The latest jobs report may look pretty bland on the surface, but I can assure you that it will generate plenty of intrigue among close observers of the Fed. After falling sharply in April, the unemployment rate held at 6.3%, in contrast to expectations that it would partially reverse course. At this point unemployment forecasts from the Fed and many economists will need to come down. At the March FOMC meeting the central tendency unemployment forecast in the Summary of Economic Projections (SEP) was 6.1-6.3% for Q4 2014. This now looks too high. Similarly, the consensus of economists surveyed by Bloomberg is that the unemployment rate will end Q3 at 6.3%—unchanged from the May level despite expectations for solid GDP growth. In a forecast update after the April employment report New York Fed staffers lowered their Q4 2014 unemployment rate projection by two tenths. Look for a revision of about this size (one or two tenths) in the SEP at the June 17-18 FOMC meeting and in upcoming surveys of economic forecasters.

The intrigue arises because it is not entirely obvious what lower unemployment rate forecasts would imply for monetary policy. After all, the unemployment rate already declined to 6.3% in April, and yet we could detect no meaningful change in communication from the Fed afterward. So do unemployment surprises matter for policy or not? Naturally there are competing opinions on this point.

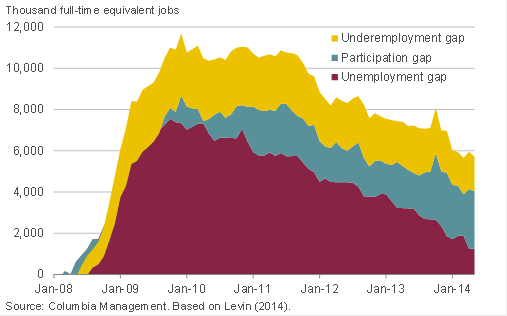

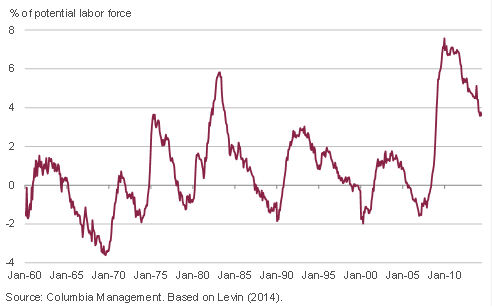

One view holds that while the unemployment rate matters at some level, Fed officials are focused on much broader measures of slack, and have perhaps put renewed emphasis on wages as well. For instance, a recent paper by economist Andrew Levin (previously Janet Yellen’s chief of staff) puts the degree of broad labor market slack at around 5.5 million full-time equivalent workers (see figures 1 and 2; these are our estimates using Levin’s methodology). Although FOMC members frequently talk about cyclical weakness in labor force participation and slack in hours worked, they rarely provide quantitative estimates like this. The Levin slack estimates are very large, and if these views were shared by Fed officials it would help to explain their limited response to declines in the U3 unemployment rate.

Similarly, Adam Posen and David Blanchflower—economists with similar ideological stripes as Janet Yellen—argued in a recent paper that wages should be used as a central guide to policy due to uncertainty about resource slack. With wages not yet definitively moving higher, Fed officials can afford to look past faster-than-expected declines in unemployment for now.

Exhibit 1: Labor market slack by type (Levin 2014)

Exhibit 2: Total labor market slack since 1960 (Levin 2014)

The alternative argument is that the lack of response to recent unemployment surprises reflects a kind of message discipline by the FOMC. Knowing that the data can be volatile, and also that markets hang on their every word, it’s possible that Fed officials wanted to see another payroll report before adjusting their tone about the timing or speed of rate hikes. For example, here’s what Janet Yellen said in her May 7 testimony to the Joint Economic Committee of Congress (i.e. right after the decline in the unemployment rate to 6.3% from 6.7%):

“So it's a little bit hard for me to give you an estimate of that. We had a huge move. It is very unusual to see a four-tenths percent decline in the unemployment rate in a single month with a comparable move in labor force participation. We always tell ourselves, and I'll state, I think one should not make too much of any single month's numbers.” (Our emphasis)

We think this debate—which has big implications for the level of rates and shape of the yield curve—could get resolved at the upcoming FOMC meeting. If the U3 unemployment rate still matters, there’s a good chance we will see an upward shift in the “dots” (Fed officials’ forecasts for the funds rate) and possibly a subtle change in message about the risks around the lift-off date at the press conference (e.g. an emphasis on “mid” rather than “late” 2015). On the other hand, if the dots remain unchanged and the press conference sounds much like recent public remarks, then perhaps we have misread the Fed’s worldview. Either way we should learn a lot about the Yellen Fed this month.

Disclosure

The views expressed are as of 6/9/14, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2014 Columbia Management Investment Distributors, Inc. All rights reserved.

943238