economists is that the U.S. economy is on a sustainable growth path, some analysts are now hedging their bets. Treasuries are again being viewed as “safe havens,” which should support other debt markets, including the municipal securities markets.

In the municipal world, it appears that the summer of 2014 could be similar to last year’s. During the summer of 2013, market volatility was intensified by Detroit’s credit woes and then followed by Puerto Rico’s debt repayment issues. This year, Puerto Rico is again in the news. Fortunately, the market is in much better condition currently due to less overall interest rate risk, reduced new-issue supply, and strong investor buying during the first half of the year.

Puerto Rico continues to be the dominant story in the municipal market following the passage of legislation allowing certain Puerto Rico public corporations (electric, sewer, and transportation) to restructure their debt. The unprecedented move resulted in a very significant reaction by the rating agencies. Puerto Rico Electric Power Authority (PREPA) debt ratings were cut by Moody’s to Caa2 from Ba3. S&P lowered its ratings to B- from BB. Fitch rates the bonds CC.

While not directly affected by the restructuring legislation, the market is worried that the Commonwealth’s general obligation and sales tax bonds could also be impacted in the future. Although there is strong language in the Constitution that protects these bonds, the market remains skeptical. Moody’s cut its ratings on the general obligation bonds to B2 from Ba2 and senior sales tax bonds to Ba3 from Baa1. Market access by the Commonwealth could be impacted in the future by the lower ratings. Adding to the uncertainty, two large mutual fund companies filed suit after the governor signed the restructuring bill. These suits could result in a prolonged legal battle without any near-term resolution.

It should be noted that liquidity for Puerto Rico debt has been good. Trading has been quite robust, with good “two-way” flow and generally tight quotes between the “bid” and “offer.” However, we believe volatility will remain for now. Hedge funds have been active traders.

An important factor in determining future market performance will be the behavior of municipal mutual fund investors. Fund flows were positive for the first half of the year; however, it appears the trend might be reversing, especially in the high yield and long-term fund categories, due to the negative press about Puerto Rico. Bond fund outflows should be monitored carefully to gauge the potential amount of selling by mutual portfolio managers to meet anticipated investor redemptions. Any upward move in rates due to fund-induced selling could provide a potential buying opportunity in general market names.

Strong market performance during the first half of the year suggests municipal holdings should be reviewed and possibly adjusted. Bond structure, maturity, duration positioning, and credit quality should be examined. The strong rally in long maturity bonds this year has resulted in a flattening of the municipal curve. The best relative value is in the intermediate (10-15 year maturity) range.

In summary, we are still generally constructive on bonds and the municipal market. Municipal bond yields have drifted a bit higher recently, while U.S. Treasury rates have declined. If this trend continues, the relative cheapness of municipals should attract more “cross-over” investor interest. The market remains in strong technical shape. New debt issuance is down significantly this year, and supply is likely to remain below normal, which should provide support. Finally, our hope is for the Puerto Rico headline risk to quiet down and allow investors to refocus on market fundamentals.

Disclosures

The information provided in this commentary is not intended to be a complete summary of all available data. Certain information contained herein has been obtained from published sources and/or prepared by sources outside SMC Fixed Income Management (“SMC FIM”), a division of Spring Mountain Capital, LP, and certain information contained herein may not be updated through the date hereof. While such sources are believed to be reliable, no representations are made as to the accuracy or completeness thereof by SMC FIM or any of its affiliates, directors, officers, employees, partners, members or shareholders, and none of the former assumes any responsibility for the accuracy or completeness of such information. Nothing contained herein shall be relied upon as a promise or representation as to past or future performance.

This commentary does not constitute an offer to sell or a solicitation of an offer to purchase securities, or any other product sponsored or advised by SMC FIM or its affiliates, nor does it constitute an offer or a solicitation to otherwise provide investment advisory services. It should not be assumed that any of the security transactions listed were or will prove to be profitable, or that the investment recommendations we make in the future will be profitable.

Statements contained in this commentary that are not historic facts are based on current expectations, estimates, projections, opinions and beliefs of SMC FIM. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Unless specified, any views reflected herein are those of SMC FIM and are subject to change without notice. SMC FIM is not under any obligation to update or keep current the information contained herein.

This commentary does not take into account any particular investor’s investment objectives or tolerance for risk. The information contained in this commentary is presented solely with respect to the date of its preparation, or as of such earlier date specified in it, and may be changed or updated at any time without notice to any of the recipients of it (whether or not some other recipients receive changes or updates to the information in it).

No assurances can be made that any aims, assumptions, expectations, and/or objectives described in this commentary will be realized. None of SMC FIM or any of its affiliates, directors, officers, employees, partners, members or shareholders shall be liable for any errors in the information, beliefs, and/or opinions included in this commentary or for the consequences of relying on such information, beliefs, or opinions.

Neither this commentary, nor any of the contents hereof, may be reproduced or used for any other purpose, or transmitted or disclosed in whole or in part to any third parties, in each case without the prior written consent of SMC FIM.

Copyright © 2014 Spring Mountain Capital, LP. All rights reserved.