Iraq Crisis Impact on Oil?

Iraq Crisis Impact on Oil?

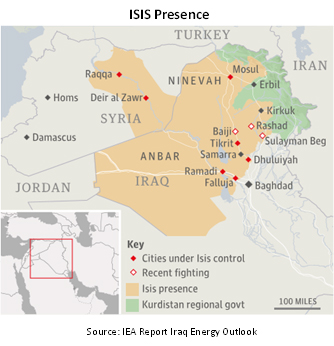

The rise and rapid expansion of the Sunni enclave known by its new rulers under Abu Bakr al-Baghdadi as the Islamic State of Iraq and al-Sham (or ISIS; al-Sham means greater Syria) comes as no great surprise. No-one can predict how far it can expand or how quickly it will be crushed (if ever).

Our tentative view is that it is reasonable to assume it will not be defeated any time soon, as support from the disaffected general Sunni Iraqi population will likely be considerable. This reflects the blatant sectarianism of Nouri al-Maliki, the Shiite Iraqi prime minister, since the US left Iraq two years ago. But it will likely be contained in the area it currently controls, and will rule over this area centered on Jazeera and covering much of Western Iraq and Eastern Syria for quite some time.

Current oil production in Iraq of perhaps 3.25 million barrels per day (b/d) includes roughly 150,000 b/d in the central region, which will likely be totally disrupted. The 700,000 b/d production in the north and 2.4 million b/d in the south, however, should be unaffected, provided the conflict does not expand seriously either through Baghdad or into Kurdistan. The immediate effect on oil supplies will therefore be the loss of 150k b/d.

An unexpected, balancing consequence may well be a settlement of the long-running Baghdad Kurdistan dispute and a commencement of unhindered exports of oil from Kurdistan. This depends, of course, on the relevant pipelines surviving and operating, but this is not so impossible as ISIS and Kurdistan, both Sunni, may choose to live in an uneasy acceptance of each other. This would, ironically, potentially release for export 150,000 b/d of shut-in production in Kurdistan.

If we are right, the immediate effect on world oil supply will be surprisingly modest. A more likely consequence is that the general uncertainty will greatly hamper efforts to grow Iraqi production in the south. The loss of a rise in Iraqi production and exports is enough to justify the current move up in the oil price by $5 per barrel, but there is no logical reason why it should rise much more.

Another consequence of this development may be to encourage the transfer of control elsewhere in the Middle East to similar extreme Islamic hands, e.g. in Libya. A major emerging figure there is Mohommad Zahawi, Islamisist leader of Ansar Al Sharia in the east of Libya, which is preventing any significant resumption of Libyan oil exports. On the other hand the emergence of murky ex-Gaddafi General Khalafi Haftar as a Sisi-like dictator (Egypt’s new dictator) may trump that.

One final consequence of a successful establishment of ISIS that should not be entirely discounted is the possibility it destabilizes Saudi Arabia. A recent press comment read as follows:

The kingdom has good reason to fear the revival of an al-Qaida-like group with wide territorial ambitions. The government claims to have broken up a terrorist cell in May that had links to both ISIS and al-Qaida in the Arabian Peninsula. ISIS has also reportedly launched a recruitment drive in Riyadh.

That would be really earth-shaking. No-one is discussing it, but if Saudi Arabia now turns against ISIS – a quite likely development – we should not rule out that ISIS survives and garners Wahhabi support inside Saudi Arabia and topples the monarchy. That would be disruptive.

Tim Guinness, Will Riley & Jonathan Waghorn

Guinness Atkinson Global Energy Team

Mutual fund investing involves risk and loss of principal is possible. The Fund invests in foreign securities which will involve greater volatility, political, economic and currency risks and differences in accounting methods. The Fund is non-diversified meaning it concentrates its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund. The Fund also invests in smaller companies, which involve additional risks such as limited liquidity and greater volatility. The Fund’s focus on the energy sector to the exclusion of other sectors exposes the Fund to greater market risk and potential monetary losses than if the Fund’s assets were diversified among various sectors.

Distributed by Quasar Distributors, LLC.

© Guinness Atkinson Asset Management