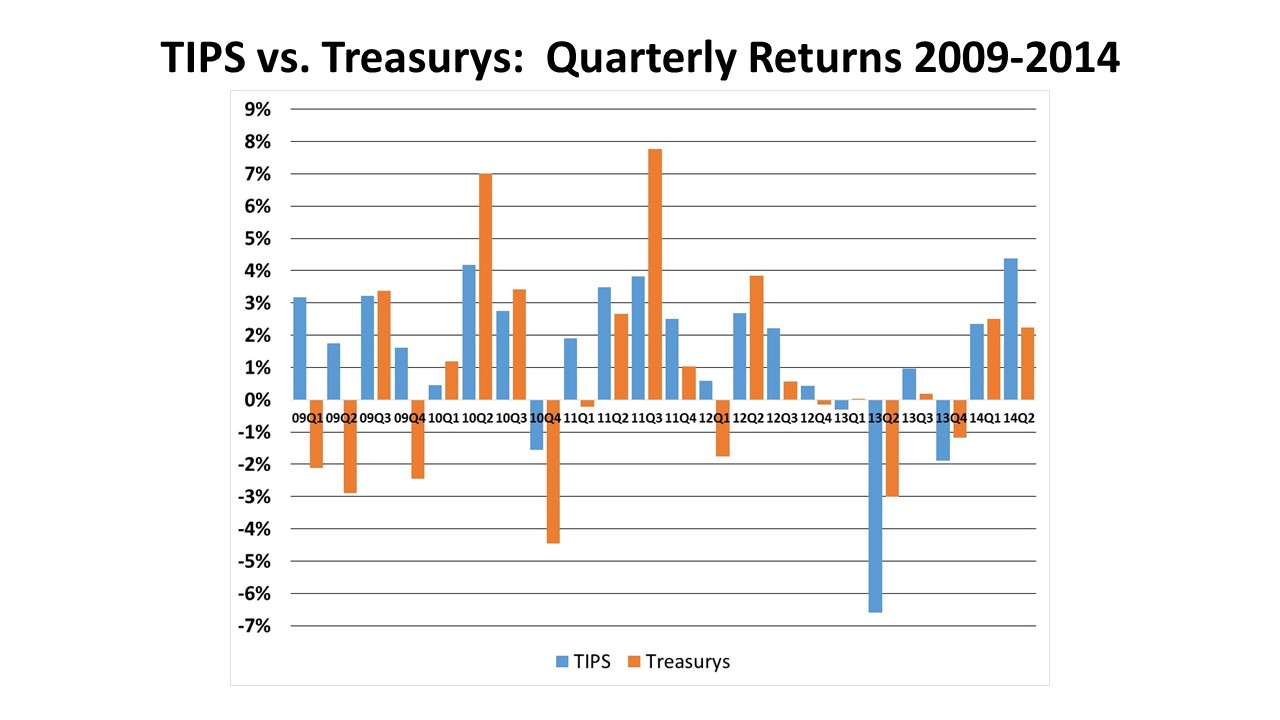

· TIPS posted gains of about 4% in the 2014 second quarter, better than the 2.2% gain in comparable maturity straight Treasury securities.

