With geopolitical risks abound, financial markets were resilient yet again last week, thanks to the mostly dovish tone struck by the Open Market Committee of the Federal Reserve and its Chair, Janet Yellen. Despite recent economic indicators registering a pickup in growth and inflation, namely CPI, the FOMC reiterated its “lower for longer” theme in managing interest rate policy. With upside surprises in both the headline number and core component, May consumer prices rose to an annual rate of 2.1%, the third straight month of solid gains. Not surprisingly, Treasury Inflation Protected Securities (TIPS) responded favorably to the data, widening their break-even yields relative to nominal US Treasuries. Rising inflation and a sit-tight Fed is unequivocally good for TIPS. In her post meeting press conference, Chair Yellen glossed over the recent uptick in inflation readings, referring to the data as “noisy.”

“So I think recent readings on, for example, the CPI index, have been on the high side, but I think it’s the data we are seeing is noisy. I think it’s important to remember that, broadly speaking, inflation is evolving in line with the Committee’s expectations.” - Janet Yellen, June 18, 2014

With interest rates solidly entrenched in a well-defined range of late, we ponder where future domestic market strength may develop—especially if the economic data continues to surprise to the upside, as the data alone does not warrant a revisit to yearly lows in interest rates. Over the near term, there is a dearth of economic releases as we approach the mid-point of 2014.

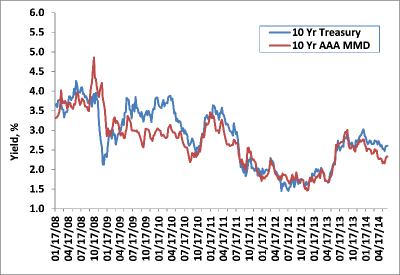

Weekly Change: 10Y Treasury Yields vs. 10Y AAA MMD

Source: Bloomberg, Thomson Reuters and Castleton Partners

Ratio of 10Y Muni Yield to 10Y Treasury Yield

Source: Bloomberg, Thomson Reuters and Castleton Partners

Tax-Exempt

Municipal yields were relatively stable last week and performed in line with their taxable counterparts amongst heavy supply. Tax exempt activity has been primarily one-dimensional of late, as participants reinvest a sizable month of coupon and maturity payments within a new issue calendar that has been dominated by large, liquid credits—and with taxable equivalent yields superior to taxable alternatives.

In a continuing sign that the credit landscape in tax exempts is improving, both Moody’s and Fitch raised their ratings and outlook on the State of New York last week. Now rated Aa1/AA/AA+, New York State has attained its highest credit rating since 1975 on the heels of “sustained improvements in fiscal governance, the strength of the recent economic recovery, and reduced spending growth” according to Moody’s. The improved economic environment in New York is not limited to just general obligation debt, however, as Standard and Poor’s raised its rating on the Metropolitan Transportation Agency (MTA) to AA- from A+. The MTA is the largest transit system in the U.S., employing 66,000 workers and carrying an average of 8.5 million people daily. Castleton continues to view each credit favorably, and we view current levels as attractive sources of tax exempt income—especially for New York State and New York City residents.

The last full week of June brings another large primary calendar, with over $9 billion expected to price. The State of Washington ($1.2b), New York State Dorm Authority ($1.2b), Massachusetts G.O. ($500mm), and Sacramento County Sanitation District ($350mm) are the largest scheduled issuers. On the “yielder” side of new debt this week, a new $185mm loan from Detroit Public Lighting Authority (PLA) will be pricing, as well. Rated A-/ BBB+, this will be the first public borrowing of this recently created entity charged with repairing and replacing the estimated 88,000 street lights in Detroit. Security for Detroit PLA is a perfected first lien on revenue from a 5% tax assessed on electric, gas, and local telephone utilities (electric & gas account for 90% of revenue). Bondholders are protected by the legal filing and approval with the current bankruptcy court overseeing the City of Detroit’s plan of reorganization, such that the 5% utility tax is not revenue of the City. All revenue from the tax is sent directly from the utilities to the trustee, who sets aside the revenue for the benefit of bondholders. As long as PLA has debt outstanding, state statue prohibits the City from ever lowering the 5% tax. Conversely, the rate may not be increased without state legislative authority. Total revenue for the Detroit PLA in 2013 was nearly $40 million, representing nearly three times coverage on their expected bonded debt. Initial price talk is a tax exempt yield of around 3.5% in ten years.

