One axiom that has been used over the last couple decades is that high tide lifts all boats; meaning that a rise in economic or market conditions will lift every component of an economy or market to some degree. While true, we deal with relative measurements when discussing returns comparable to a benchmark. So, while the high tide does lift all boats, if the boat is tethered too tightly, you may be higher than being beached, but you also could still be underwater.

Philosophically speaking, this tightness of a tether could be defined as fiscal policies, judicial precedent, accommodating central banks and demographics for broad-based economic comparison. It could also be defined as cash flow, new innovation in products, prudent fiscal management and efficiency in manufacturing for how high a company’s equity might rise relative to a high tide of increased growth.

One area of the global arena that appears to be in the beginning stages of a higher tide (after a very elongated low tide) is in China. There are a multitude of reasons that we are beginning to see some signs that we feel investors should be paying attention to, even if there are still some headwinds to the long-term structural challenges. To be fair, the challenges are in place for every country, as the relative nature of pursuing growth always shines light on those areas that may ultimately hold it back. Recall the negativity bias written about a few months ago which should help put in the proper light how we read and focus on certain viewpoints while disregarding others.

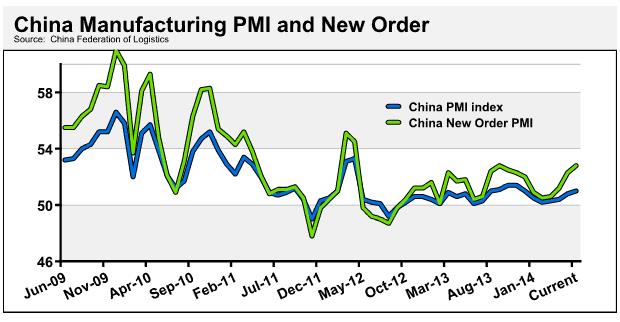

On the manufacturing front, the Purchasing Managers Index (PMI) has now been slowly increasing from the 50 level to 51 on its most recent reading. Anything over 50 is seen as expansionary. The “glass half full” investor will see this as a positive, while the pessimist will cite that this is below the five-year average of 51.3. However, we saw a spike in new orders – and more importantly – leading indicators show a 52.8 level which is well above the five-year average. Below is a chart from the last four years (end of the recession in the United States) used to take out the anomalistic low prints of 2008, due to skewing.

We also have seen some “benign” inflation prints in China recently. We see some pseudo-stimulus packages being utilized in the form of rail projects and a continuing push to drive more domestic consumption. This should allow them to have a more diverse economy rather than relying on exporting their way to prosperity, which puts them into heavy competition across the globe as the push for devaluing currencies continues form emerging markets and developed markets.

There also is an improving trend that helps with the domestic consumption push in the form of net wealth being created according to the BCG Global Wealth Report:

- In 2013, there were 2.378 million “millionaire” households in China. Second only to the United States that had “millionaire” households totaling 7.135 million.

- This is roughly 33% of the United States’ total; while China’s gross domestic product is running at nearly 82% of the United States. This would corroborate an increasing rising level of millionaires in China relative to the United States in the foreseeable future.

- The combined amount of wealth rankings from the United States and China will see 38% growth in the next four years, with 84% of that growth coming from China.

- According to the report, by 2018, the Asia-Pacific region – excluding Japan – will be the wealthiest region in the world.

One seasonal pattern we discovered in looking at the last 10 years is the substantial outperformance in the Shanghai Composite in the second half of the year relative to first half of the year. The average price return of the Shanghai Composite since June 2003 has averaged 5.3%. Consider the breakdown of the returns of the first half relative to second half and on an average and median value.

|

1st half |

2nd half |

|

|

3.4% |

7.2% |

Average Return |

|

-3.2% |

6.9% |

Median Return |

(Source Shanghai Stock Exchange)

This week we have the Strategic Alliance discussions between the United States and China which will focus primarily on the currency trading and restriction set in place by China, though there will be other topics discussed. It brings to light the symbiotic likeness of the relationship between the United States and China, as well as the challenges in moving both countries forward. However, recent measurements and historical trends point to a continued favorable investment long term in China.

This commentary is for informational purposes only. All investments are subject to risk and past performance is no guarantee of future results. Please see the disclosures webpage for additional risk information.