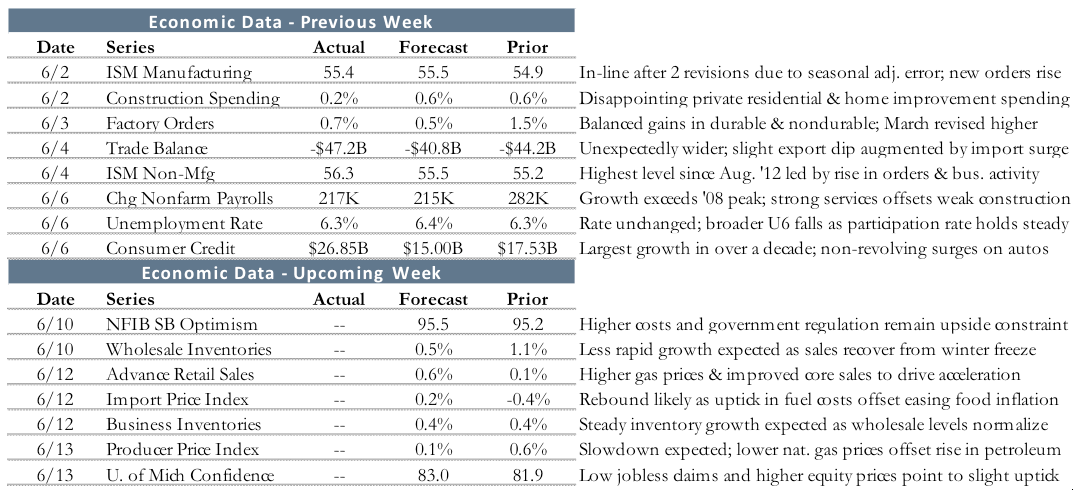

Fed’s beige book: growth rebounds from severe weather

Global equity markets cheered the European Central Bank’s (ECB) decision to lower rates and provide further monetary stimulus last week, as the DJIA and S&P 500 gained 1.2% and 1.3%, respectively. As one might imagine, notable outperformance came from Europe’s peripheral countries with Italy (MSCI Italy) and Spain (MSCI Spain) gaining 3.4% and 2.6%, respectively.

The unemployment rate for May, which came out Friday, was roughly in-line with expectations. The unemployment rate held at 6.3% while job additions totaled 217,000, results (in the eyes of investors) that were good enough to signal growth but not so good that they accelerated the Fed withdrawal of QE and ZIRP. We discuss Friday’s report further in the next section.

The Federal Reserve’s Beige Book came out last week where all 12 Federal Reserve Districts reported economic expansion during the current reporting period. Consumer spending was reported as growing at a “moderate pace” across all regions as improved weather provided a boost to business. More than half the districts experienced new vehicle sales growth. Demand was less robust for used vehicles relative to new vehicles.

Service sector activity and manufacturing activity rebounded strongly from weather-related weakness in the prior report. This was evident by the jump in both ISM Non-Manufacturing and Manufacturing indices in May.

Despite several errors in the initial report (owing to seasonal adjustment factors), the ISM indices came in positive for the month of May with the service sector jumping to 56.3 from 55.2 in April and the manufacturing sector expanding from 54.9 in April to 55.4. The ISM Non-Manufacturing index has trended in expansionary territory (i.e. above 50) for 53 straight months. The ISM Manufacturing index improved in May but fell just shy of economists’ expectations of 55.5.

The Fed reported mixed activity across residential real estate. Half the districts reported increases in residential construction activity with a few indicated weakening in activity. Non-residential construction activity and commercial real estate markets were, for the most part, steady to stronger on the period.

Overall lending activity continues to increase as roughly two-thirds of the districts reported rising loan demand. Increased loan demand occurred across both commercial and industrial businesses, as well as among consumers. Consumer credit jumped from $17.53bn in March to $26.85bn in April, substantially exceeding expectations of $15.00bn. Revolving credit – largely representing credit card use, and a better sign of consumer health and confidence than non-revolving credit – improved dramatically from $2.2bn to $8.8bn. According to Econoday, this was one of the largest gains on record. The Fed also reported encouraging news that credit quality and delinquency rates generally improved. Credit standards remained mostly unchanged.

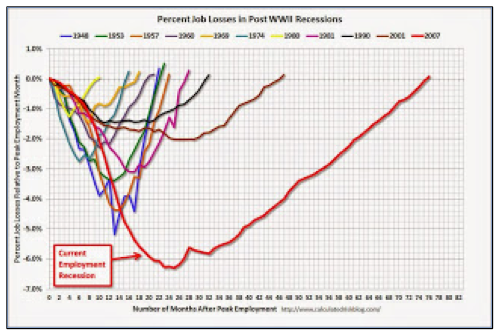

Jobs Return To Pre-Recession Peak

The US labor market continued to plod along in May, as last week’s government jobs report revealed nonfarm payrolls increased by more than 200,000 for the fourth straight month. After very poor figures in a weather-afflicted December-January period, job growth appears to be solidly back on track, averaging 231,000 in net payroll gains since February. The prior two months were revised down by a combined 6,000 jobs.