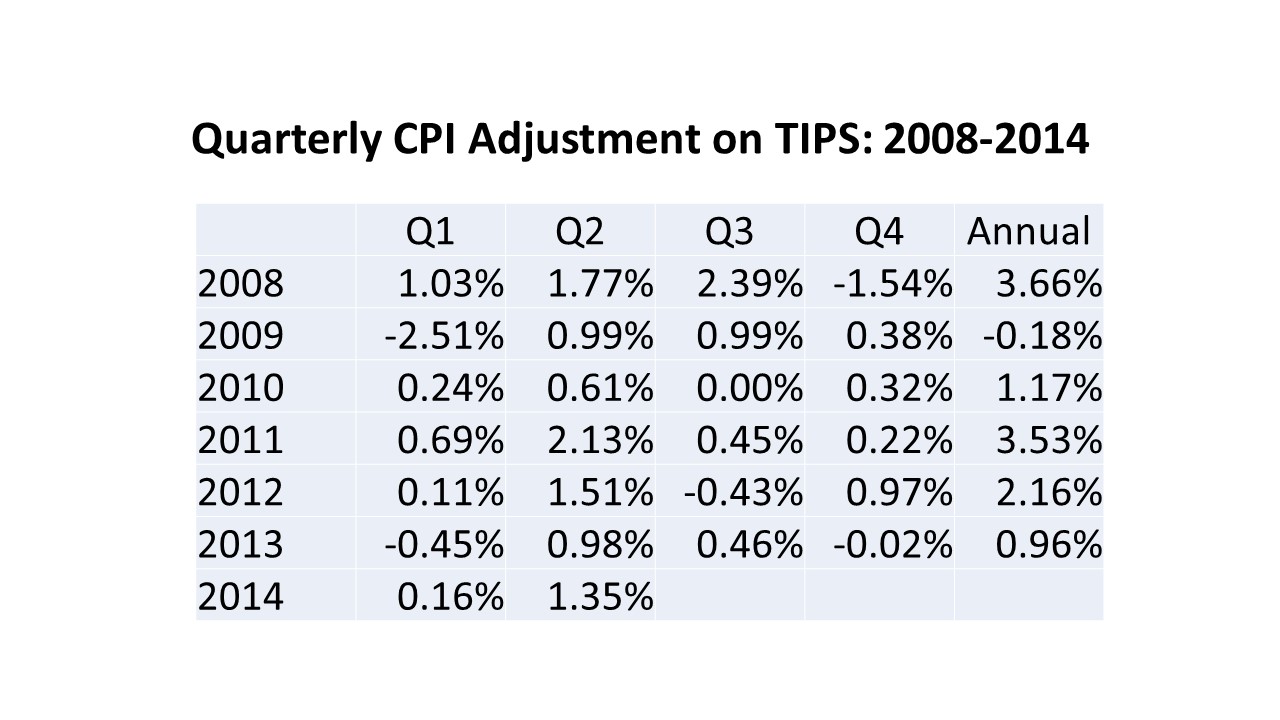

· Most of the excess return this quarter was due to the CPI adjustment of 135 bp, the best in two years.

· TIPS can outperform Treasurys in two ways: 1) if the actual inflation adjustment is positive or 2) if inflation expectations, as measured by the TIPS spread, rise.

TIPS have been on a tear so far in 2014. While returns on straight Treasury securities have been strong, TIPS returns have been stronger. After scampering away from Treasurys last year out of fears about the winding down of Federal Reserve stimulus, bond investors seemed reassured, after the weak first quarter GDP report and statements by the Fed, that interest rates are not about to rise anytime soon.

Yet, the recent economic data seem confirm that the weak first quarter GDP was a speed bump. Employment growth has been solid. Manufacturing activity has picked up. Even housing market activity has recovered modestly from a disappointing spring selling season. By all accounts, this should have raised investor concerns that interest rates will begin to rise sooner than expected.

So what gives? I will look at the numbers and return to this question later.

