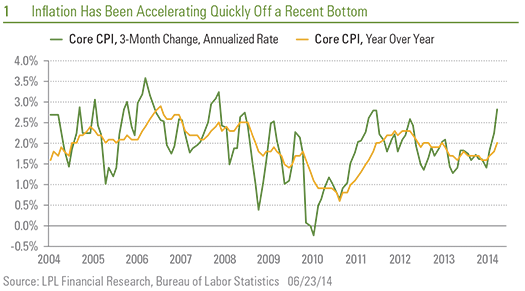

The term “behind the curve” has been used to describe a Federal Reserve (Fed) that is perceived to be late in lowering or raising interest rates in response to changing market or economic conditions. The most common use of the phrase is to describe the Fed as behind the curve on inflation. The Fed showed little concern over inflation during last week’s Fed meeting, despite the monthly consumer price index (CPI) report showing a continued rise in price pressures for May 2014 with recent gains accelerating [Figure 1].

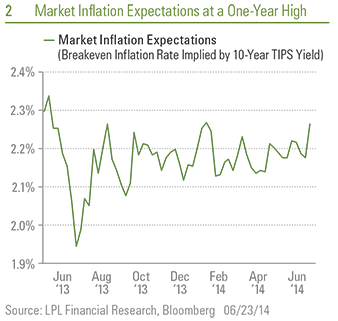

Fed Chair Janet Yellen downplayed the recent rise in inflation as likely “noise,” but the response still left investors questioning whether the Fed is behind the curve. Intermediate- to longer-term bond prices, which are most sensitive to inflation pressures, finished last week (June 16 – 20, 2014) slightly lower, and market expectations of future inflation, as measured by Treasury inflation-protected securities (TIPS), moved higher. The implied breakeven inflation rate on 10-year TIPS rose to near a one-year high [Figure 2] but is still very subdued when viewed in a longer-term context.

The yield curve also steepened last week, as intermediate- and long-term yields closed the week slightly higher, while short-term yields finished marginally lower. Short-term bonds benefited from the Fed’s cautious tone regarding the recent improvement in economic data, which allayed market fears that the Fed may move up its timing of a first interest rate increase. Longer-term bonds, on the other hand, focused on a modest increase in inflation risk. Bond market changes overall were minor, however. Although the bond market may be getting more worried about inflation, in the grander scheme of things it isn’t really that worried…yet.

The annualized change in the personal consumption expenditures (PCE) index -- the Fed’s favorite inflation measure -- will be a focal point the week of June 23, 2014. The core measure is expected to increase at a 1.5% annualized rate, which would put core PCE at the low end of the Fed’s 2014 year-end forecast range of 1.5% to 1.7%. Since the Fed chose to downplay recent inflation readings, economic data over the coming two to three months may help confirm whether the recent inflation trend may be more lasting. The limited reaction by the bond market so far suggests more proof is needed before bond prices may be pushed materially lower. Additional economic improvement and rising inflation may add to the June 2014 rise in yields, while mixed data may maintain the longer-term trading range defined by a 2.5% to 3.0% 10-year Treasury yield.

Inflation, and uncertainty around the Fed’s potential response, is one reason why the broad bond market, as measured by the Barclays Aggregate Bond Index, is down 0.5% month-to-date through June 23, 2014. Profit taking has emerged in June as low inflation, one of the drivers of bond strength during the first half of 2014, is beginning to fade.

The recent rise in inflation has made bond valuations more expensive as measured by inflation-adjusted, or real, yields [Figure 3]. The lower the real yield, the more expensive bonds are, and vice versa. The inflation-adjusted yield of the 10-year Treasury has increased slightly in June 2014 but remains near a one-year low after falling for most of 2014. With the Fed continuing to taper, inflation on the rise, and the economy improving, real yields are likely to resume their ascent and may pressure bond prices lower and yields higher.

Inflation can have a beneficial impact on lower-rated bonds, however. As inflation increases, the value of a company’s debt (issued during a period of cheaper prices) decreases while revenues come in commensurate with higher prices. Results are company specific, but in general, rising inflation can help deflate debt burdens. Since lower-rated bonds tend to have little or no interest rate sensitivity, they may fare better in a rising rate environment spurred by rising inflation.

It is too early to determine whether the Fed is behind the curve on inflation, and data released over coming weeks and months should shed further light. Should the Fed be slow to adjust policy in response to a gradual rise in inflation, bond yields (longer-term yields in particular) may move higher as investors price in a greater buffer again inflation risks. Lower-rated bond sectors, such as bank loans and high-yield bonds, tend to fare better against inflation risks. As the low inflation pillar of year-to-date bond strength fades, it may be one more reason to be cautious in the bond market.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Stock and mutual fund investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Barclays US Aggregate Bond Index is a broad-based index that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Tracking #1-284682 (Exp. 06/15)