With the US S&P 500 Index and Dow Jones Industrial Average advancing into record territory this year and some European equity benchmarks likewise nearing new highs, some investors may be wondering whether it’s still wise to be jumping into the market at this stage. Lisa Myers, executive vice president, Templeton Global Equity Group, thinks that a long-term investment horizon, supported by bottom-up analysis, can reveal hidden value. Myers also thinks that regardless of the market cycle, there could be opportunities to be had, particularly when taking a global view with a balanced approach that considers different sectors and asset classes.

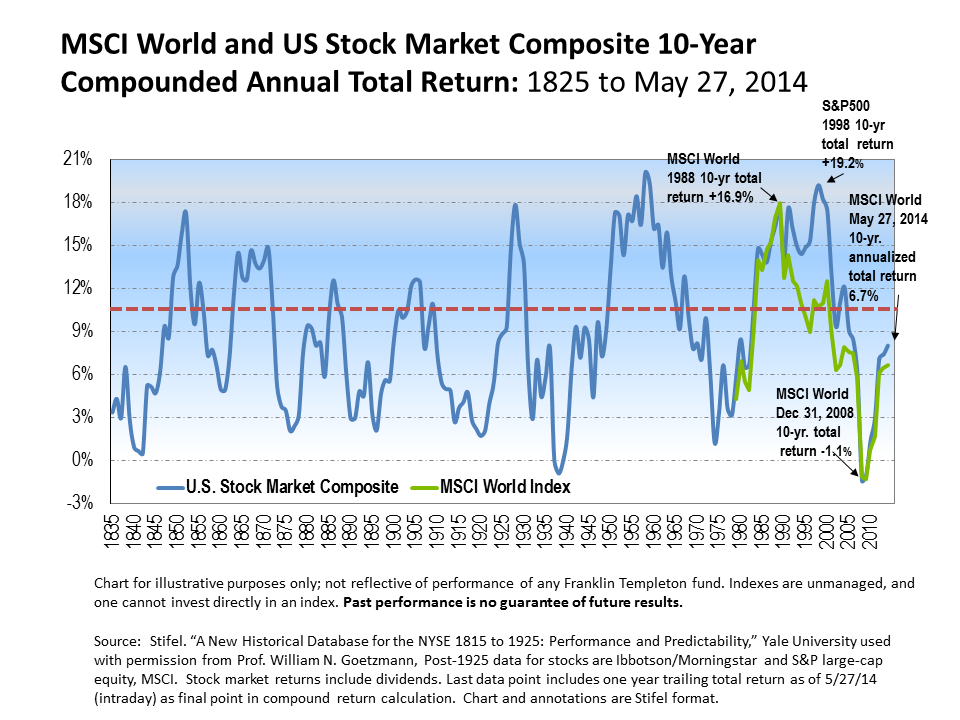

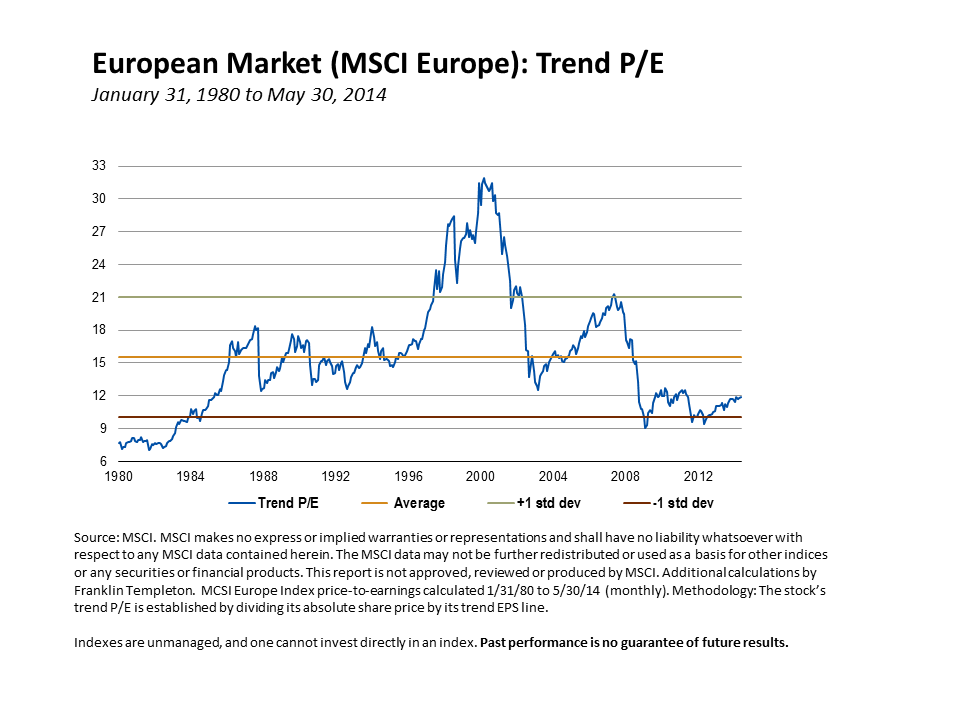

Global equity markets, led by the US, have continued to recover from their lows hit during the 2007-2008 financial crisis. To assess the potential for further gains, I find it useful to take a longer-term perspective. On a 10-year basis, whether looking at the US or the global market as a whole, annualized total returns are still below historical averages. On a trending basis, equity valuations still don’t look very expensive to us, either on a price-to-earnings (P/E) basis or on a price-to-book (P/B) basis.1 In fact, they’re still not back to their historical averages.