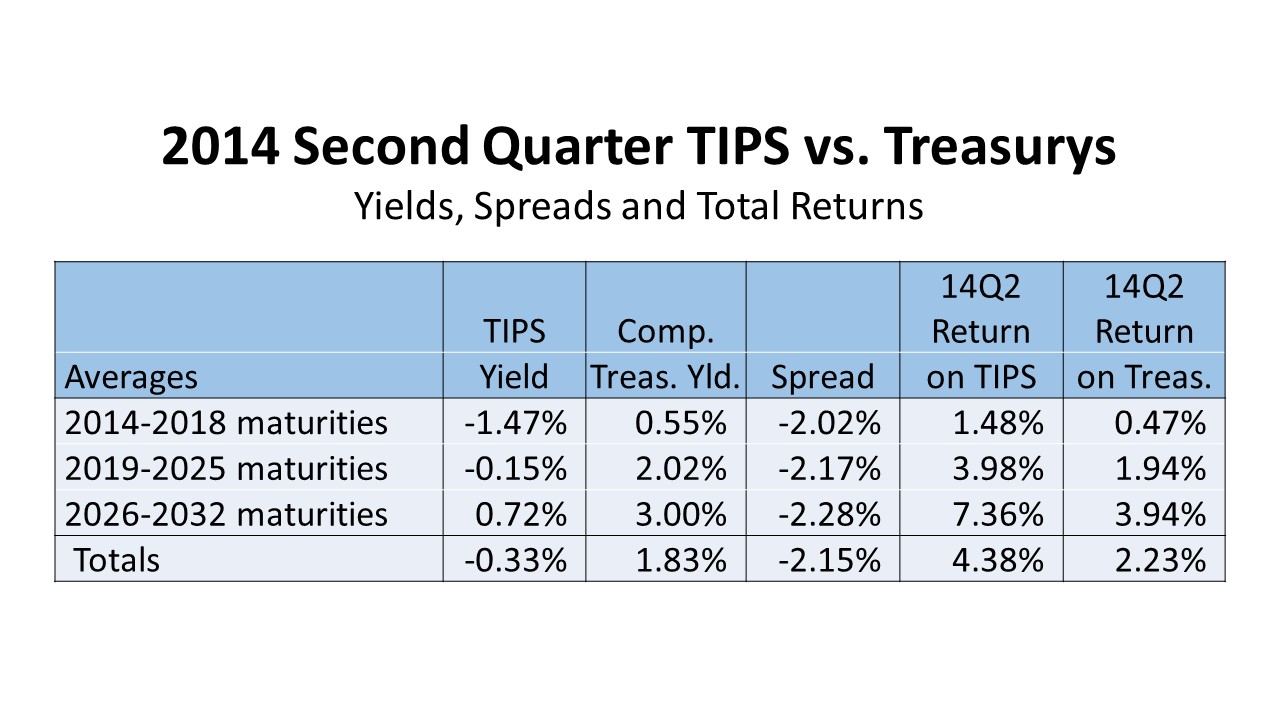

According to my calculation methodologies, TIPS posted a total return of 4.38% in the second quarter much higher than the 2.23% earned on comparable maturities Treasurys. The calculated return on TIPS is sometimes skewed by the returns on newly issued TIPS that experience outsized returns. In this case, when the return on the 30-year TIPS bond issued in February 2014 is excluded, the average return on long maturity TIPS (i.e. 2026-2032 maturities) falls to 6.68%, 68 bp below the 7.36% return reported above, and the average total return on all TIPS drops to 3.99%, 39 bp less than the 4.38% return given above.

Even with this adjustment, the difference between the 3.99% return on TIPS and 2.23% return on Treasurys seems pretty big. It is explained by two factors: First, the inflation adjustment – the added return from the change in CPI - was 135 basis points this quarter. This was the biggest quarterly CPI adjustment in two years, as shown in the table below:

