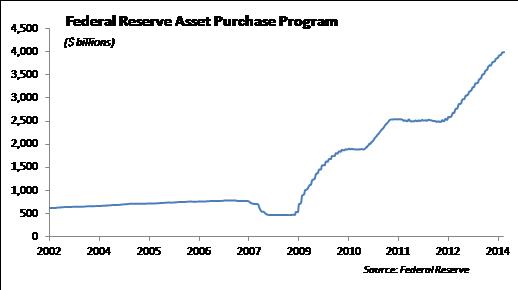

During the Financial Crisis, as the capital markets seized up and interbank lending froze, traditional tools of monetary policy proved ineffective. The Federal Reserve implemented a series of initiatives called Quantitative Easing that essentially used the central bank’s balance sheet to purchase bonds in the open market and directly manipulate interest rates lower. This tool proved extremely powerful and allowed the Fed to manipulate interest rates across the yield curve which, in turn, allowed for a wave of refinancing activity that helped to lower borrowing costs. While the success of the Fed’s Quantitative Easing programs is being debated, there is no doubt that many of the initiatives the Federal Reserve took during the Financial Crisis helped to keep the capital markets functioning in the face of an impaired banking system. The Fed has amassed a portfolio of $4.0 trillion through its purchasing activity. Now the Fed is in the process of curtailing its open market purchase activity which we expect will substantially come to end by the end of this year. The Fed has admitted that they are in new territory and they haven’t formulated a plan for the next steps for monetary policy. Quantitative Easing has acted as an anesthetic for the capital markets, helping to suppress volatility. As the Fed removes the blanket of monthly asset purchases, we expect that volatility will increase. This paper discusses the potential for increased volatility in the capital markets in the second half of the year and the potential for increased private credit expansion in the economy today as the Fed curtails its asset purchase program.

Volatility in the Capital Markets is Expected to Increase

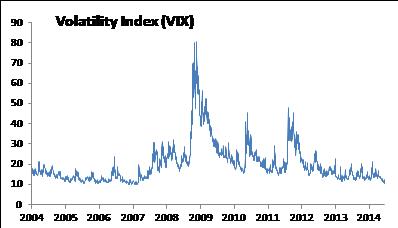

As the Federal Reserve blanketed the capital market with liquidity through its Quantitative Easing programs following the Financial Crisis, we experienced a dramatic decline in volatility across domestic capital markets. Volatility in the bond market has been running between 6% and 8% over the period following the Financial Crisis and now rests below 3%. Similarly, volatility in the S&P 500 (measured by the VIX) was running between 18% to 20% over the same period and is now coming in below 12%. That’s a fancy way of saying that investors aren’t being adequately compensated for the risks in publicly traded securities going forward.

The Federal Reserve announced in June that they would be decreasing their monthly asset purchase program another $10 billion in July down to $35 billion per month. These open market purchases of U.S. Treasury and mortgage-backed securities are a form of direct market intervention which has helped to lower interest rates, increase investor confidence, sustain commerce and support stock prices. Now, as the Federal Reserve eases out of its open market purchase program, we expect investors will be faced with an increase in the level of volatility in the market. While the economy is limping along at 2% growth the Fed is concerned that an abrupt withdrawal of its open market support will have a negative impact on economic activity. The Fed is not in the process of tightening monetary policy; it is in the process of making it less easy.

As the Federal Reserve removes its direct support of the capital markets, it is critical for private credit expansion and business formation that the banks increase lending. In this ambiguous world where the Dodd-Frank Act rules are still not fully formulated and implemented, we do not believe the banks are as incentivized to make loans and take risk. As a result, the next few years will be important to investors as the Dodd-Frank rules are finalized and fully implemented, we have more clarity on bank lending activity, and security valuations in the capital markets adjust back to levels without the support of the central bank.

Traditional Role of Banking under the Glass-Steagall Act

A healthy financial system is a requirement for sustained growth in an economy. The banking system is the backbone of the financial system and an extension of the Federal Reserve in the implementation of monetary policy. Prior to the repeal of the Glass-Steagall Act in 1999 banks were in the business of taking in deposits and making loans. The Glass-Steagall Act mandated a separation of traditional banking from other business activities including investment banking, capital market and insurance activities. As interstate banking laws changed in the 1980s and 1990s, banks searched for additional sources of revenue and pushed the boundaries on traditional banking activities by setting up investment banking divisions, capital market groups and insurance operations. The business model for banking began to look like a mega-supermarket instead of a more focused neighborhood grocery store. Ultimately, this search for profit compromised the financial system, contributing to the Financial Crisis in 2008 and forced the Federal Reserve to implement new tools to support credit and lending activities.

The banking system, which was severely undercapitalized leading up to the Financial Crisis, was effectively bailed out through the TARP program. Our capital markets have been forced to weather many changes since the Financial Crisis including the Dodd-Frank Act, regulatory reform, and Quantitative Easing. As a result of Dodd-Frank and Basel III, banks have been forced to increase capital levels and curb risk taking. We believe that the banks are less incentivized today to make loans and put their capital at risk following the repeal of the Glass-Steagall Act and the implementation of the new Basel III capital requirements since they have other businesses that they can emphasize to produce revenue.

