A Brief Review of Year-to-Date Gold/Currency Performance

Ade Odunsi is the Managing Director for Treesdale Partners and portfolio manager of the AdvisorShares Gartman Gold/Euro ETF (GEUR), AdvisorShares Gartman Gold/British Pound ETF (GGBP), AdvisorShares Gartman Gold/Yen ETF (GYEN) and AdvisorShares International Gold ETF (GLDE).

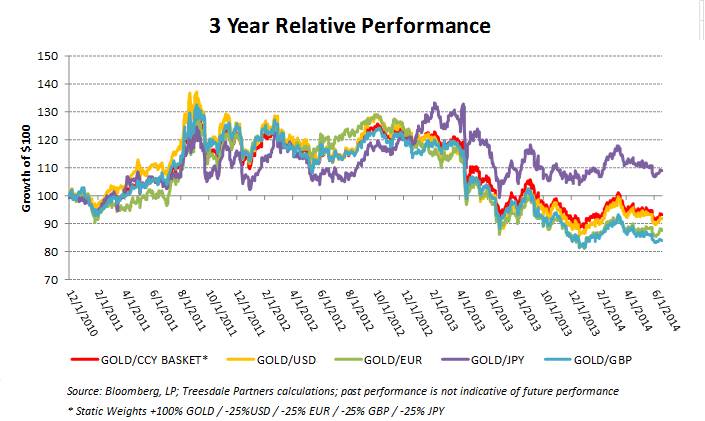

1. As a brief primer on how the performance numbers are calculated, we note firstly that all figures shown here are expressed in US dollar terms. The performance for the gold financed in non-dollar strategies is calculated by subtracting the percentage change in the ccy/USD FX rate (expressed in US dollars) from the percentage change in the gold price in US dollars [ e.g. % Gold in Yen = % Gold in USD – % Yen/USD FXRate]. The Gold/Basket strategy is simply an equally weighted average of the return of gold in dollars, euro, yen and pounds, rebalanced on a daily basis.

2. At its peak in March, gold in dollar terms was up just over 15% on the year but has since fallen back and is currently up 5.7% on the year. Its performance earlier in the year was buoyed by a resumption of inflows into gold-linked ETPs following a long period of outflows during 2013 as well as the escalation of tensions between Russian and Ukraine. These factors have since dissipated with year to date flows into ETPs now firmly in negative territory (-36 metric tonnes) and the political situation in Ukraine inexplicably fading from investors’ concerns despite a significant escalation of the conflict.

3. Year to date, gold in euro terms has been the best performer, out-performing gold in dollars by 1.5%. The outperformance has very much been driven by the weakness in the euro versus the dollar which itself has been driven by the European Central Bank cutting interest rates at its last policy meeting on June 5th and announcing a number of unconventional policy measures to combat the slowdown in credit growth and disinflation.

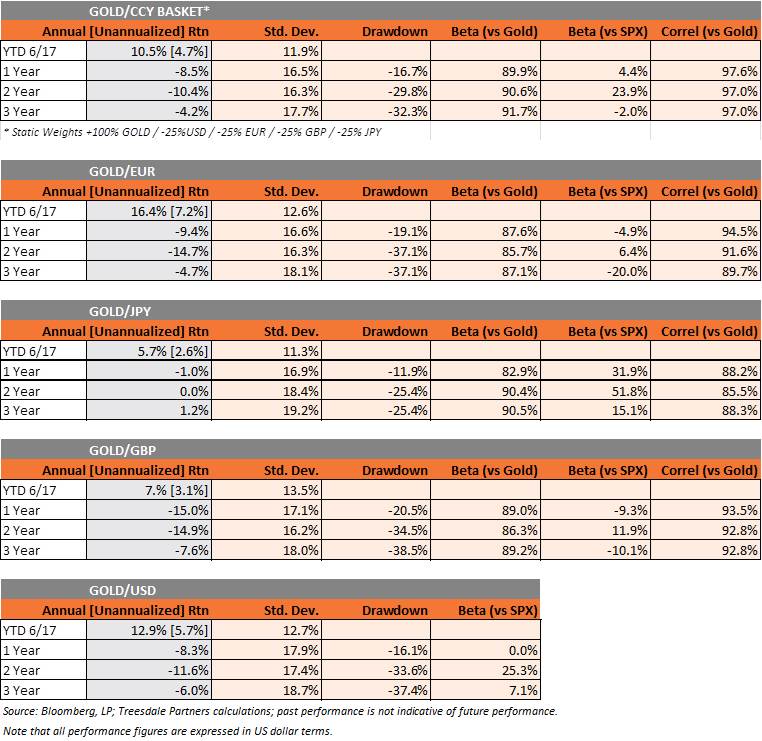

4. Performance for gold/Basket is an equally weighted average of the performance of gold in dollars, gold in euro, gold in yen and gold in pounds, with daily rebalancing. In effect the performance reflects the price of gold funded with an equally weighted basket of the four currencies. The benefits of ‘averaging’ are evident in the performance figures with the gold/Basket showing lower price volatility versus gold in dollar terms. Year to date, gold/Basket has underperformed gold in dollars by 1% but has experienced lower price volatility in every time period.

5. Gold in yen terms has shown the smallest peak-to-trough drawdown in every period going back 3 years. This is a reflection of the performance of the yen versus the dollar which has weakened by over 38% trough-to-peak since June 2011. The weakness in the yen has in turn driven the outperformance of gold in yen terms versus gold expressed in the other currencies. Over the last 3 years gold in yen terms returned +1.2% versus gold in dollars which has returned -6%. Also of note the peak-to-trough drawdown for gold/Basket over the same period was 5% lower than gold in dollars, a reflection of the positive contribution to performance from the allocation away from the dollar into the yen.

6. We note however that gold in yen terms has been the worst performer of the gold strategies a reflection of the 3% strengthening in the yen versus the dollar, experienced since the start of the year.

7. All the gold strategies exhibit very low betas versus the S&P 500 index showing the potential benefits of holding gold as part of a diversified portfolio. Interestingly, gold in yen terms has shown the highest beta versus the S&P 500 (although the beta is still well below 1) most likely reflecting the strongly correlated positive performance of the dollar/yen FX rate (+38%) and the S&P 500 (75%) over the same period – however we should stress that we do not infer any causal relationship between the two markets.

8. Unsurprisingly, all four gold strategies (gold in eur, yen, pounds and the basket) exhibit very strong correlation to gold in dollar terms.