Treasury yields fell across the maturity spectrum last week, with longer dated maturities recording the largest price gains relative to shorter dated bonds and notes. With geopolitical concerns continuing to weigh heavily on investors’ minds, interest rates were propelled lower on the surprising revision to the 1st quarter GDP and the resulting downward revisions to 2nd quarter GDP estimates. GDP fell to -2.9%, a massive drop far in excess of the -1.8% consensus—the biggest quarterly decline in five years. Consumption data—namely, a consumer burdened by flat wage growth and rising food, energy, and heath care costs—was the chief reason for the decline in economic growth. FOMC consensus for GDP growth in all of 2014 is expected to be +2.5%. Knowing that the first six months were well below expectations, the US economy will need to see growth accelerate to the 5%+ range in the second half of this year to meet those expectations—a seemingly unlikely event.

In general, trading and conviction in interest rate markets has been lacking, as a bevy of unknowns (geopolitical, policy, mid-term elections, economic data) has kept volumes low. The reality is that not much is looming on the horizon until we get to Federal Reserve Chair Janet Yellen’s testimony to Congress in mid-July. Though stock and bond market volatility has sunk to near all-time lows, the prevailing strategy for most has been a bias to overweight spread and/or risk assets. With complacency at a potentially worrisome level, we remain mindful of liquidity as we enter the second half of a year in which fixed income has been strong.

Tomorrow brings the 1st of July—a concept that seemed but a dream last winter—in a holiday shortened week. As such, the Bureau of Labor has moved up the release of the monthly jobs report to Thursday from Friday. Expectations are for +215k jobs added in June.

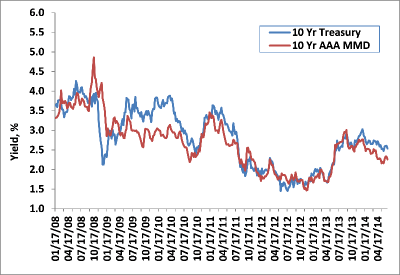

Weekly Change: 10Y Treasury Yields vs. 10Y AAA MMD

Source: Bloomberg, Thomson Reuters and Castleton Partners

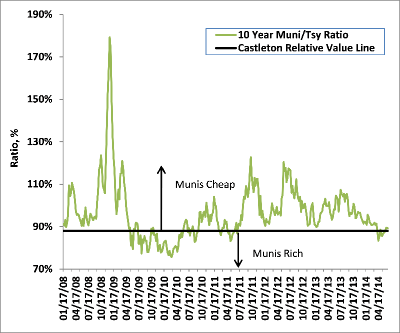

Ratio of 10Y Municipal Yield to 10Y Treasury Yield

Source: Bloomberg, Thomson Reuters and Castleton Partners

Tax-Exempt

Tax exempts registered another constructive week, with benchmark yields in ten year and thirty years falling 8 and 9 basis points, respectively. Over $8 billion of new debt was easily absorbed, as investors began planning for July’s expected $43 billion (Bloomberg) of principal and coupon payments. With interest rates surprisingly lower through the first half of 2014 relative to expectations, tax exempt credit preference has been biased towards lower investment grade debt and below. As June comes to a close, the Barclays Municipal high Yield Index continues to trump all domestic fixed income sectors year to date, with a return of +7.95%. With the “risk on” trade still very much in vogue, yields on taxable high yield debt have fallen to an all-time low—making municipal yield opportunities increasingly more attractive. In fact, the Barclays Taxable High Yield Index has fallen to an all-time low yield of 4.90%—or just 2.77% when factoring in the top federal tax rate of 43.4%!

Two of the biggest issuers in tax exempt land—California and Puerto Rico—continued to make headlines last week, though for opposing reasons. California received its long overdue credit upgrade from Moody’s, rising to Aa3 from A1. The upgrade reflects the state’s rapidly improving financial position and high, but declining, debt metrics. Moody’s action affects over $86 billion of outstanding debt.

As for Puerto Rico, Governor Padilla signed into law last Thursday the Puerto Rico Public Corporations Debt Enforcement and Recovery Act, essentially a legal framework allowing for the restructuring of certain of the Commonwealth’s public agencies. This new bill explicitly allows the debt-laden and resource-draining, P.R. Electric & Power Agency (PREPA), P.R. Aqua & Sewer Agency (PRASA), and the P.R. Highway & Transportation Agency (PRHTA) two paths to work with creditors in addressing their financial conditions. This surprising action has caught the tax exempt market by surprise. Though still a developing situation, the above referenced credits have registered sharp price declines, while P.R. general obligation has recorded minor price improvements. Together, these three agencies (PREPA, PRASA, PRHTA) account for about 40% of the roughly $73 billion in Puerto Rico debt and are chiefly responsible for the explosion of Island debt over the last ten years. Though not specifically labeled a bankruptcy law, the objective of this new filing is to allow these agencies the ability to restructure, while preventing creditors from moving against the assets of these public corporations with the intention of liquidation to satisfy their claims.

General obligation debts of the Commonwealth, as well as sales tax bonds (COFINA), are explicitly and specifically excluded from this bill and the ability to restructure. Though still developing, pundits believe this new bill is designed with the Electric & Power Authority (PREPA) in mind. Solely reliant on oil for generation, PREPA’s balance sheet is in dire straits, with several lines of credit and debt maturities coming due in July. With limited access to capital, PREPA has been relying on the P.R. Government Development Bank (GDB) to pay its bills. Reducing energy costs is the single most important element to generating better economic growth on the Island. In principle then, a restructuring of PREPA that reduces energy costs and reduces reliance on the GDB is good for growth and GO debt.