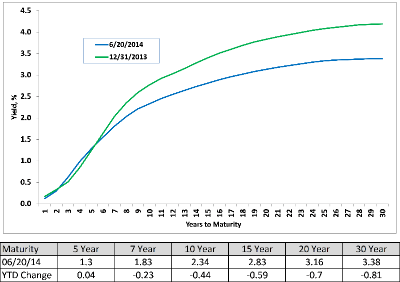

AAA Municipal Market Data (MMD) Yield Curve

Source: Thomson Reuters

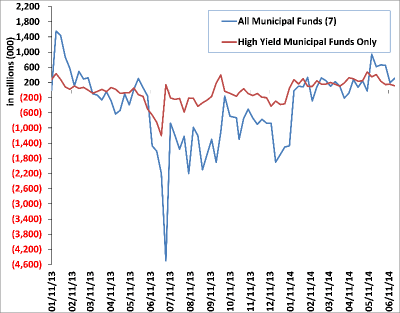

Weekly Municipal Mutual Fund Flow Data

Source: Lipper AMG Data

Taxable

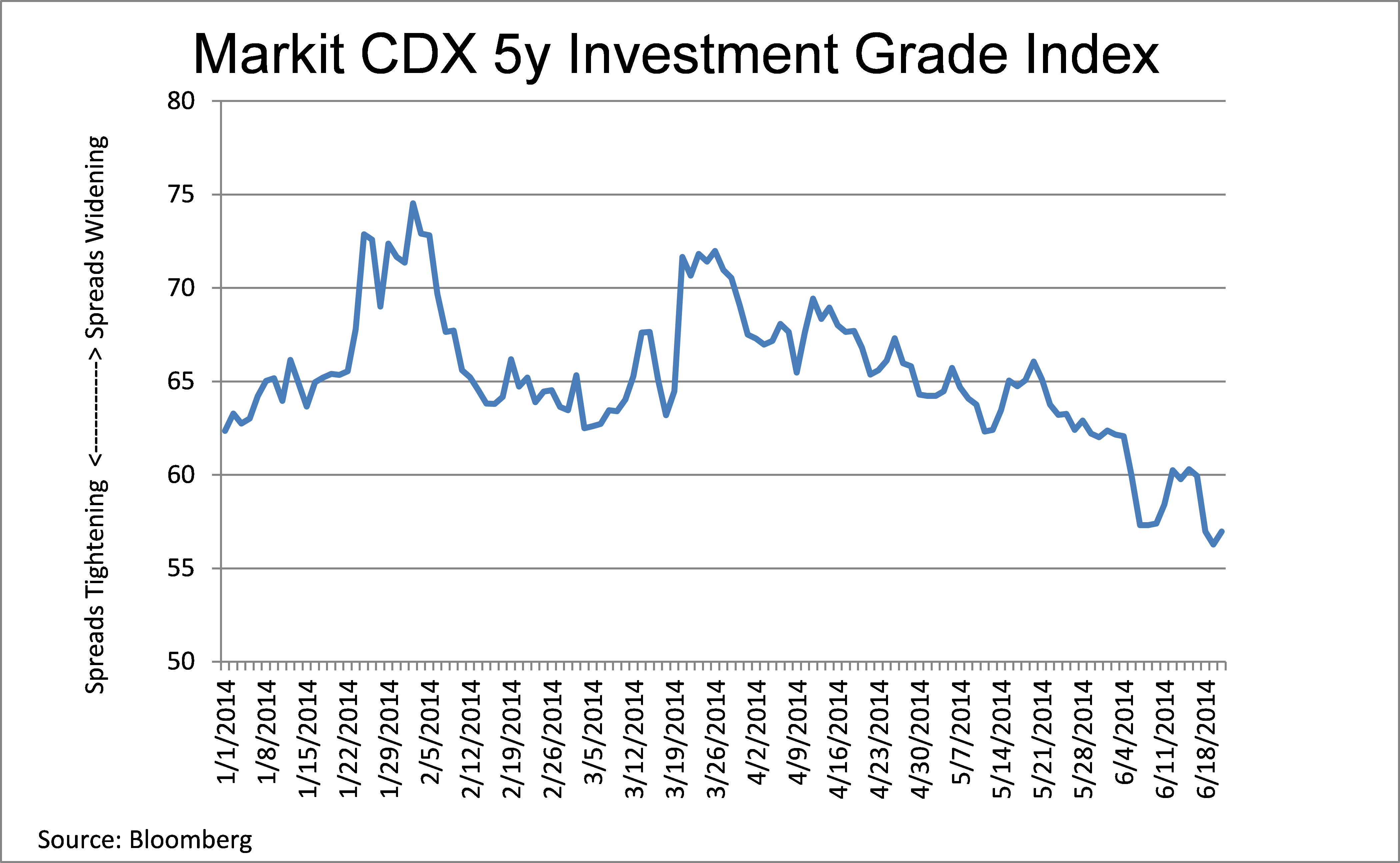

Continuing to benefit from historically low levels of volatility, investment grade spreads ground tighter yet again and ended the week at post financial crisis tights relative to US Treasuries. Taking its cue from an FOMC that offered no surprises, all sectors were able to improve (on average 3-4 basis points each), with financials registering the best performance. Despite rates creeping higher during the month of June, total returns in high grade credit has returned close to +5% so far in 2014 (as measured by Barclays)—besting the +2.16% return in Treasuries (Barclays). With credit spreads near historically tight levels, we reiterate our caution on the sector, as there is little widening required to offset the carry of the excess credit spread.

With the FOMC meeting front and center on investors’ minds, “only” $25 billion of new issue supply was priced last week, versus the prior week’s calendar of $44 billion. Financials, once again, dominated issuance, with the 10 year sector the most active tenor. High-grade mutual funds received an additional $2 billion in demand last week, as well.

© 2014 Castleton Partners, LLC. All rights reserved.

THE FOLLOWING NOTES AND DISCLOSURES ARE AN INTEGRAL PART OF THIS REPORT: Past performance is not a guarantee of future results. Different investments involve varying degrees of risk, including the risk of illiquidity and the risk that you could lose part or all of your investment. There can be no assurance that the future performance of any specific investment, investment strategy, or product (including those discussed herein or recommended or undertaken by Castleton Partners, LLC) will be profitable, equal any corresponding indicated historical performance, be suitable for your portfolio or individual situation, or prove successful. Charts, graphs and indices are included herein only for reference and do not constitute forecasts of the past or predicted future performance of any investment. Indices are not investments. Due to changing market conditions and other factors the content herein may no longer reflect Castleton Partners, LLC’s current opinions or positions. Nothing discussed herein is or is intended as tax, legal, accounting or personalized investment advice from Castleton Partners, LLC. Should you have any questions regarding the applicability of any specific issue discussed herein we encourage you to consult competent advisers of your choosing. Nothing herein is or is intended as an offer to sell or a solicitation of offers to buy any security. Castleton Partners, LLC’s current written disclosure statement including discussion of our advisory services and fees is available upon request.