Treasury yields rose sharply last week, with intermediate and long date bonds registering the sharpest price declines, as US equities again reached new highs. Friday’s eagerly anticipated May employment report came in line with market expectations, continuing to signal gradual improvement in the labor market. With +217,000 jobs created last month, May marked the first 4-month string of payroll reports over +200,000 since 1999. With a yield of 2.62%, the 10 year Treasury note has now risen over twenty basis points since reaching a yearly low last month. With global growth and inflation remaining low, we are of the opinion that the recent reversal in interest rates is simply a corrective move within a well-defined yield range: 2.40%-2.80%.

Equally important last week, the European Central Bank (ECB) announced further aggressive and unprecedented steps in their multiyear campaign to promote growth and ward off potential deflation. The ECB lowered rates on three key short term rates that they control, including setting the rate for assets that banks have on deposit with the central bank to a negative number (-0.10%). Simply put, the ECB will now be pumping a large amount of liquidity into the European system. With the Federal Reserve exiting their unprecedented monetary policy, and while the ECB embarks on theirs, sovereign yields are marking recent extremes. Unthinkable just a few years ago, interest rates on Italian and Spanish five year bonds are now lower than US Treasury five year notes. Further out the curve, US 10y yields are now at their widest level to German 10y yields in 9 years.

Attention this week will be on the retail sales number on Thursday and the Producer Price Index release on Friday. Additionally, the Treasury will be auctioning off $62 billion of new supply this week (3y, 10, 30y).

|

|

|

Weekly Change: 10Y Treasury Yields vs.

10Y AAA MMD

Source: Bloomberg, Thomson Reuters and Castleton Partners |

|

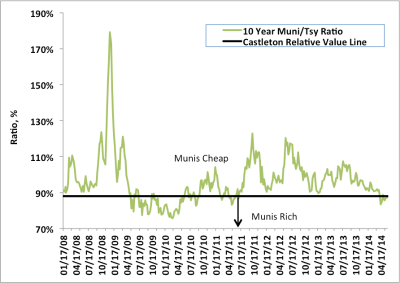

Ratio of 10Y Muni Yield to 10Y Treasury Yield

Source: Bloomberg, Thomson Reuters and Castleton Partners |

|

Tax-Exempt

Despite generally favorable technicals, tax exempt bond prices registered their first weekly drop in a month—performing in line with the rise in Treasury yields. Having risen 11 basis points last week, ten year benchmark muni yields are now at 2.27%, with the Muni/ Treasury ratio unchanged at 88%. Supply last week ($7 billion) finally saw some resistance, as tax exempt buyers were reluctant to invest at levels where yields were the lowest in nearly a year. Tax exempt credit spreads however, continued to contract, owing to the fact that high yield mutual funds continue to receive the majority of the positive cash flow recorded in mutual funds.

At nearly $9 billion, supply this week is expected to be the highest since March—well above the 2014 weekly average of $5 billion. Despite the increase, four of the largest loans this week account for over 40% of the total volume: $1.7b Los Angles School District (AA-), $850mm New York City G.O. (AA), $527mm Houston Utility (AA), and $400mm South Carolina Public Service Authority (AA-). We remain constructive on the tax exempt market, believing the sudden spike in supply and associated yield concessions should be viewed as an opportunity to invest idle cash that has been targeted for the asset class.

