Geopolitical headlines, coupled with renewed stress in European markets, led to a strong rally in US Treasuries last week. Further supporting the decline in interest rates was the perceived dovish overtone to the minutes of the June Federal Open Market Committee meeting. The yield curve flattened yet again, as intermediate and longer dated maturities registered outsized price gains relative to shorter dated notes and bonds. The US Treasury yield curve—specifically the spread between 5 year and 30 year bonds—has now fallen to its lowest level since February 2009 (+169bp). Risk assets, namely stocks, generated price declines as the market exhibited a classic “risk off” feel throughout the week.

As we embark on the second half of 2014, Castleton fully expects the yield curve to continue its flattening bias. The recent improvement in economic data—especially employment—will likely lead to a more hawkish tone from the FOMC going forward, producing more volatility in financial markets than was realized during the first half of this year. As market pundits publicly debate the timing and size of interest rate increases, expected to begin sometime in 2015, we expect the Fed-influenced front end of the yield curve—namely the 1 to 5 year area—to underperform. Given an economic recovery quieter than hoped for (as noted by negative GDP growth for the first six months of this year), the future direction of any interest rate policy may ultimately be lower than consensus, as a sustainable recovery is still impaired by a consumer experiencing flat wage growth and high debt levels.

The Federal Reserve will most likely remain in focus again this week, with Chair Yellen’s semi-annual testimony before Congress tomorrow and Wednesday. As for economic data, a host of tier one reports are scheduled for release, as well (Retail Sales; PPI; Industrial Production).

Weekly Change: 10Y Treasury Yields vs. 10Y AAA MMD

Source: Bloomberg, Thomson Reuters and Castleton Partners

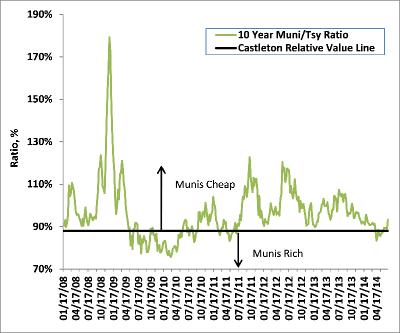

Ratio of 10Y Muni Yield to 10Y Treasury Yield

Source: Bloomberg, Thomson Reuters and Castleton Partners

Tax-Exempt

The first full week of July was not kind to municipals, with benchmark rates exhibiting sharp nominal and relative weakness versus their taxable counterparts. Muni underperformance is best measured by the cheapening of various Muni/ Treasury ratios last week. On average, Muni/ Treasury ratios across the maturity spectrum rose by 4-6 points. The 5y ratio (79%) now rests at its cheapest level since March, while the 10y (93%) is at its highest level since February. Uncertainty related to the recent universal downgrades of all Puerto Rico credits by the three main rating agencies, and concerns of escalating fund redemptions as a result, were the primary culprits for the tax exempt sell off. In fact, mutual funds did experience outflows of $790mm, the first such outflow in ten weeks. Though we do not anticipate a material muni yield correction, we do feel there is a good chance of the market “over correcting” on Puerto Rico through mutual fund induced selling—creating a buying opportunity in tax exempt debt. As mentioned above, we anticipate market volatility rising during the second half of this year. With its stable income stream, tax efficiency, and improving credit profile, we fully expect tax exempts to generate the best returns in fixed income for the balance of 2014.

Tax exempt supply this week stands at nearly $7 billion. Heavily influenced by such high tax states as California and New York, the largest loans this week are a $1.2b deal for San Francisco Bay Area Toll Bridge revenue bonds (Aa3/ AA-) and a $800mm loan for the New York City Transitional Finance Authority (Aa1/ AAA).

