The ECB finally acts and hopes for a good reaction

Many have criticized the European Central Bank (ECB) for preferring words over action in recent months. So credit must be given to ECB President Mario Draghi and his colleagues for enacting a series of measures aimed at shaking the eurozone from its malaise. The question is whether yesterday’s decision will result in more credit given to eurozone borrowers.

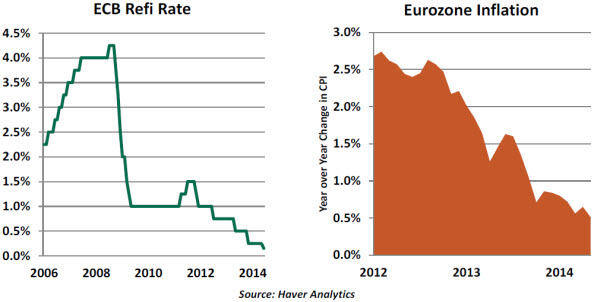

As expected, the ECB lowered its key interest rates. In particular, it pushed into negative territory the rate paid to banks for deposits held with the ECB. In theory, this should increase incentives to lend. This is the first time that a major central bank has broken the “zero nominal bound,” and the reaction of intermediaries to the new environment will be closely watched.

In addition to this groundbreaking step, the ECB will again offer inexpensive funding to euro-area banks. These funds can be obtained for up to four years if the institution can demonstrate that the funds have been used for new loans. (They will be recalled after two years if this standard is not met.) The ECB will also stop sterilizing some of the short-term money market operations it conducts, allowing the money supply to grow more freely.

The ECB had no choice but to capitulate. Its assertion that inflation would stabilize and normalize was at odds with the data. With the risk of deflation rising, something had to be done. The decision, at least this time, was said to be unanimous.

Getting credit flowing will remain a problem. Eurozone banks are in the midst of a stress test, with results to be announced in October. They may be very reluctant to get aggressive with their balance sheets during this period and may choose to simply use the new term funding to replace more-expensive liabilities. This was the fate of similar programs the ECB conducted in recent years.

Mr. Draghi noted that the ECB was also at work on a program to purchase asset-backed securities (ABS), an effort which would be much more similar to the quantitative easing conducted by the Federal Reserve. However, the ABS market is very small in Europe, limiting the potential impact of this strategy. And as we’ve written, any asset purchase program will encounter the complication of deciding which assets to buy, from which countries, at what price.

The euro did not weaken further on yesterday’s announcement, having depreciated importantly when Mr. Draghi foreshadowed the move last month. The ECB was likely hoping for more of a currency retreat, which helps reduce imported deflation and opens export markets for eurozone producers.

The currency markets may be looking beyond yesterday’s action and wondering what (if anything) might follow. Mr. Draghi was fairly clear that no further rate reductions are anticipated, and additional forays into quantitative easing must be carefully choreographed.

From here, all eyes will be on the lending aggregates in the eurozone and the reaction of banks and their clients to negative rates. The outcome of yesterday’s ECB decision is uncertain, but doing something certainly beats doing nothing.