Oil prices and energy security have once again come back into the spotlight as the Islamic State of Iraq and the Levant, the group known as ISIS, has taken control over parts of northern and western Iraq. To date, the impact on oil prices has been fairly muted, but any escalation of violence could pose a serious threat to the stability of global oil markets and has a wide range of implications for future OPEC crude supply growth.Â

No material supply disruptions so farÂ

Since the violence began a few weeks ago, the attacks have been focused mostly in the northern and western parts of the country; a safe distance from the southern region where the majority of Iraq’s production is located. While over 90% of Iraq’s exports are from the south, the Iraq-Turkey pipeline in the north has been offline since March when it was attacked by insurgents. This has reduced exports by approximately 200,000 barrels per day and since the pipeline passes through ISIS-controlled territory, it is likely the repairs will be delayed. Additionally, some evacuations of non-essential expatriate personnel have begun. The rise in oil prices is largely a reflection of the increased risk of future outages, not a reaction to any lost physical volumes.Â

Iraqi oil production: present and future

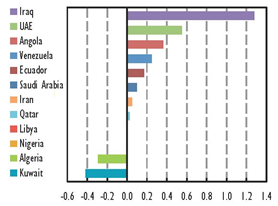

Iraq is OPEC’s second largest oil producer at 3.3 million barrels per day (mb/d), after Saudi Arabia; nearly 80% of which is exported. The majority of Iraq’s production is in the south (2.6 mb/d), with 0.5 mb/d in the north and output of 0.25 mb/d from the Kurdistan Regional Government (KRG). The IEA’s most recent medium term oil outlook forecasts Iraq’s production capacity to reach 4.5 mb/d by 2019 from 3.3 mb/d during 2013, accounting for over 60% of OPEC’s growth. Baghdad’s own projections are considerably more ambitious, with production expected to reach 8.5-9 mb/d by the end of the decade. However, Iraq could fall short of this trajectory with prolonged violence which could have a material impact on the global crude supply-demand balance especially as it comes at a time when global unplanned crude oil outages exceed 3.3 mb/d, driven by downtime in Libya, Iran, Iraq, Nigeria and several non-OPEC nations.Â

Incremental OPEC crude production capacity 2013-19 (mb/d)

Â

Â

Short-term Risks – Can Saudi Arabia offset additional supply losses?Â

In May, Saudi Arabia produced 9.7 mb/d, leaving a spare capacity cushion of 2.8 mb/d to offset any further supply disruptions. The Kingdom has repeatedly assured the market that it can produce at or above its technical capacity of 12.5 mb/d if required. Despite these assurances, the market remains skeptical Saudi Arabia can maintain production over 10 mb/d for a significant length of time. Even if no additional supply is required as a result of the current unrest, Saudi Arabia’s domestic consumption this summer, in addition to the current unplanned outages abroad will require it to maintain production above the 10 mb/d level for likely the longest period in more than 30 years. Should any additional supply shortfalls emerge from Iraq, or elsewhere over the next few months, Saudi production would need to ramp up considerably higher than 10mb/d.Â

What are the implications for oil-levered equities?Â

Prior to the recent events in Iraq, many equity investors were expecting oil prices to decline over the next few years as a result of growing North American onshore production, higher availability in the MENA region (i.e., less unplanned outages) and increased production capacity from Iraq and other OPEC members including Angola and the UAE. However, with Iraq accounting for the majority of OPEC’s production growth over the next several years, the market has started to rethink long term supply-demand dynamics and adjust commodity forecasts which underpin the earnings and cash flows of energy companies. Of note, North American energy companies are generally more levered to domestic crude prices, and given the current U.S. export ban on crude oil, they are somewhat less sensitive to changes in the Brent oil price stemming from geopolitical tensions.Â

What are the implications for oil prices?Â

While oil prices have increased only modestly over the past few weeks, prices for Brent crude oil still remain at a 9-month high. Despite the day-to-day volatility, prices remain within the $105-$115 per barrel range; in line with the quarterly average price for Brent we’ve seen in 7 of the past 8 quarters. U.S. gasoline prices remain somewhat elevated at approximately $3.68 per gallon but well within the $3.25-$3.95 per gallon range we have seen since unrest began in Libya in 2011. Any further escalation in the region especially if accompanied by any lost physical volumes, would have a more dire impact on the price of oil and could lead to demand destruction and possibly lower global economic growth.Â

Longer term oil prices also face upward risks, as the market has been expecting strong production growth from Iraq which may now be in jeopardy. Any prolonged turmoil in the region could result in a curtailment of the additional investment required to meet the country’s long-term production goals.Â

DisclosureÂ

The views expressed are as of 6/30/14, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.Â

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.Â

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.Â

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.Â

© 2014 Columbia Management Investment Distributors, Inc. All rights reserved.Â

953542