It is worth noting that May’s employment gain pushed the US labor market back to its pre-recession peak for the first time since the financial crisis. As illustrated in the chart below, this was by far the slowest jobs recovery of the post WWII era at approximately six and a half years. The next longest occurred in the 2001 recession, with a recovery period of just under four years.

Source: Calculated Risk

The bulk of May’s job gains occurred in professional & business services, health care & social assistance, and food services & drinking places, the latter of which is a sub-industry of the leisure & hospitality sector. These groups added 55,000, 55,000, and 32,000 respectively. A large chunk (20,000) of the professional & business services gain occurred in employment services, however, which houses the temporary help service category. The nonfarm payroll survey does not distinguish between full-time and part-time jobs in its measure; thus, temporary help employment serves as a measuring stick for the quality of job gains. The measure has increased by 224,000 jobs over the past 12 months.

The household survey remained unchanged, with the unemployment rate sticking at 6.3%. The reading fell a precipitous 0.4% in the previous month, but no retracement occurred this time around. The previous unemployment rate decline was largely associated with a sharp drop in the labor force participation rate, from 63.2% to 62.8% in April. The participation rate was unchanged in May.

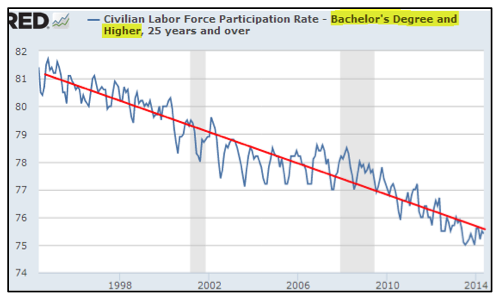

There is growing debate over whether the substantial decline observed in the labor force

participation rate is a cyclical or structural occurrence. The measure actually peaked in 2000 and has been on the decline ever since; however, the pace of declines accelerated during the financial crisis and has yet to let up.

Source: zerohedge.com

Analysis by Sober Look suggests this phenomenon is not a homogenous one, and that a bifurcation between skilled and unskilled workers has created a more complex set of dynamics underneath the surface. While the skilled investor base (denoted here as those with a college degree) has experienced a steady decline in participation over the past 20 years, the decline among those without a high school education looks like a more cyclical development, coinciding with the financial crisis in 2008. Sober Look attributes the secular decline of skilled workers to the gradual migration of Baby Boomers into retirement.

Source: Sober Look, St. Louis Fed

Source: Sober Look, St. Louis Fed

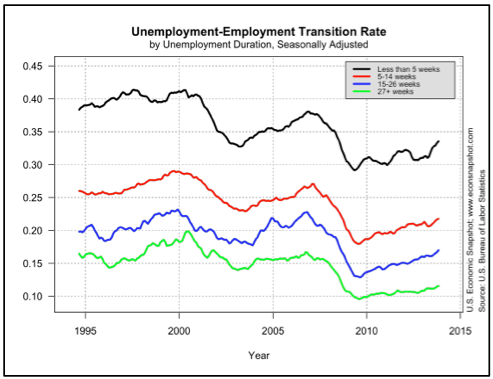

The implications of this phenomenon could further complicate the Fed’s approach to monetary policy in the coming months and years. While there are reports that prospects for the short-term unemployed are improving rapidly, those for the longer-term unemployed remain stagnant. This sentiment is illustrated in the chart below produced by U.S. Economic Snapshot, which shows the probability of finding employment for groups of various unemployment durations.

Source: US Economic Snapshot

Fed officials will have a tricky chore ahead of them in evaluating just what constitutes a healthy labor market in this new normal. A growing two-speed recovery is distorting the meaningfulness of traditional unemployment statistics; in retrospect, the Fed’s abandonment of the 6.5% threshold for reversing ZIRP was clear acknowledgement of this issue. Unfortunately, that leaves investors with a much higher degree of ambiguity as the Fed unwinds from an unprecedented period of monetary accommodation.

The week ahead

Economic data is on the lighter side this week. NFIB’s small business optimism survey and the University of Michigan’s Consumer Sentiment index are slated to report. Also on tap are wholesale inventories, advanced retail sales, and business inventories. More insight on the direction of inflation will be provided via the release of the Import Price and Producer Price indexes.

Notable central bank meetings this week include New Zealand, Indonesia, Chile, and Korea. The Bank of Japan will meet Friday to wrap up the week.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

For more information, please visit our website at http://www.Fortigent.com.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value