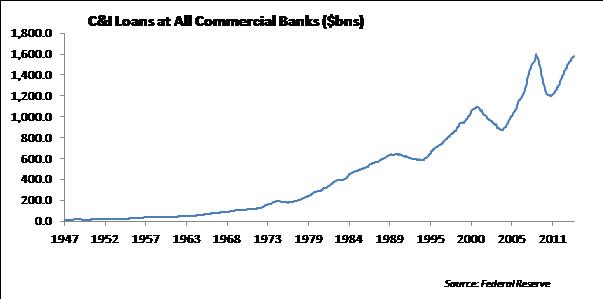

In addition, this focus on replenishing capital is having a negative impact on private credit expansion and economic growth. According to the U.S. Census Bureau business formation is running 30% lower than the annual rate in the 1980s. One of the contributing factors is that banks have been reluctant to lend to small and medium-sized businesses which is the bedrock of the economy. The Fed’s recent announcement that it will make the annual stress tests more rigorous will likely have a compounding effect on private credit expansion.

Banks exist to extend credit and provide a safe haven for savers. They do this by taking in deposits and making loans to consumers and businesses. In the good old days the central bank would manipulate the Fed Funds rate (which is the rate that banks would lend to each other) as a way to increase or restrict credit flow. In turn, this would impact capital market activity and economic growth as changes in interest rates impacted borrowing costs. This worked in a system where banks managed risk and made a profit by making loans. However, today large banks are essentially closed distribution systems where the business model appears more interested in cross selling products to a captive client base and making loans with the primary intent of selling them into the street and taking out fees.

In this post-Glass-Steagall marketplace banks have more ways to earn a profit other than putting their capital at risk by making a loan. At the same time, the regulatory environment remains overly punitive which is acting as a deterrent for banks to make loans, particularly for small businesses.