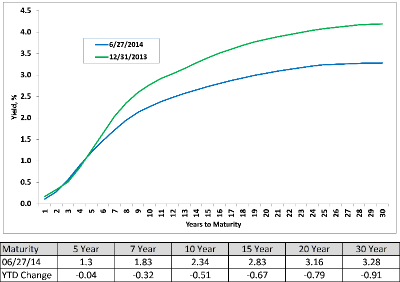

AAA Municipal Market Data (MMD) Yield Curve

Source: Thomson Reuters

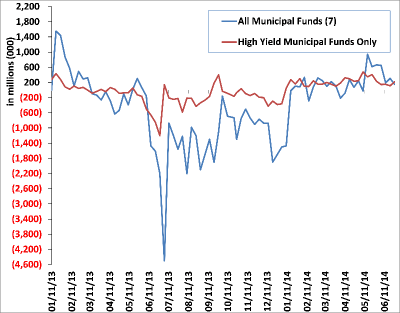

Weekly Municipal Mutual Fund Flow Data

Source: Lipper AMG Data

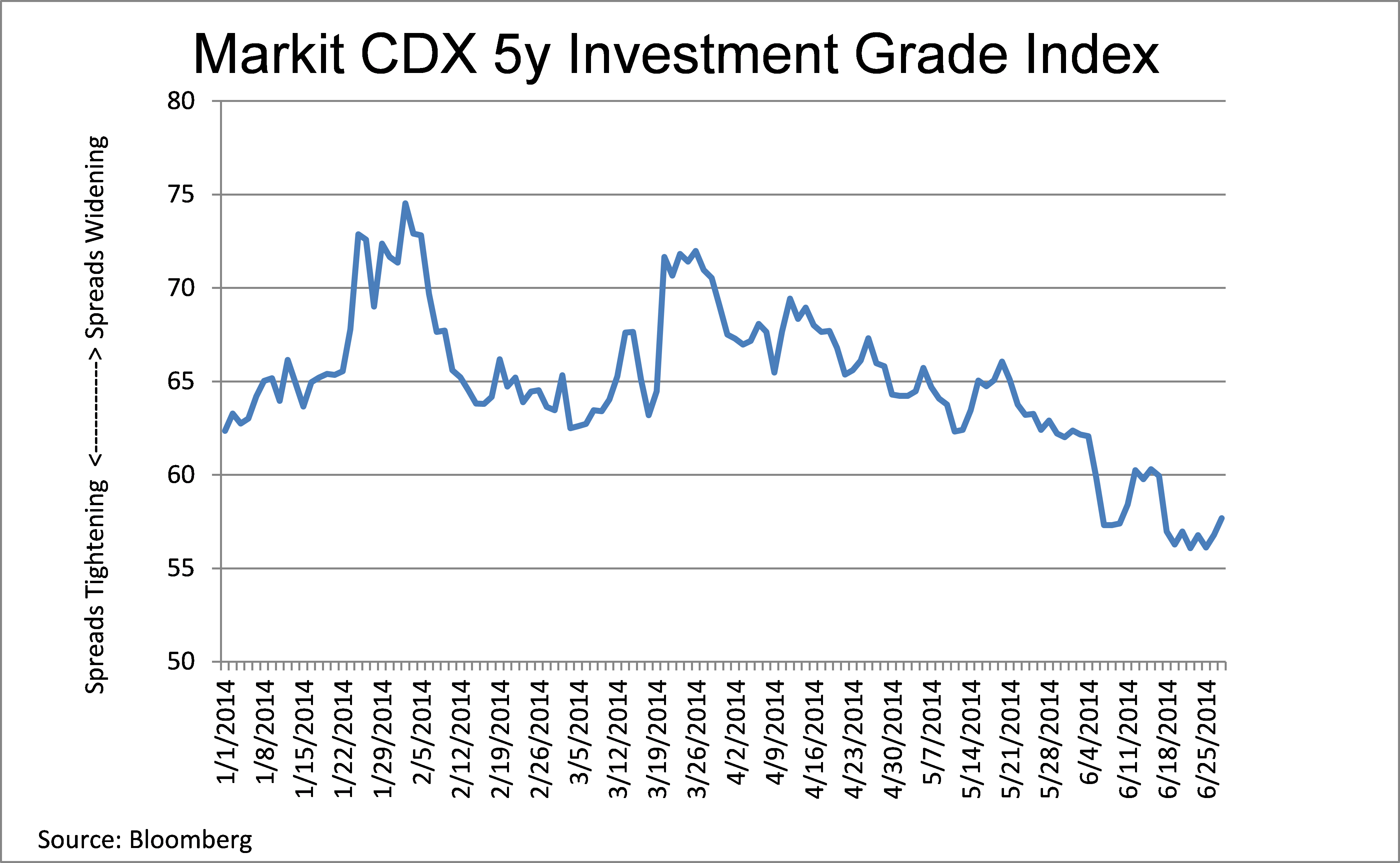

Taxable

An environment of low volatility and positive technicals remained in place last week, propelling investment grade corporates tighter yet again relative to Treasury rates. Most sectors were able to grind out gains of 2-4 basis points, as high grade bond funds recorded another +$2.4b of new cash in the lightest supply week of June. Financials led all issuers with $7 billion of new debt last week.

Corporate bond performance so far in 2014 has been favorable, with all sectors posting excess returns for the first half of the year. Though Castleton reiterates our neutral view on investment grade spreads—believing current levels offer little protection should rates rise—we accept the fact that the search for yield and any excess carry may continue to push credit spreads tighter. Additionally, we remain concerned over the increased activity in mergers and acquisitions (M&A), particularly the rationale behind some of the deals and the re-leveraging of balance sheets in a world of “cheap financing.”

Due to the Independence Day holiday, there will be no Weekly Market Update next week.