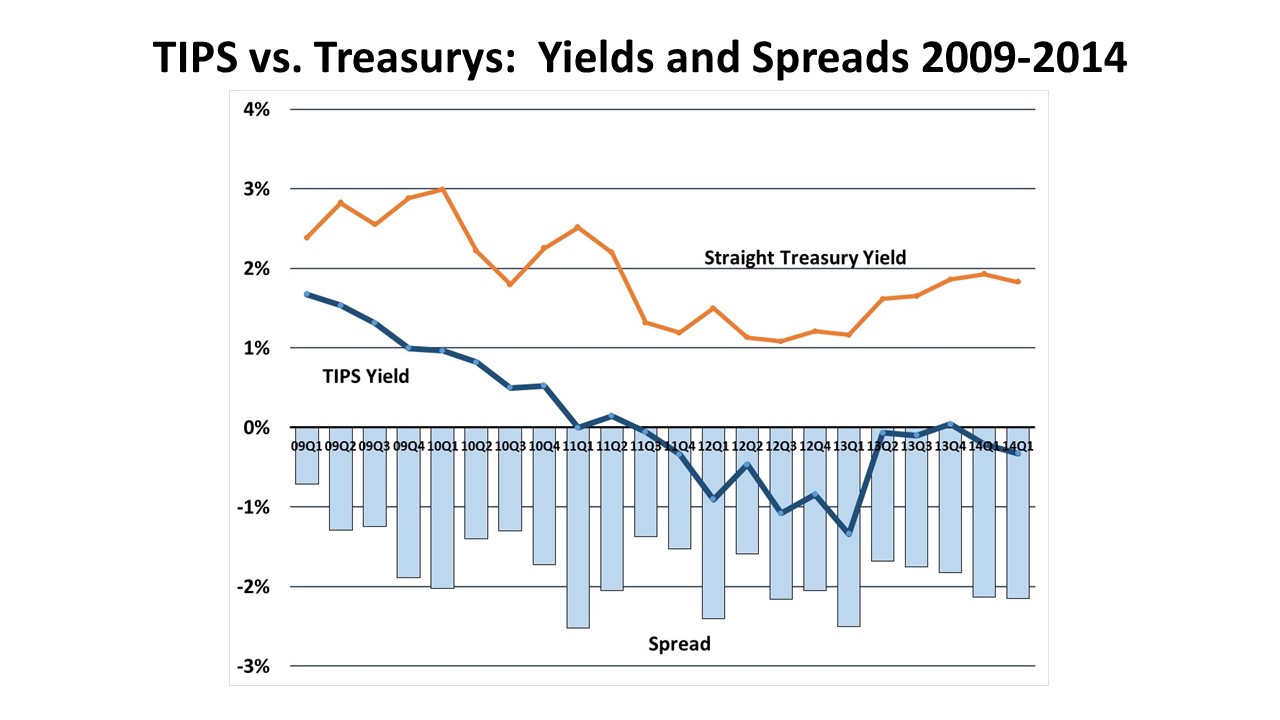

The second component of the return is simply straight bond performance. If the return on the straight TIPS bond exceeds Treasurys, then TIPS yields are falling faster that Treasury yields. This is evident in the widening of the TIPS spread (i.e. the difference in yield between TIPS and comparable maturity straight Treasury bonds).

In the 2014 second quarter, the TIPS spread widened to 215 bp from an adjusted 207 bp in the first quarter. In both cases, the TIPS spread was adjusted to exclude both TIPS bonds issued and those that matured during the quarter.

