Lately, concerns have been on the rise regarding technology stocks and their growth outlook. We’d like to provide our thoughts on the current market environment, our outlook, and as a result, how the Fund is positioned.

Short-term turmoil

One of the questions we have received in recent months is, “Do you feel like we’re in the midst of a tech bubble?” For many, the answer is yes, but we think that’s wrong. We believe volatility has been driven by some macroeconomic concerns, but more specifically, it’s been driven by a very small handful of names – many of them in science and technology sectors and industries – that have been “bubble-like” in terms of valuation. But, unlike what we saw as the market peaked going into March of 2000, and unlike what we saw as we entered the second quarter and beyond of 2008, we think, by and large, the market is reasonably priced. Not only do we see continued valuation support and steady earnings growth, but we are encouraged by a number of compelling investment opportunities throughout the global marketplace. As such, we haven’t implemented significant hedges to combat a declining market nor defensively raised the Fund’s cash position. Our view over the short to intermediate term does not warrant those actions.

Staying the course

Unfortunately, with the U.S. Federal Reserve tapering its bond-buying program, accompanied by the disappointing recent performance of many biotech and tech company IPOs, the speculative risk and cautious growth outlook associated with owning these companies has increased. As a result, we have seen a general market shift to value-oriented securities and a lack of discretion by investors when reducing exposure to perceived higher-beta stocks.

Consequently, we’ve seen positions in the Fund underperform through the first part of 2014 despite, in our view, them being fundamentally sound, well-positioned companies. When we think about the Fund’s investment strategy and the approach we take, we think quite seriously about stocks that have the durability and the potential to be in the portfolio over the course of several years. The Fund seeks companies that are able to achieve both top- and bottom-line growth of at least 20% over the course of a minimum three to five years. That means, not only can a company grow, but it can grow in a profitable manner over time.

We think Isis Pharmaceuticals1 is a very good example of this investment approach. The stock has been in the portfolio since 2008 and was up more than 150% for the one-year period ending first quarter 2014. Lately, however, it has pulled back quite substantially. Despite the general market sell-off, we think the prospects for Isis Pharmaceuticals continue to be bright. The company maintains a broad pipeline of 32 drugs to treat a wide variety of diseases, and in our view, the company’s patents provide strong and extensive protection for its innovative drugs and technology. Recently it announced positive clinical data relating to its collaboration with Biogen Idec for a drug that treats spinal muscular atrophy. Bottom line – when a company is able to create novel, new therapies with significant positive outcomes, we believe people will pay for them. As such, we’re staying the course.

Opportunities on the horizon

We continue to see a number of compelling investment opportunities. One surrounds innovative water technology. We believe there are going to be a significant number of opportunities around the globe where people are going to be forced to engage in water transportation, desalinization and other efforts to treat less-than-potable water. Not convinced? A recent report2 released by the White House expresses concern regarding water demand and usage right here in the U.S. “The Southwest, Great Plains, and Southeast are particularly vulnerable to changes in water supply and demand. Changes in precipitation and runoff, combined with changes in consumption and withdrawal, have reduced surface and groundwater supplies in many areas. These trends are expected to continue, increasing the likelihood of water shortages for many uses.”

Based on these trends, we are attempting to increase our exposure to this theme in the portfolio. Currently, approximately 5% of the portfolio is directly related to water technology, such as holdings in Pentair, Inc.3 and Abengoa S.A4. On a global scale, Pentair, Inc. creates solutions engineered for the transmission of potable and recycled water supply, as well as water within desalinization plants, to produce clean drinking water and water for efficient use in irrigation and agriculture. Additionally, the company is a leading provider of energy-efficient pool and spa pumps, flow management solutions and water filtrations systems. Meanwhile, Abengoa S.A. offers desalination technologies that transform sea and salt water into drinkable water and develops waste-water treatment technologies for water regeneration to address scarcity. We think Pentair, Inc. and Abengoa S.A. are competitively positioned to capture the increase in demand for innovative water solutions. By offering products and services that meet these demands, we think these perceived competitive advantages will serve as catalysts for growth.

An additional theme that we expect to materialize in the portfolio is additive manufacturing and 3D printing. These are innovative technologies that we have been studying for several years but have been hesitant to include in the portfolio due to valuation concerns. In our view, developers of the technology have been overpriced, but lately we have seen a market correction. With prices that seem in-line with current market expectations, we are excited about the growth potential these companies offer. We are starting to see in a variety of end markets, particularly in aerospace and automotive, where additive manufacturing and 3D printing costs are coming down, providing the potential to realize significant value.