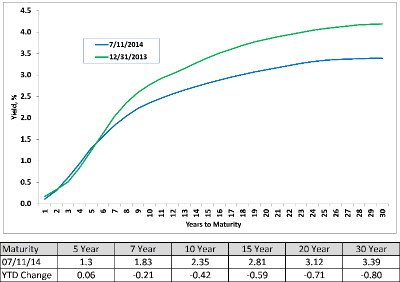

AAA Municipal Market Data (MMD) Yield Curve

Source: Thomson Reuters

Weekly Municipal Mutual Fund Flow Data

Source: Lipper AMG Data

Taxable

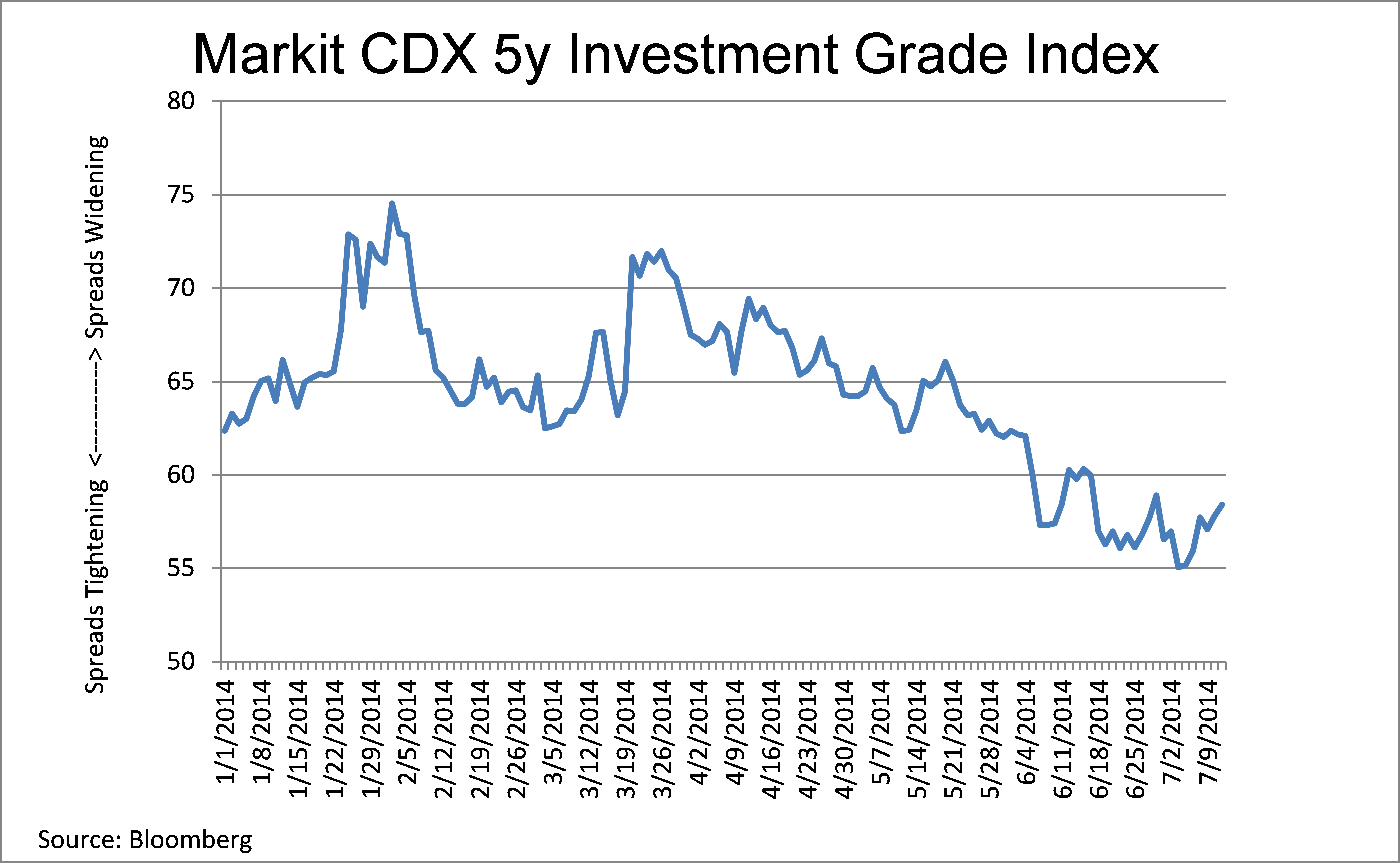

Though interest rates were able to rally last week, investment grade credit spreads actually widened, on average, 2 basis points across all sectors. With second quarter earnings season set to escalate this week, we expect a fairly subdued new issue market for corporate debt. As such, we expect market direction to be dominated by activity in the secondary market and the dealer community. The most recent data from the Federal Reserve Bank of New York shows dealers holding $14.2b of investment grade bonds and notes on their books—a near 100% rise from April.

With the first six months of 2014 now in the books, high grade debt has returned a respectable +5.68% according to Barclays, outperforming taxable high yield debt (+5.46%).

© 2014 Castleton Partners, LLC. All rights reserved.

THE FOLLOWING NOTES AND DISCLOSURES ARE AN INTEGRAL PART OF THIS REPORT: Past performance is not a guarantee of future results. Different investments involve varying degrees of risk, including the risk of illiquidity and the risk that you could lose part or all of your investment. There can be no assurance that the future performance of any specific investment, investment strategy, or product (including those discussed herein or recommended or undertaken by Castleton Partners, LLC) will be profitable, equal any corresponding indicated historical performance, be suitable for your portfolio or individual situation, or prove successful. Charts, graphs and indices are included herein only for reference and do not constitute forecasts of the past or predicted future performance of any investment. Indices are not investments. Due to changing market conditions and other factors the content herein may no longer reflect Castleton Partners, LLC’s current opinions or positions. Nothing discussed herein is or is intended as tax, legal, accounting or personalized investment advice from Castleton Partners, LLC. Should you have any questions regarding the applicability of any specific issue discussed herein we encourage you to consult competent advisers of your choosing. Nothing herein is or is intended as an offer to sell or a solicitation of offers to buy any security. Castleton Partners, LLC’s current written disclosure statement including discussion of our advisory services and fees is available upon request.