“I’m turning Japanese, I think I’m turning Japanese, I really think so.”

The English band, the Vapors, was an 80s one hit wonder with the song “Turning Japanese.” I was never a fan but the tune seems to be getting renewed airplay with a very narrow audience these days: central bankers and economic policy makers. The song has little to do with Japan, or Asia for that matter, aside from a clever oriental riff (it’s actually about love). That hasn’t stopped policy makers from taking the chorus line at face value: namely the risk of their economy “turning Japanese”.

Turning Japanese in today’s macroeconomic environment means that your country (or block of countries) is at risk of deflation and if action is not taken quickly and decisively, that risk can turn into a 20 year battle, just like in Japan.

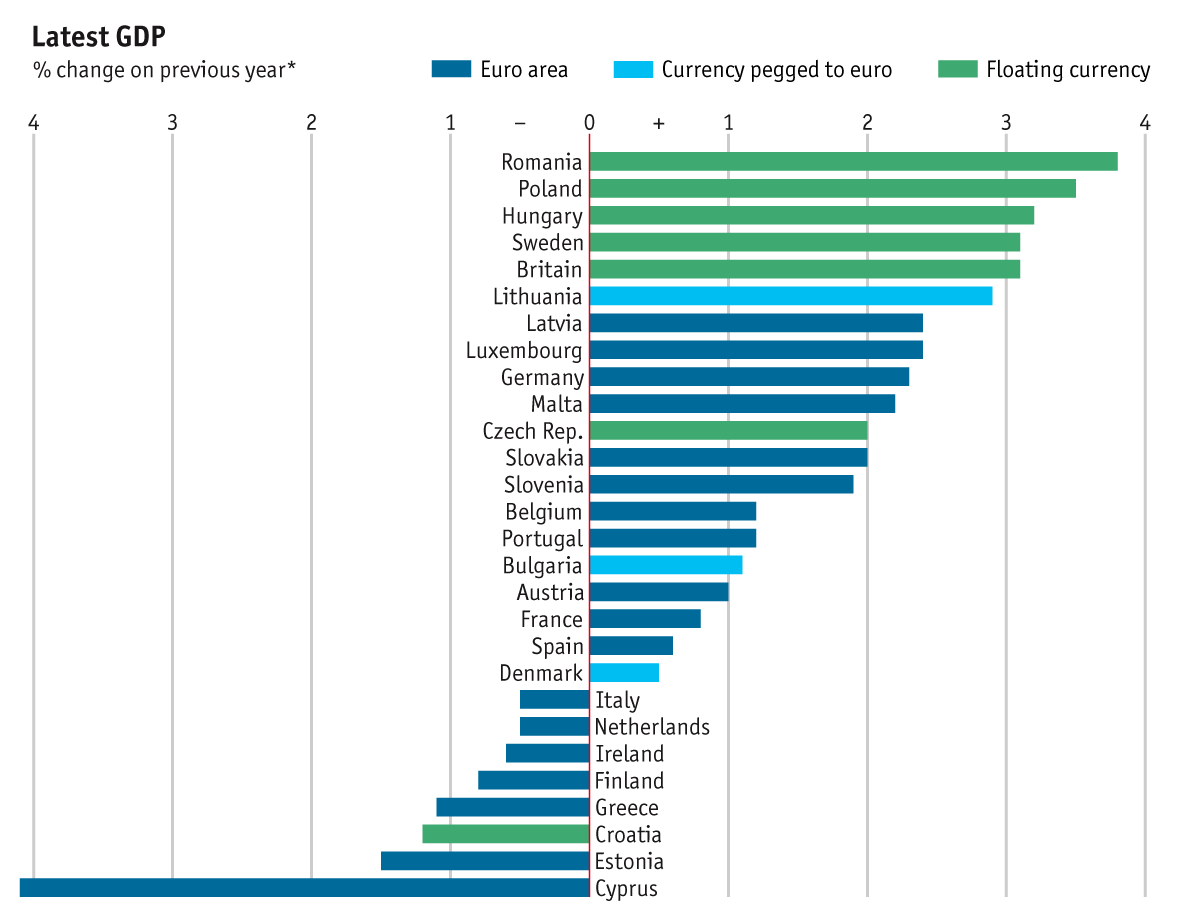

Last week, Mario Draghi, the European Central Bank president, fearing the deflationary trend in Europe is getting worse, took decisive action by cutting the benchmark interest rate to 0.15% (a record low) as well as the unprecedented action (for a central bank) of lowering the deposit rate to a -0.10%. First quarter GDP growth in the EU (28 countries) was just 0.30% and an even poorer 0.20% across the Euro block (18 member states). Additionally, consumer prices across the EU have plummeted over the past two years and while this trajectory was to be expected in countries like Spain, Portugal and Greece, where the bite of austerity was the fiercest, the trend in consumer prices in Northern Europe has sharpened minds to act, or at least give Mr. Draghi the leeway to act.