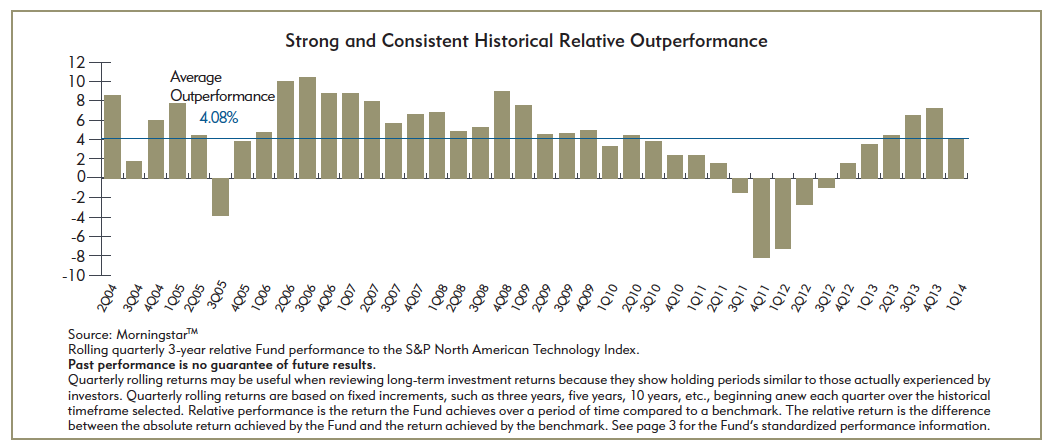

The identification of investment themes is a cornerstone of the Ivy Science and Technology Fund’s investment mandate – serving as a guide to help us resist overreaction to short-term market gyrations. And, we believe the identification of such themes serves as an investment map for the long term. This methodology has served us well. Over the past 10 years, the Fund has outperformed the benchmark on a rolling three-year basis 85% of the time. Using the same methodology, the Fund has achieved relative average outperformance of 4.08%.

Optimistic outlook

While we recognize the challenges of the world economic backdrop, we are excited about the innovation and growth that is taking place within certain companies. We believe many of the stocks in the information technology space remain relatively inexpensive and are well positioned going forward. As confidence is restored, we believe there should be an increase in capital expenditure in various markets around the world as companies become more comfortable with the high cost transitions related to changes in internal infrastructure.

On the health care front, we believe managed care companies will benefit from the implementation of government initiatives. Also, in developing markets, as the standard of living increases, we believe the demand for quality health care increases as well. In our view, medical technology, biotechnology, medical records and pharmaceuticals are among the greatest innovators and early adopters of new science and technology, so we are paying particularly close attention to companies in those areas. We also are looking more closely at names that may benefit from a low-interest-rate environment.

To summarize, we are generally positive about the path of economic growth. In mixed economic environments, we believe there are many potential investment opportunities – especially in scarce resources, data, mobility and health care – around the world. As we look at the securities of such companies, we are attracted by what we believe are good growth prospects and sound capital structures. We believe there will be a modest improvement in capital spending trends, and we are looking for some restoration of merger-and-acquisition activity as well. As always, we will carefully monitor the macroeconomic environment, but our focus remains primarily on security-specific fundamental research. We believe this attention to bottom-up research, coupled with the innovation and transformation under way across the globe, will continue to uncover investment opportunities.

1 1.6% of Fund net assets as of May 31, 2014

2 2014 National Climate Assessment

3 2.9% of Fund net assets as of May 31, 2014.

4 1.9% of Fund net assets as of May 31, 2014.

Data quoted is past performance and current performance may be lower or higher. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. Please visitwww.ivyfunds.com for the Fund’s most recent month-end performance. Class A share performance, including sales charges, reflects the maximum applicable front-end sales load of 5.75%. Performance at net asset value (NAV) does not include the effect of sales charges. High recent returns are attributable, in part, to unusually favorable market conditions and may not be repeated or consistently achieved in the future.

The opinions expressed are those of the Fund’s manager and are not meant as investment advice or to predict or project the future performance of any investment product. The opinions are current through May 31, 2014, and are subject to change due to market conditions or other factors.

Risk factors. As with any mutual fund, investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. Investing in companies involved in a specified sector may be more risky and volatile than an investment with greater diversification. Not all funds or fund classes may be offered at all broker/dealers. Holdings information is not intended to represent any past or future investment recommendations. Holdings and allocations can and do change frequently.

Investors should consider the investment objectives, risks, charges and expenses of a fund carefully before investing. For a prospectus, or if available, a summary prospectus, containing this and other information for the Ivy Funds, call your financial advisor or visit www.ivyfunds.com. Please read the prospectus or summary prospectus carefully before investing.

S&P North American Technology is an unmanaged index comprised of securities that represent the technology sector of the stock market. The S&P North American Technology Sector Index is a product of S&P Dow Jones Indices LLC (“SPDJI”), and has been licensed for use by Ivy Investment Management Company (IICO). Standard & Poor’s®, S&P® and S&P North American Technology Sector Index are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by IICO. IICO’s Ivy Funds are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the S&P North American Technology Sector Index.

© Ivy Funds Investment Management