The claim of provenance in the invention of football always puts great pressure on teams from the United Kingdom when they compete in international play. Unfortunately for the English, the results from Brazil to date make some in Britain wish they had never heard of the game.

In the present day, the British may be on the verge of trend-setting in the central banking arena. During the past week, the Bank of England (BoE) has sent out strong hints that it will be the first major world central bank to begin removing the accommodation it provided in the wake of the 2008 financial crisis. In blazing this trail, the BoE will be closely watched by others who hope to follow the same path before long.

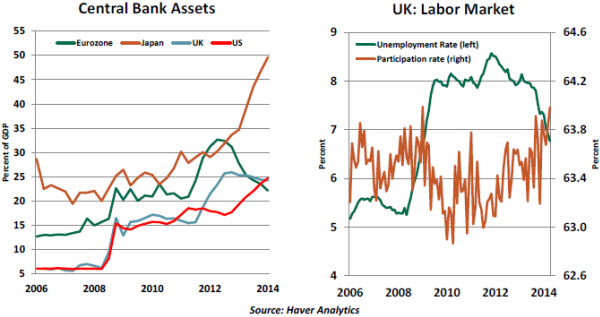

The United Kingdom suffered badly during the 2008 financial crisis. Real gross domestic product (GDP) fell by 7% from peak to trough, considerably more than the decline seen in the United States. Unemployment rose by more than 3%, and two of the country’s biggest banks needed substantial help from the government to avoid failure.

In response, the BoE used the same mix of conventional and unconventional policies employed by the Federal Reserve. The short-term interest rate was cut from 5% to 50 basis points in a matter of months, and forward guidance was given that it would remain there for some time. A program of quantitative easing (QE) was initiated.

Initially, the BoE’s quantitative easing program was more aggressive than the Fed’s, but it was ended in 2012 based on the assessment that it was no longer effective. Today, the two central bank balance sheets are at about the same level of GDP.

But the results gained from these actions have not been the same. American unemployment has fallen by more than Britain’s since 2010, but the U.S. labor force participation rate has dropped by 2.5% during that interval. In the United Kingdom, the labor force participation rate has increased by a full percentage point in the last three years and now stands higher than the U.S. level for the first time since the 1970s. Both countries have sizeable postwar generations moving into retirement, so this divergence has piqued a good deal of curiosity.

Less than a year ago, the BoE set a 7% unemployment threshold for considering changes to policy. The bank’s forecasts suggested that goal would not be reached until 2016, but that proved two years too long. The bank’s Monetary Policy Committee (MPC) replaced that target earlier this year with an extensive labor market dashboard, which continues to show strong job market performance.

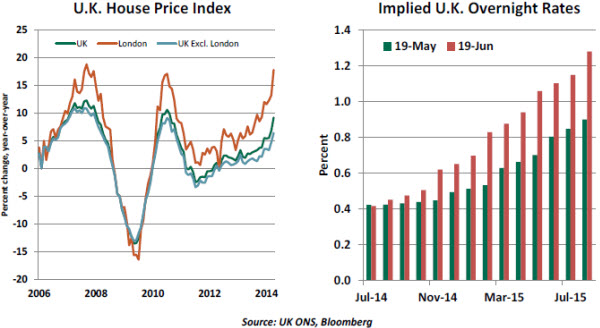

The MPC has also focused on the renewed heat under the U.K. housing market. Nationwide, house prices have risen by nearly 10%. And while much of the impetus for the increase came from London, values in other parts of Britain have also moved ahead more rapidly. BoE officials have engaged in the debate over how best to address the situation.

Persistent warnings about the rise in home prices have been the MPC’s first line of defense. (It almost seems required for MPC members to make mention of the situation in their public remarks.) The second might be a set of restrictions on mortgage lending. But in some markets (London in particular), foreign buyers paying cash are setting the pace, limiting the potential effectiveness of lending curbs.

New rules would also hinder first-time homebuyers, a market segment that many would prefer to promote. This is a conundrum seen in many world property markets, raising questions over the use of “macroprudential” policies.

Perhaps recognizing this, BoE Governor Mark Carney warned last week that interest rates could rise “sooner than markets currently expect.” This observation came as a surprise, given that Carney had cautioned just last month that Britain’s economic recovery was still not firmly entrenched and that rates would be held down until it was.

Markets moved quickly to adjust their expectations; the first movement in the benchmark bank rate is now anticipated before the end of this year. This, in itself, represents a tightening of monetary policy. Having used forward guidance to put a cap on long-term interest rates, Carney has now abruptly removed it. Central bank observers will be watching to see how, and if, the BoE can keep a lid on expectations about future increases.

The timing of tighter credit will be difficult. The BoE has the sole mandate of controlling inflation, which has been halved during the past 12 months and now stands at just 1.5% year-over-year. This would normally call for accommodation, and not restraint. How will Carney balance these readings with the desire to preserve financial stability?

All of this is tricky business, but the BoE should feel fortunate about the opportunity to switch from defense to offense. The Three Lions may not be advancing any further at the World Cup, but at least they’ll come home to a strong economy. And Wimbledon starts next week, to divert the attention of sports fans.

