Dear Fellow Investors,

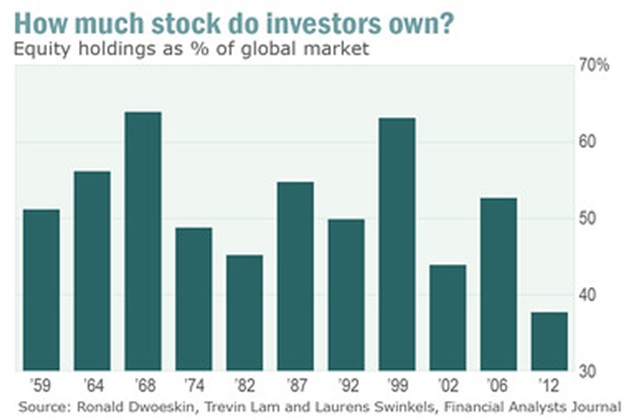

Howard Gold is an inquisitive writer for Marketwatch.com and we think has done us all a great favor in his latest column titled, “Not even a bull market can interest people in stocks.” He points out via the chart below that—despite a huge rebound the last five years in US common stocks—equity holdings as a percentage of global investable assets just climbed to levels only seen at major stock market low points. Relative to the past 50 years, this stock market has been abandoned and orphaned even as it had made participants wealthy.

Mr. Gold draws what we view as a very logical and natural conclusion from this chart and the research which came to him in the Financial Analysts Journal. He looked at the research of three Dutch researchers — Ronald Doeswijk, Trevin Lam and Laurens Swinkels, who showed that investors held only 37.7% of global investable assets in equity at the end of 2012. This led him to believe there must be some kind of a permanent change in the way money is invested. Previously strong five-year look-back returns of 18% compounded from the S&P 500 index usually elicited enormous enthusiasm like we saw in 1968 and 1999. This produced equity ownership exceeding 60% of investable assets. Here is how Gold speaks about the recent past and how it compares to history:

That and the 37.1% they invested in equities in 2011 were the lowest exposure to equities investors have had since 1959, when records were first kept. It’s considerably below what they held even in the late 1970s, before the Reagan-era bull market began, and in the early 2000s after the dot.com bubble burst.

You will probably be shocked to hear that we at Smead Capital Management draw a completely different set of conclusions from the statistics. You’ll probably be less shocked, however, to hear that we have been feeling these statistics in our gut for the last four years and are very thankful that Marketwatch.com brought them to the forefront of the conversation. We believe there are four main cyclical reasons for this shift and we are happy to share our thoughts.

First, the mass movement to bonds is a function of the 31-year bond bull market in the US which started at 15% on ten-year Treasury bonds and bottomed around 1.5% near the height of budget debate in the US in the summer of 2012. The research piece pointed out US individual and institutional investors led an increase in bond ownership to 57% of investable assets from 33.5% in 1999. This movement was also a function of the second largest population group (baby boomers) needing and seeking income and security for retirement. The final victory for the bond market was the panic and dread of the financial crisis which drove irrational behavior towards zero interest rates. As Mark Twain quipped, “There will come a day when investors will be more concerned with the return of their money than the return on their money.”

Second, US investors spent the last fifteen years attempting to organize their investments around wide-asset allocation at the expense of owning US large-cap equities. This once-in-a lifetime movement into new-found asset classes drew money away from traditional equity ownership, especially among institutions. To back up Gold’s argument, the CIO of Harvard’s endowment wasn’t embarrassed at all in a 2014 Barron’s interview, even though they entered the bull market with 12% long-only US equity ownership and proudly state that they have 11% as of the first quarter of 2014!

Third, alternative investing, as a portion of wide-asset allocation, became all the rage as interest rates declined. What could be better than to get the price of your companies out of the newspaper in down markets? Leveraged-Buy-Out (LBO) firms—it seems—were renamed private equity firms and received the endorsement of the nation’s largest endowments and institutional investors. Hedge funds appeared attractive in a world of having one foot in and one foot out the door of the US equity market. These two categories took in 9% more of global investable assets than they had as recently as in 1990.

Lastly, the largest population group in the US is echo-boomers born between 1977 and 1996. They have been much slower to get married, have kids, buy houses and merely by their age and circumstances, they are a tiny participant in equity ownership. Notice that the previous low point in the chart above was 1982, when it was baby boomers that were the large, young population group and didn’t yet own common stocks.

Here is our assessment for the future: as interest rates rise the next ten years bond returns will sour and equity dividend payout ratios will normalize. Investors will seek income from equities in a way they are not today. Bond ownership will revert to the historical mean.

We believe returns in everything from gold, commodities and other relatively esoteric asset classes will be doomed by the lack of follow up to the once-in-a lifetime move into them from 1999 to 2012 by US investors both large and small. Interest rates rising over ten years will make LBOs much less economic and private equity returns will sour if that is true. Both private equity firms and hedge funds seem to have picked over US small cap companies looking for opportunities, making it appear to us a “crowded” trade. We contend that poor performance by hedge funds will make the mystic come off, leaving good old bread-and-butter common stock ownership to regain favor based on results and transparency.

We’re confident that echo-boomers, who currently average 28-years old, will marry, have kids, purchase homes and cars. Their incomes will rise in all walks of life and they will become willing equity owners in 401k and other savings programs.

We belive the negative nabobs, who spread “black swan” fears about a massive sell-off in US equities, will be mathematically crippled by the fact that US institutional and individual investors don’t own enough in US large-cap equity to make their run for the exits meaningful. Their low historical level of participation proves it. These facts should make it impossible to have a massive sell-off, because what is not on (owned), can’t be taken off. To us it means that for an extended time period, the lack of affection for US large cap equities will mute declines and reward patient long-duration owners of quality common stocks.

Warm Regards,

William Smead

The information contained in this missive represents SCM's opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve month period is available upon request.