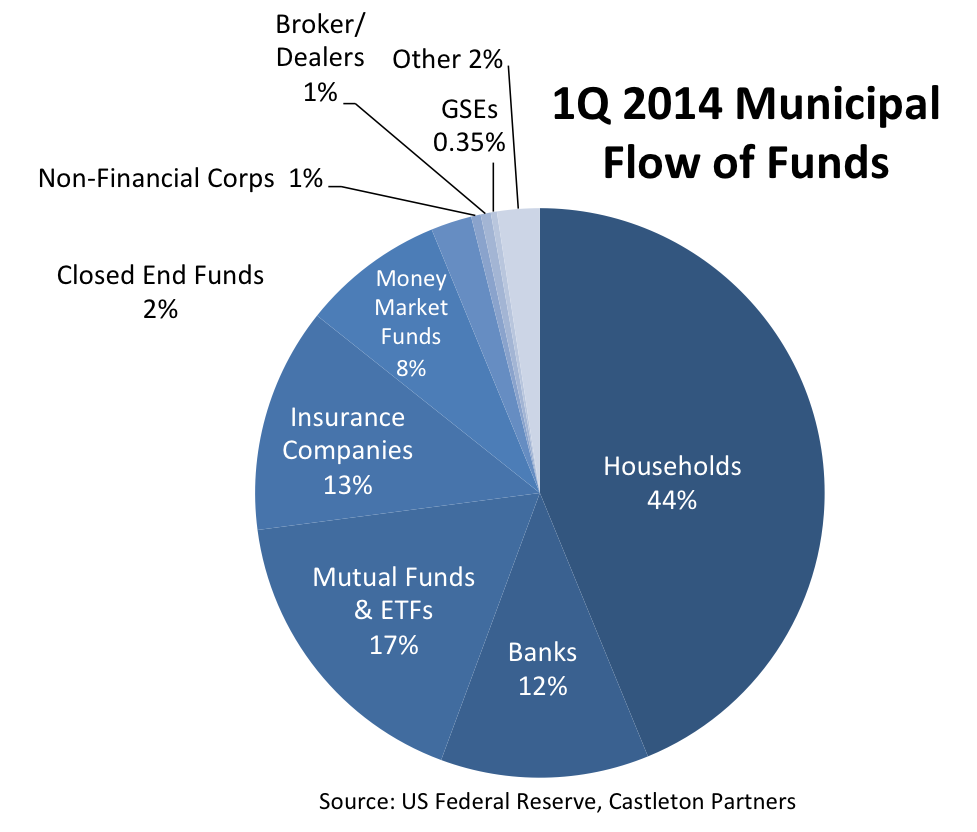

The Federal Reserve released their quarterly flow of funds data last week. Though retail investors continue to be the largest owner of tax exempt debt, with over 70% of the $3.7 trillion market, banks continue to increase their exposure. Banks now own over $433 billion (12%) of municipals as of March 31st, a near13% jump from the $384 billion they owned at the end of the first quarter of 2013. |

|

|

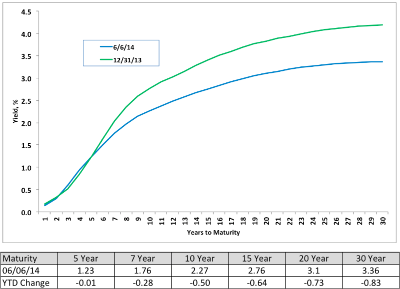

AAA Municipal Market Data (MMD) Yield Curve

Source: Thomson Reuters |

|

Weekly Municipal Mutual Fund Flow Data

Source: Lipper AMG Data |

|

Taxable

Investment grade spreads tightened modestly in the rate selloff last week, with financials registering the best performance among all sectors. With payrolls failing to trigger higher volatility in interest rates or the broader credit markets, spreads may have capacity to tighten further. However, we reiterate our neutral position on taxable spreads and duration, feeling that the increased leverage on corporate balance sheets (M&A activity)—combined with the little spread cushion available in the market today—makes taxable bond spreads vulnerable, should interest rates rise materially further. With both stock (VIX Index) and bond (MOVE Index) volatility at multi year lows, the CDX has now reached post financial crisis tights, as well ( +57). With nearly $24 billion of new debt issued, investment grade supply last week was considered heavy and varied among a diverse set of names. American Express (3y +40), AT&T (30y +140), Ford Motor (3y +90), and McDonalds (10y +67) were all well received, despite investment grade funds receiving a meager $261 million in net new cash. |

|

Read more commentaries by Castleton Partners