A Brief Note on Gold as a Defensive Asset

Ade Odunsi is the Managing Director for Treesdale Partners and portfolio manager of the AdvisorShares Gartman Gold/Euro ETF (GEUR), AdvisorShares Gartman Gold/British Pound ETF (GGBP), AdvisorShares Gartman Gold/Yen ETF (GYEN) and AdvisorShares International Gold ETF (GLDE).

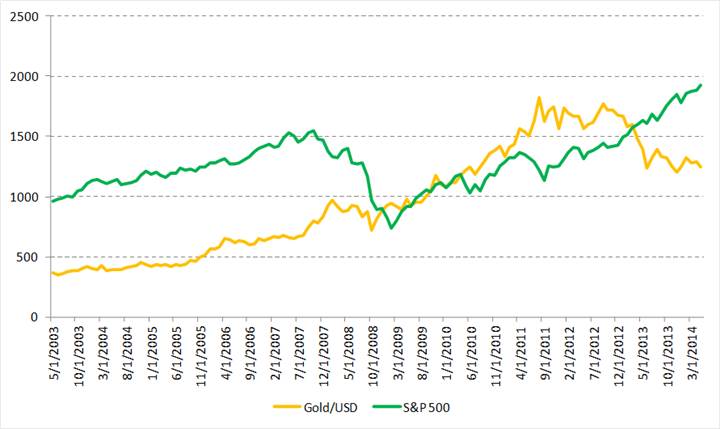

In previous notes we have written about the defensive nature of gold relative to the broad equity market. Much of the discussion has focused on the low correlation and beta of gold versus equity markets. In fact, the ten year monthly returns of gold (priced in US dollar terms) and the S&P 500 show a correlation of zero with the beta of monthly gold returns versus S&P 500 returns also being essentially zero (0.1). With a low and fairly stable correlation the diversification benefits of adding gold to a portfolio are evident – as has been noted in many discussions on portfolio strategy, the diversification benefit of adding an asset to a portfolio does not come from adding many different assets to the portfolio but rather from adding assets to the portfolio that are shown to have low correlation to the portfolio constituents.

Source: Bloomberg LP

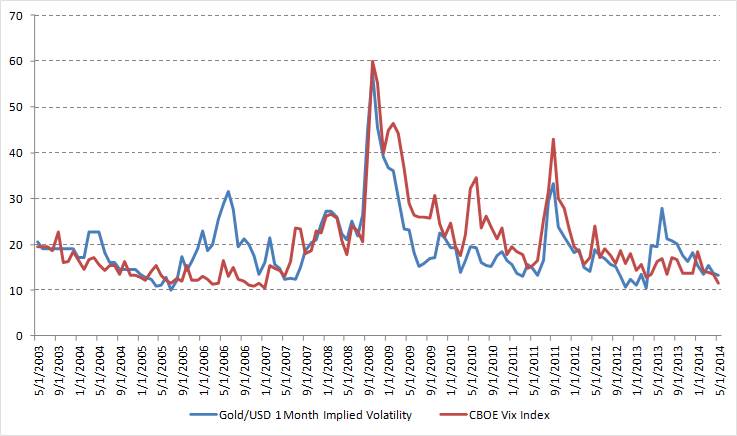

A key factor however that must also be taken into consideration is the expected price volatility of gold relative to the expected price volatility of the existing portfolio. For ease of illustration we will focus on equities here and look at price volatility as implied from option prices. When options are traded, the dollars and cents cost of the option can be used to imply the markets’ expectation of future market volatility – the higher the option price, the higher the expectation of future volatility. This expectation of volatility is expressed as an annualized, percentage standard deviation. For example, if the implied volatility for a 1 month option is 11%, this would indicate, approximately, the market’s expectation for the potential movement (within a 1 standard deviation range) in the gold price over the next month, but expressed on an annualized basis.

In the chart below the CBOE VIX Index (the market’s expectation of short-term equity market volatility) is plotted along with the expected volatility, as implied from one month gold option prices, going back over the last 10 years. The striking feature of the chart is the strong relationship, both on an absolute and relative basis, between the markets’ expectations for short term volatility. Typically rises and falls in expected volatility in one market are mirrored in the other indicating that both markets share risk factors that drive the respective market’s expectations of future volatility. But not only is there strong correlation between changes in expected volatility between the two markets, the chart shows that the absolute level of expected volatility in both markets has also tracked each other. The price volatility of gold has been akin to the price volatility of a broad based, large capitalization equity index.

Source: Bloomberg LP

Taken together these charts show us that gold in relation to equities has little or no correlation of returns but high correlation of price volatility. So how does this relate to portfolio construction? Despite the low correlation of gold to equities, it is also critical to consider the volatility of an asset in determining its effectiveness as a defensive asset. In a nutshell, gold has historically been as volatile, if not more volatile, than equities. During periods of high risk aversion in equity markets when gold has typically been sought out as a defensive asset, the chart shows that it has in fact been extremely volatile. Adding an asset such as gold to a portfolio, despite its apparent low correlation, requires care as its high volatility hints at the potential for large swings in NAV. Which brings us to perhaps the key consideration which many investors factor into their weightings when adding gold as a defensive asset; namely an expectation that the gold price would be expected to outperform as investors seek out the “safety” of gold during periods of high stress. With low correlation but high volatility, a positive expected return for gold would likely raise the efficiency of a typical portfolio in a mean-variance optimization framework.

We should stress that our intention is not to dissuade investors from the defensive properties of adding gold to a portfolio but rather that it is important to consider its correlation, volatility and expected return, relative to the overall portfolio as part of the asset allocation process.