The Federal Reserve’s Monetary Policy Tools

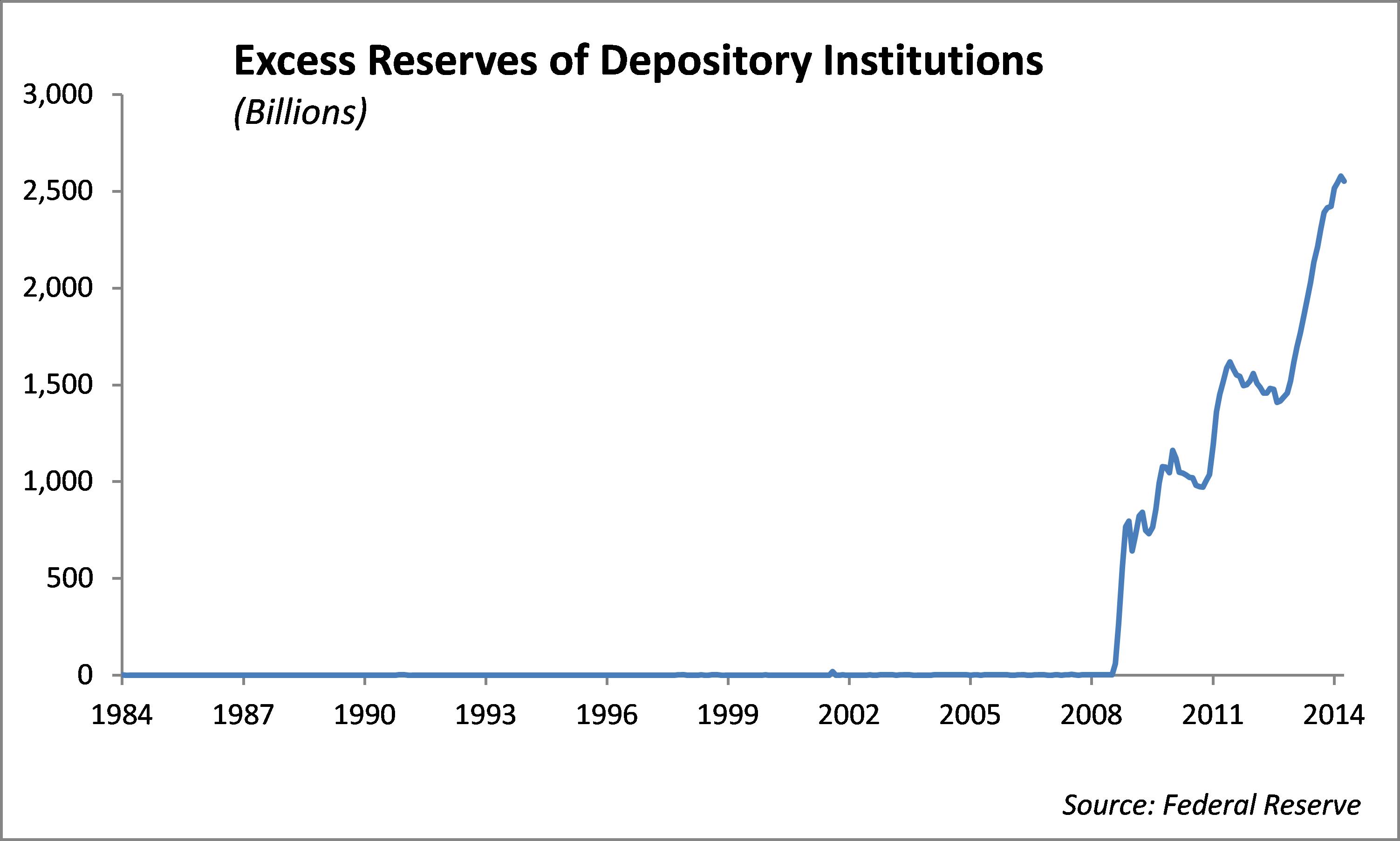

Many of the businesses that banks were legally allowed to enter after the repeal of the Glass-Steagall Act, including insurance, trading, asset management and investment banking, do not require significant capital levels to compete. With a more laissez faire regulator, banks were able to increase their leverage over a more diversified revenue base leading up to the Financial Crisis in 2008. During the decades of the 1980s and 1990s the Federal Reserve manipulated the flow of credit by adjusting the supply of money in the system and the interest rate that banks would lend to each other. The capital markets experienced healthy private credit expansion during this period. As a result of the Financial Crisis and the need to recapitalize the banking system, the tools that the Federal Reserve has used to incentivize the banks to extend or contract credit have effectively been neutered. Manipulating the Fed Funds rate to fight inflation or marginally impact economic growth will not work since commercial banks have over $2.5 trillion in excess reserves. With access to all these excess reserves banks don’t really need to borrow from each other right now.

Today our capital markets are effectively operating under a huge experiment of policy initiatives that have never before been attempted on a large scale by a central bank. The Federal Reserve has moved beyond tools that manipulate the supply of money in the system or target interest rates that banks charge to lend to each other. The Fed has been forced to implement a new set of tools that result in open market purchases of securities to manipulate the level of interest rates along the yield curve. As a result of the asset purchase programs, the Federal Reserve has built a portfolio of securities that approaches $4.0 trillion and interest rates are near historic low levels. We are nearing the point when the Fed will curtail its open market purchase activity.

The Federal Reserve is primarily focused on policies that support modest inflation and increase job growth. However, it is clear to us that the Fed does not want to disrupt the capital markets in a way that would negatively impact economic growth. Inflating asset prices has been a critical initiative for the Federal Reserve since it has a strong correlation to consumer confidence and spending. The Federal Reserve has pretty much indicated that it will ultimately let short term interest rates rise but is in no hurry to move in that direction. However, we are more concerned about the potential for increased volatility in the markets.

The Implications for Investors

Proper asset allocation requires the calculation of both expected horizon returns and expected volatility for each asset class included in the portfolio. Over the past five years, realized volatility has come in below our expected volatility for most of the major equity and fixed income asset classes. We believe the decline in volatility is, in a large part, due to the effect of the Fed’s Quantitative Easing programs. As the Federal Reserve built a $4.0 trillion bond portfolio by purchasing $85 billion in securities each month over the past three years, volatility declined sharply. We expect there will be several consequences in the capital markets as the Federal Reserve contemplates curtailing its asset purchase program.

First, we expect volatility will increase in the capital markets. Without the anesthetic of the central bank’s asset purchase program the capital markets will once again transition back to allowing free markets to set the level of interest rates. This will likely be a bumpy transition beginning in the second half of 2014.

Second, we expect the range of interest rate movement will increase from the narrow range we’ve experienced in the past three years. We expect the 10 year US Treasury will trade in a yield range of 2.50% to 3.60% over the next twelve months.

Third, fundamentals will begin to matter for valuing securities trading in the U.S. equities market. Stock prices will revert back to being evaluated based on the companies’ underlying fundamentals and no longer based on the excessive availability of liquidity provided by the Fed.

Fourth, the Fed will sit on its $4.0 trillion portfolio and let it run-off. This will mitigate any dispersion and allow for an orderly decline in US Treasury borrowings to further fund asset purchases.

Fifth, the Fed will slowly reduce the level of interest rates that it pays for banks to hold excess reserves on deposit at the central bank. This is the critical factor in both credit expansion and inflation. During the financial crisis, the Fed began to pay banks 25 basis points for holding excess reserves on deposit with the central bank. This compensated the banks in a manner sufficient to pay depositors and, in our opinion, has served as a direct subsidy to the banking system. We expect, as the Fed curtails its QE program that it will reduce the interest it pays on reserves as an incentive for the banks to make loans. The challenge is that if the banks increase credit too quickly, there is a heightened risk of acceleration in the rate of inflation.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data. © 2014 Winthrop Capital Management