We think the global recovery that the US economy appears to be leading may be sustainable for several reasons. Within the US, a critical aspect of any recovery in our view is consumption, which accounts for 70% of US GDP.2 In this regard, the US consumer has deleveraged, and savings rates have come up substantially since the 2007–2008 financial crisis.3 The rebound in US equity markets since then has enabled household wealth to recover, in tandem with the housing market. And yet, looking at the US housing market today, it still isn’t driving the economy to the extent it had been before the crisis. We think there’s more housing market recovery potential to come. Meanwhile, unemployment levels have fallen substantially, energy prices are low and the US continues to enjoy low inflation. So we think this bodes well for a further recovery in the US.

Some would argue that the strength of the US economy has made the US market more expensive than the rest of the world. By most market metrics, advances in US equities do seem to reflect the economic recovery there, which is further advanced than in most other developed nations.

Europe’s recovery has lagged the US, in large part due to the fiscal austerity measures that were introduced in some of the hardest-hit countries in the European Union (EU) as a condition for receiving bailouts. However, we think Europe may be turning the corner. In fact, we have been interested in European equities for the past couple of years because we have seen them generally trading at such a substantial discount to the US and to their own history.

We are particularly excited about the investment prospects in Europe, given that European equities still have not experienced a corporate earnings recovery as we have seen in the US. In contrast to the US, operating margins (the proportion of a company’s revenue remaining after paying for variable costs of production) in Europe have not yet recovered strongly. Many have tried to blame this on structural reasons such as inflexible labor markets, higher taxes or some other factor specific to Europe. However, considering historical data, this has not been an impediment to European companies in the past. In our view, as Europe’s economy starts to recover, we will likely see European earnings recover.

The significant amount of cash on corporate balance sheets is one of the factors that gives us confidence that there may be more room for global equity markets to perform well.4 It provides companies choices, including whether to invest to expand their businesses, to pay higher dividends, or to buy back shares. All of these options potentially increase earnings and returns. Companies could also invest to improve technology, which drives productivity and earnings growth.

As long-term, bottom-up investors, we go to places where the catalysts for improvement may not yet be clearly visible. We look at a time horizon of at least five years and invest where others often may not because we are willing to be patient to recognize the potential value that our analysis reveals. As we look around the world at where we are finding values now, financial stocks stand out to us. In the US and Europe, a lot has happened in the banking sector since the financial crisis. In the US, banks have deleveraged and restructured, bad loans have been written off or have recovered. Therefore, banks are starting to provision less and profits are starting to improve. US banks are also starting to see some loan growth.5 European banks are slightly behind in this process, but are appearing to show similar improvements. We believe very little of this seems to be reflected in current valuations because the sector remains so out of favor.

Oil services are another area we like for similar reasons. Energy company share prices have been under some pressure from expectations of increased oil supply in the future, as well as less productive capital investment for exploration and development by large integrated oil companies. Conversely, oil service companies have continued to benefit from many of the recently discovered oil and gas reserves, which require increasing levels of technology and services to extract. That said, when there are concerns about oil prices in the global markets, oil service company shares tend to suffer. In the past couple of years, we have taken advantage of these market conditions. When many are focused on near-term issues, we have looked to buy into some of what we believe are premier oil service companies like Halliburton6 and Baker Hughes7 and more recently some names in Europe, which we feel should be the beneficiaries of structural changes in the industry for years to come.

Based on all the exciting investment opportunities we are seeing in global equities, it should not be surprising that the current Templeton Global Balanced Fund allocation is 70% equity today and 30% fixed income.8 We actively allocate between the two asset classes on the basis of fundamental bottom-up research. We do not try to generate a fool proof macro-economic view which directs our investments between and across each asset class. Instead, we assess the opportunity set in each asset class and where our analysis of valuations and risk suggest we can seek strong long-term risk adjusted total returns, including an income component.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

All investments involve risks, including possible loss of principal. Special risks are associated with foreign investing including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds in the fund adjust to a rise in interest rates, the fund’s share price may decline. The risks associated with higher-yielding, lower-rated debt securities include higher risk of default and loss of principal. To the extent the Fund focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a fund that invests in a wider variety of countries, regions, industries, sectors or investments. The fund’s investment in derivative securities, such as swaps, financial futures and option contracts, and use of foreign currency techniques involve special risks as such may not achieve the anticipated benefits and/or may result in losses to the fund. The fund’s risk considerations are discussed in the prospectus.

Investors should carefully consider a fund’s investment goals, risks, sales charges and expenses before investing. The prospectus contains this and other information. Please read the prospectus carefully before investing or sending money.

1. The price-to-earnings ratio, or P/E ratio, is an equity valuation multiple defined as market price per share divided by annual earnings per share. The price-to-book ratio is another valuation multiple calculated by dividing the stock price by the difference of total assets minus intangible assets and liabilities.

2. US Bureau of Economic Analysis, © 2012.

3. Federal Reserve Bank of St. Louis, Economic Research.

4. Source: Moody’s.

5. Source: Board of Governors of the Federal Reserve System.

6. Halliburton Co. common stock represents 0.99% of total net assets of Templeton Global Balanced Fund, as of 3/31/14. Holdings subject to change.

7. Baker Hughes Inc. common stock represents 0.91% of total net assets of Templeton Global Balanced Fund, as of 3/31/14. Holdings subject to change.

8. As of 4/30/14. Holdings subject to change.

© Franklin Templeton Investments

© Franklin Templeton Investments