The June FOMC meeting contained a little bit for everyone and interest rates reacted only marginally after the announcements. But looking across asset markets—including nominal and inflation-linked bonds, equities, commodities and the dollar—it’s clear that investors interpreted the news as another dovish surprise from the Fed. We are not sure that is the correct interpretation, and the reason comes down to the issue of “data dependence”. The FOMC’s forecasts and Yellen’s comments in the press conference could indeed have reacted more to recent news. But we saw enough evidence of data dependence yesterday to remain convinced that policy will turn more hawkish as inflation and unemployment gaps close.

Central bankers often say that policy is “data dependent”, but it’s not immediately clear what they mean by that phrase. One should hope that at some level monetary policy always depends on the outlook for the economy, so emphasizing data dependence can seem like stating the obvious. Nevertheless, we think there is in fact an important concept here.

Data dependence is not a black or white issue. Rather, the responsiveness of monetary policy to economic data should be thought of as running along a continuum: sometimes policy responds hardly at all to incoming news, while at other times individual data points can have a major impact on the outcome of an FOMC meeting. The current QE tapering process would be an example of the former: the degree of data dependence is so low that policy is effectively on a preset course. An example of the latter would be the Fed’s rate hikes in mid-2006, when the committee was finessing the very end of a tightening cycle and every data point seemed to matter.

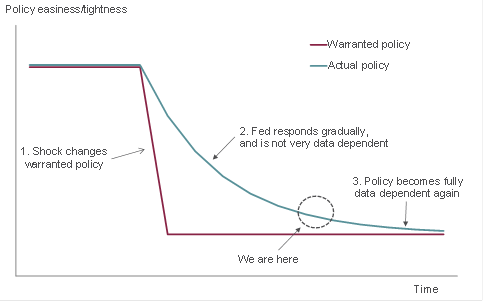

We think the reason that the sensitivity to incoming data varies over time is related to the practice of gradualism in central banking: the Fed responds only gradually to shocks, so there are times when policy is actually miscalibrated but on a glide path to a more appropriate stance. During that process committee decisions are not in fact very data dependent. Exhibit 1 visualizes this idea. First, a shock of some kind changes the warranted stance of monetary policy. Second, the Fed gradually moves the actual stance of policy to its warranted level over time. Lastly, when the two converge, policy becomes data dependent again.

Exhibit 1: Gradualism and data dependence

In the present context, we think the “shock” was a change of heart about how aggressively to use monetary policy to deal with labor market slack—in effect, the more dovish FOMC members won the argument (though this did not happen all at once). This led to a gradual recalibration of policy, during which time the Fed was not very data dependent. Instead of responding to incoming news, the Fed’s reaction function steadily drifted in a more dovish direction.

Bond investors need to know whether this process of moving the goalposts will continue or whether it has come to an end. At present, many observers believe that it will continue as Yellen’s views eventually dominate the committee. We disagree, and thought the critical part of the June FOMC meeting was the fact that the funds rate outlook once again responded to the decline in the unemployment rate. This evidence of data dependence suggests the period of shifting goalposts is ending.

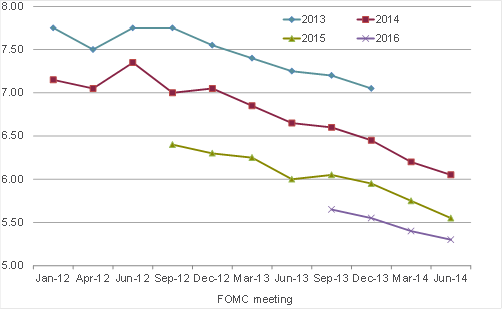

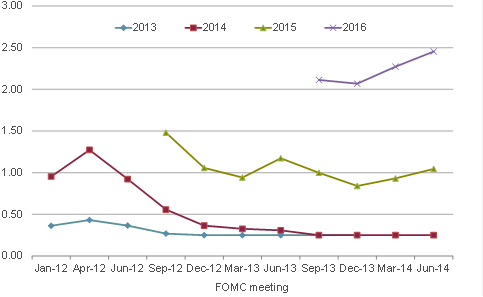

In Exhibits 2 and 3 we show the committee’s central tendency forecasts for the year-end unemployment rate and fed funds rate at the time of each FOMC meeting. Until this year, almost every forecast update involved lower unemployment forecasts and lower funds rate forecasts—i.e. a dovish shift in the reaction function. In contrast, at both the March and June 2014 FOMC meetings officials lowered their unemployment forecasts and raised their funds rate forecasts—despite cutting gross domestic product growth projections at the same time.

Exhibit 2: FOMC unemployment forecasts, central tendency (%)

Exhibit 3: FOMC funds rate forecasts, central tendency (%)

We can use these forecast changes to measure the degree of the Fed’s data dependency and compare them to some normal standard like the Taylor Rule. From December to June, the central tendency forecast for the 2015 unemployment rate declined by 40 basis points, and the central tendency forecast for the funds rate rose by 20 basis points. This implies a coefficient of 0.5, which compares to a range of 0.75-2.0 for standard policy rules used in the U.S. Thus, we can say that the data dependence of the 2015 forecasts still seems low (i.e. the liftoff date looks sticky). However, we see something different for the pace of rate hikes. From December to June, the 2016 unemployment rate forecast declined by 25 basis points and the funds rate forecast increased by 39 basis points, implying a coefficient of about 1.5. Thus, the response of the 2016 funds rate projection to recent data could be considered normal, and we interpret this as evidence that the Fed’s reaction function is (nearly) done moving.

Given our optimistic view on recent activity data and pessimistic view on the prospects for higher labor force participation, the odds still seem skewed toward a faster-than-expected normalization in the unemployment and inflation gaps. Plus, the June FOMC meeting gives us more confidence that this will elicit a response from the Fed—we are seeing sufficient data dependence. As a result, we remain cautious about exposure to U.S. interest rate risk, especially at the middle of the yield curve.

Disclosure

The views expressed are as of 6/23/14, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2014 Columbia Management Investment Distributors, Inc. All rights reserved.

953542