Source: Economist

Source: Economist

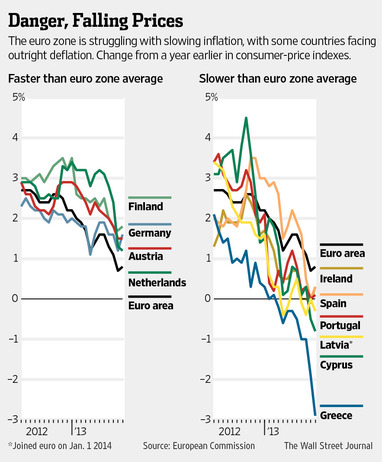

Germany’s inflation rate fell to 0.60% in May (see “Falling Prices” image below), the lowest since the financial crisis. In the Netherlands, property prices have fallen by over 20% and a quarter of houses are in negative equity. France, where Monsieur Hollande has been able to alienate the political left (by implementing austerity measures worth 5% of GDP) and the political right (increasing / not cutting taxes, failing to promote pro-business policies) with his policies, remains stuck at zero growth. It’s no wonder that Francois Hollande may be the most unpopular president in French history.

There is clearly a risk of EU-wide deflation and if there is one thing policy makers can agree on, its that it needs to be stopped before it starts. Once deflation sets in (like Japan), it’s a lot harder to get inflation than one may think. The markets anticipated something big and they got it, namely negative interest rates. While the efficacy of the policy may turn out to be underwhelming, the unconventional nature of negative interest rates has rightfully drawn a lot of attention. Negative interest rates are effectively a fee (or a tax) on reserves a bank would hold at a central bank, in this case, the ECB. Rather than a bank paying a depositor interest (a novel and long forgotten concept), the depositor bank is charged a fee to keep their money in a central bank deposit or reserve account.

For the ECB, the immediate goal is two-fold: force banks to lend more, especially in the South, and weaken the Euro. Whether banks actually lend that money into the economy is another story – they could just as easily invest those funds in interest paying sovereign bonds at particularly unattractive rates (Spain now borrows at a cheaper 10 year rate than the U.S.)

Source: WSJ

Negative interest rates have only been tried a handful of times in the past (Sweden in 2009-2010, Denmark in 2012 and Switzerland in the 1970s), typically to dissuade foreign capital from pushing up a currency. There is no robust historical sample to guide Mr. Draghi – he is in uncharted waters.

The risk of deflation is not to be underestimated and the havoc it can wreak in Europe makes it potentially more crippling than in Japan. Specifically, the impact deflation has on debt dynamics is significant for Europe. For the southern countries like Spain and Portugal, which are trying to implement austerity measures to drive down debt to GDP ratios, deflation is more than a couple steps backwards – while the economy contracts the nominal value of those countries debt does not, thereby making it more difficult to service the debt and bring aggregate debt levels down.

While there is no doubt the recent economic reports have prompted Mr. Draghi to act, it may be the recent results of European elections that really got Mr. Draghi moving. Eurosceptic parties have won increasing seats in government across much of Europe, including Britain (UKIP) and France (Front National). The political tides are moving against Mr. Draghi and it is unlikely that European leaders will be as willing to promote EU convergence or Eurobonds as they have in the past.

It is telling that when asked what she would do on her first day as President (if she were to be elected), Marine La Pen, leader of the Front National (and significantly more rational and mainstream than her father Jean-Marie, the founder of the Front National), said she would instruct the French Treasury to draft a plan to restore the Franc. In the short-term, a lack of growth and deflation may have Europe “turning Japanese” but it may be Europe’s politicians “turning Japanese” that ultimately leads to the Euro’s undoing.

© CMG Capital Management Group