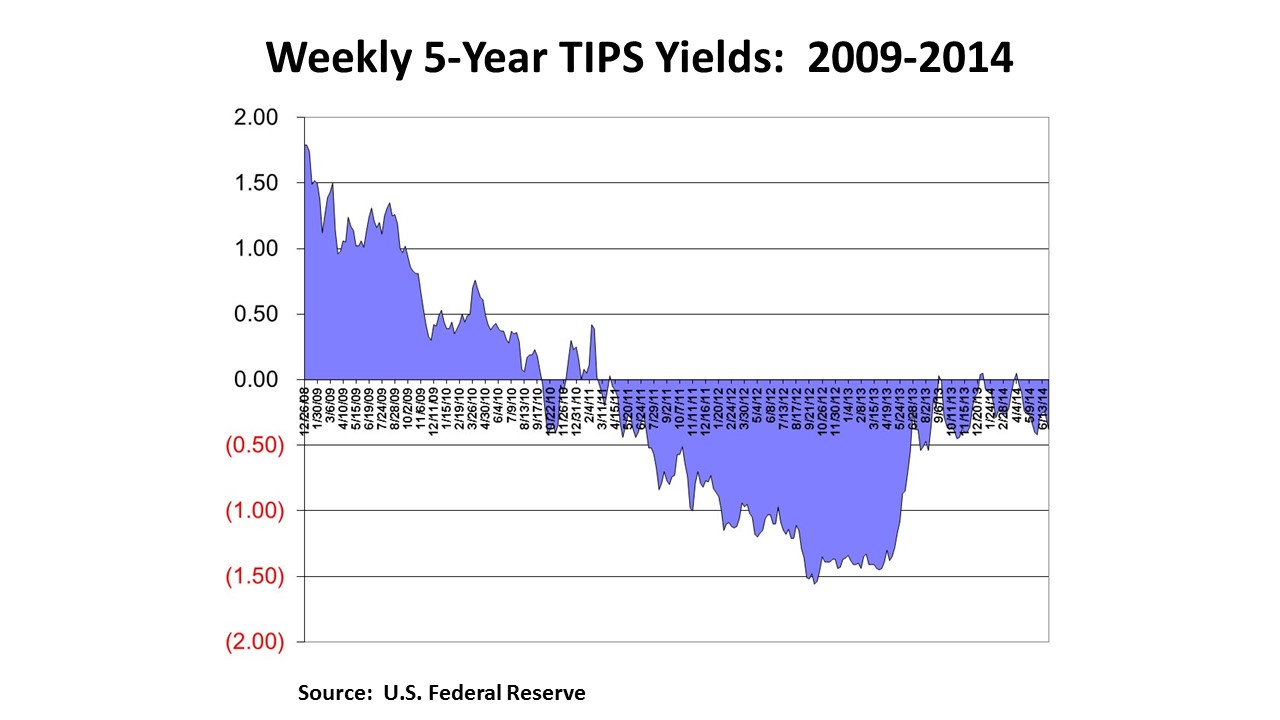

Since TIPS yields rebounded from historically low levels just about one year ago, they have mostly been range bound. The 5-year TIPS yield has been fluctuating between ‑0.35% and 0.00% for the past year.