Prices and Patience

The Fed’s latest policy statement retained the language on inflation from the previous meeting. The inflation forecast for 2014 was nudged up only one tick, while inflation predictions for the rest of the forecast period were left mostly unchanged. Yet these elements may be at odds with recent inflation numbers that are firmer than a few months ago.

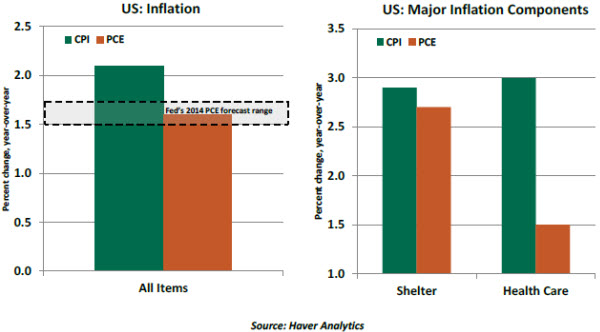

The Fed prefers inflation readings obtained from the personal consumption expenditure price index (PCE); April PCE overall inflation and core PCE inflation stand at 1.6% and 1.4%, respectively. Neither looks that threatening.

But the Consumer Price Index (CPI) of May, published earlier this week, shows an unmistakable and widespread pickup in inflation. The May CPI and core CPI, which excludes food and energy, rose 2.1% and 2.0%, respectively, from a year ago.

Some of the differences between the CPI and the PCE are due to their composition. Shelter is a bigger contributor to the former, and medical care expenses are a larger share of the latter. Shelter costs are expected to maintain the advancing trend, reflecting the pressure from rising rents.

Medical care costs are better reflected in the PCE inflation measures, as they cover more than simply the out-of-pocket expenses captured in the CPI. But both indices are being challenged by transitory factors related to federal budget cuts to the sector and the impact of the Affordable Care Act. This makes projecting inflation, especially as represented by the PCE, a bit more difficult.

It is entirely possible that the May PCE inflation reading due next week will breach the Fed’s current 2014 inflation forecast of 1.5% – 1.7%. When the likelihood of this was brought to Fed Chair Janet Yellen’s attention during the press conference earlier this week, she firmly stated that recent CPI readings were on the high side but “noisy,“ and that the Fed sees inflation moving gradually toward its 2% target.

The Fed’s dual mandate of price stability and full employment is generally complementary. But in situations where the two send conflicting signals, the Fed might set policy based on just how far it is from achieving each of them. If the distance from achieving one objective is particularly large, it could be desirable to “tolerate some movement in the opposite direction on the other objective.” This is a broad hint that the Fed may allow inflation slightly higher than the target of 2% for a limited time if progress on the employment front is unsatisfactory.

Two factors support Yellen’s optimistic view about inflation. First, inflation expectations are contained and moving in a narrow range close to 2%. Second, Yellen pointed out that the current rate of nominal wage growth is low. Wage trends reflect spare capacity in the economy and as long as they are low, higher inflation is not as great a risk.

So there is no imminent threat of runaway inflation. However, if the Fed’s projections of economic growth are accurate, it may be under pressure to modify the current inflation forecast and its views about inflation sooner than expected.

Iraq and Oil Prices

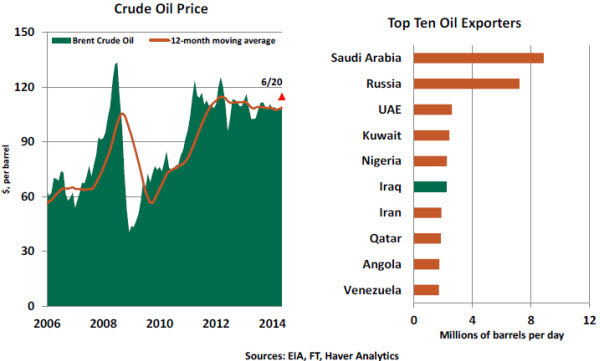

Brent crude oil for July delivery is trading around $115 a barrel as of this writing after holding around $110 for a little over three years. Internal strife in Iraq is the primary reason for the recent gain in oil prices, and the direction of the discord is highly uncertain. The key question is how to think about future oil prices in this context.

There are two main factors that influence oil prices: geopolitical conflicts and economic fundamentals. Market disruptions from geopolitical developments in Iraq will continue for a finite time period. Within this time frame, a hike in oil prices should not be surprising.

Iraq’s latest conflict has affected a part of its oil infrastructure, but the major oil fields in Southern Iraq are untouched. Although Iraq has important levels of crude reserves, it is not the largest exporter. Capacity exists elsewhere in the world and in the region to compensate for any temporary interruptions of supply.

It is also noteworthy that U.S. reliance on imported oil has dropped noticeably in the past few years.

Higher energy prices can act as a tax on consumers, but for now the impact of the Iraqi situation looks limited. Gasoline expenditures in the United States have generally held between 2.5% and 3% of total nominal consumer expenditures in the last 20 years. Gasoline prices are below the 2011 mark, but there is small risk to consumer spending if oil prices advance further.

So in the short-run, the economic impact of the hostilities in Iraq seems manageable. But longer term, the risk that other regimes might be destabilized by the push for an Islamic state that crosses current borders is one that could upset the current equilibrium. For markets where volatility is low and prices are high, this represents the kind of event risk that could create a correction.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.