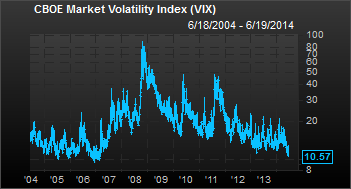

Many investors, including ourselves, look at the CBOE VIX to measure market volatility. Over the past few days the VIX has made multi-year lows and is back at levels last seen in 2006-2007.

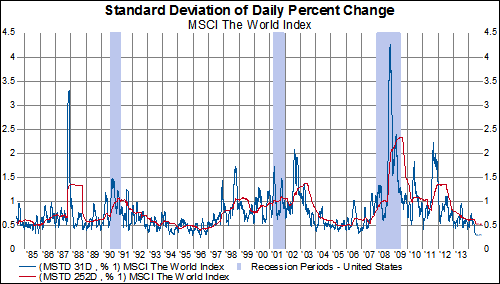

Another way that we look at volatility is by tracking the standard deviation of the daily price change in the market. What we see when we measure volatility using that metric is that volatility over the past 31-days is lower than at any point since 1996. Looking at it from a longer time-frame, over the past 252-days volatility is now at its lowest point since July 2007.

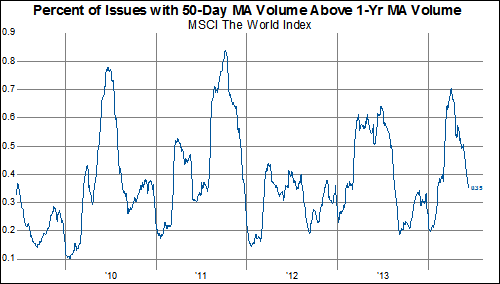

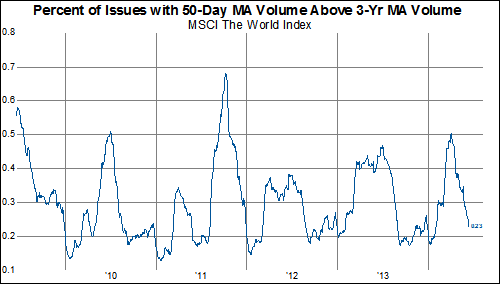

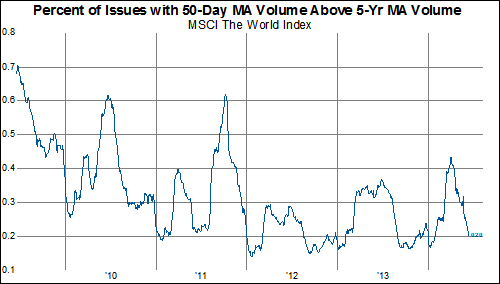

This lack of volatility seems to have made its way into volume statistics as well. As the charts below show, volume levels have fallen sharply since April as the percent of issues with their 50-day moving average of volume compared to their 1-year moving average, 3-year moving average and 5-year moving average have all steeply declined.