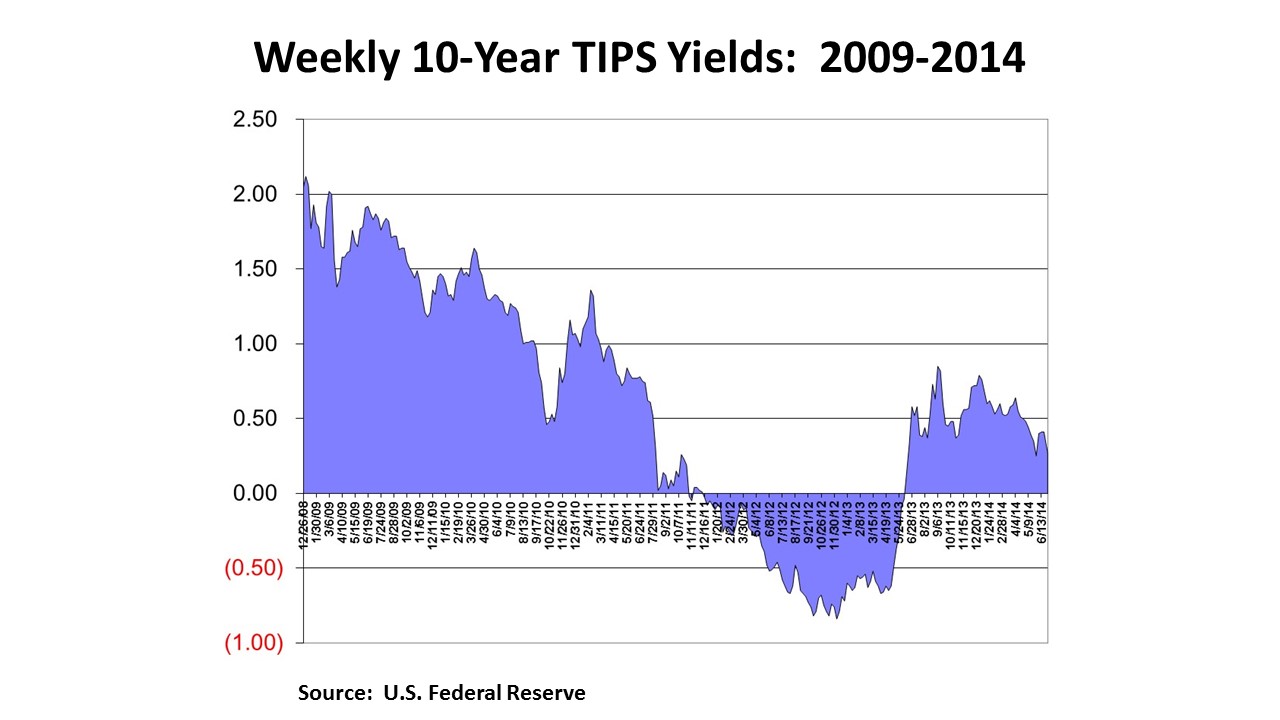

The 10-year TIPS yield has also fluctuated around 0.50%, but it has been on a modest downtrend since the fall of 2013.

The decline in both TIPS and Treasury yields has produced solid returns for both in 2014, quite a contrast from returns in 2013:

After ending a long slide in the summer of 2013, TIPS and Treasury yields rose sharply; but they have been sliding back in 2014. With the gyration in yields over the past five years or so, the spreads between TIPS and Treasury yields have fluctuated between 100 bp and 200 bp. In normal times, the spread has been around 200 bp. The spread did approach zero during the financial crisis (apparently on expectations that inflation would be near zero for quite some time), but it has not risen above 250 bp in recent times.

Going forward, the performance of TIPS will be governed by the interplay between interest rates and inflation. TIPS have usually lost money (i.e. their yields have risen) during periods of rising rates. This was the case when rates began to rise sharply one year ago. All of this has happened, however, during a period of “well-anchored” inflation expectations and low actual inflation.

If inflation expectations rise, then, all other things being equal, TIPS should outperform straight Treasurys. Straight Treasury yields may rise, but if TIPS yields rise less, then TIPS would outperform Treasurys. In this case, investors would be less likely to sell TIPS, because inflation expectations are increasing. The spread between Treasury yields and TIPS would widen.

Alternatively, if there is no change in the TIPS spread, but actual inflation is positive (or increasing), then TIPS will outperform Treasurys through the added return of the CPI inflation adjustment, which is added to principal.

So positive actual inflation and rising inflation expectations, as measured by a rising TIPS spread, will cause TIPS to outperform Treasurys. However, if interest rates rise sharply, more than inflation expectations, it is possible that TIPS investors could realize negative returns, even though TIPS might still outperform Treasurys (i.e. the losses on TIPS would be less than those on Treasurys).

Turning back to the question of why TIPS and Treasurys have continued to outperform, despite the improvement in the economy and the stock market: There are a few possible explanations. First, the financial markets may be adjusting to the “new normal,” the term coined by Bill Gross of PIMCO to describe an environment where interest rates remain well below levels previously thought to be normal, because growth in the economy remains sluggish for an extended period of time.

Second, the strong performance of both stocks and bonds simultaneously could be a function of too much money sloshing around the financial system. Cash might be invested anywhere, without necessarily any regard for whether such movements can be explained rationally. Furthermore, the combination of a higher stock market and lower interest rates is consistent with Fed policy, given its focus on trying to sustain and accelerate economic growth.

Third, it is also possible that either the stock market or the bond market have it wrong. Either the economy is much weaker than high stock prices would seem to suggest (in which case, the stock market will before too long suffer a correction) or the bond market is underestimating the potential strength in the economy and therefore the risk of a rise in interest rates. Time will tell.

FYI, in the first half of 2014, I estimate that, excluding newly issued TIPS bonds, TIPS have produced an average total return of about 6.4%, compared with an average return on comparable maturity straight Treasurys of 4.7%. This solid return places TIPS among the best performing subsectors in the fixed income market so far this year.

July 2, 2014

Stephen P. Percoco

Lark Research

P.O. Box 768

Norwood, MA 02062

(781) 762-1476

[email protected]