The very first index fund, created by Wells Fargo in 1970, equal-weighted the stocks in the NYSE index. But it didn’t last very long. The process of trading stocks to maintain equal weights was too time consuming and costly.1

That historical outcome might surprise modern investors. Consider, however, that until 1975 the brokerage commissions were set by NYSE (even for institutional trading), and they were 10–15 times higher than they are today (Eisenach and Miller, 1981). In addition, computers were just emerging on Wall Street, and the effort involved in making them work often exceeded any benefits they offered. Because equal weighting was impractical in those times, capitalization weighting—a buy-and-hold strategy for index investing—became the predominant industry standard.

By the 1990s, however, major index providers started offering equal-weight versions of certain indices. In the past decade, the range of equal-weight indices increased, and ETFs and other investable vehicles linked to these indices came to market. More than 40 years after the first attempt, equal weighting finally took off as a viable approach to index investing.

It might seem that an investment strategy as incredibly simple as equal weighting couldn’t possibly offer anything of interest to sophisticated investors. But equal weighting should not be dismissed so quickly. Without a material increase in risk, the equal-weight strategy robustly outperforms the traditional cap-weight benchmark on a gross basis.

If equal-weighted strategies are not only easy to understand but also provide better risk-adjusted returns than cap-weighted indices, why should anyone bother with a more complicated smart beta strategy such as a fundamentally weighted index? For two reasons: A fundamentally weighted index outperforms its equally weighted counterpart before accounting for costs; and it also has lower implementation costs. In addition to reviewing simulated performance records, we will describe the mechanism that drives the returns of both smart beta strategies, and we will explain why selecting and weighting stocks on the basis of fundamentals uses the mechanism more efficiently.

Both fundamental and equal-weight strategies owe their attractive performance to the noise in prices—the fact that stocks are often mispriced—and the tendency for stock prices to reverse direction and head back toward their long-term averages. Stocks that are temporarily overpriced automatically receive a higher weight in the cap-weighted benchmark; conversely, stocks that are temporarily underpriced are given a lower weight. This internal dynamic causes a performance drag for the cap-weight strategy: it overweights expensive stocks, magnifying the adverse return impact when their prices revert toward the mean, and it underweights cheap stocks that may be poised to rise in price.

In comparison, fundamentally and equally weighted strategies avoid the return drag because they do not use prices as weighting inputs.

Nonetheless, there are important differences between the two strategies. First, the equal-weight strategy disregards not only stock prices but also the size of the companies in the index. Consequently, it takes disproportionate positions in smaller—and therefore less liquid—stocks. These bets only indirectly capture the noise in prices, and are therefore less effective in generating performance. In addition, as one might expect, they create very significant implementation costs. The fundamental-weighted strategy breaks the link between stock price and index weight while still maintaining a high degree of investability. It achieves this by maintaining a systematic relationship between a company’s index weight and its economic size, as reflected by the financial variables that serve as weighting factors.

Second, equal-weight strategies select the stocks they hold by market capitalization (when, for example, their construction rule is to equal-weight the largest 100 stocks in a given universe). Fundamental indexing selects as well as weights stocks on the basis of fundamental metrics. This key methodological difference contributes to the performance advantage enjoyed by fundamentally weighted strategies: the stocks that are selected by the equally weighted index, and not by the fundamentally weighted strategy, are more likely to be overpriced. The selection effect would disappear if the equal-weight strategy were to invest in the entire universe of stocks; however, this would further impair investability, because microcap stocks would get the same allocation as the largest of the large-cap stocks in the opportunity set.

Comparative Returns

In a long-run simulation, fundamentally weighted strategies outperformed equal weighting by as much as 280 bps.

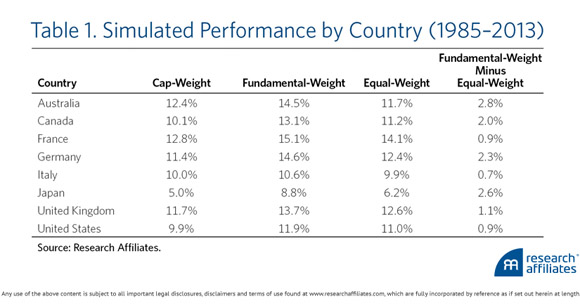

Table 1 shows the hypothetical performance of the two smart beta strategies and the cap-weight benchmark in multiple countries from 1985 to 2013. Here, the starting universe is set to the 85th percentile by cumulative market capitalization (for the cap-weight and equal-weight strategies) or by cumulative fundamental weight (for the fundamental strategy). This threshold leaves a modest amount of room for the selection effect to play a role. Over the measurement period, the annualized returns of both smart beta strategies exceed those of the cap-weighted benchmark in almost every case, and the fundamentally weighted index consistently outperformed the equally weighted one.

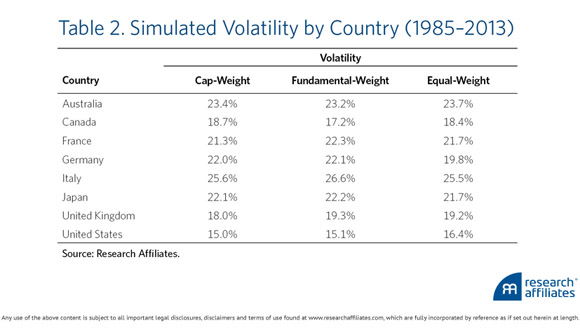

An argument sometimes heard in favor of equal-weight strategies is their greater diversification compared to the fundamental-weight strategy. In itself, however, diversification is not the ultimate goal; rather, it is a means to achieving the desired risk characteristics. And, as can be seen from Table 2, the volatilities of the equal-weight indices are roughly the same magnitude as those of the fundamentally weighted indices. It may be surprising that the much broader diversification of the equal-weight strategy does not ensure materially better risk characteristics. However, most of the benefits of diversification can be achieved with a relatively small number of stocks; incrementally reducing concentration results only in marginal improvements.2

Relative Implementation Costs

In estimating implementation costs, we focus on what happens upon rebalancing the non-price weighted indices, because that’s where most of the cost variation across the strategies occurs. Our cost model assumes that the cost of trading a security is proportional to the fraction of its volume being traded.3

Intuitively, allocating a large weight to stocks with low liquidity (as measured by trading volume) should result in higher trading costs. In that respect, the equal-weight suffers greatly relative to both the fundamental- and cap-weight strategies.

It is obvious that the strategy with the higher turnover will cost more to trade. A more careful examination suggests that a given amount of turnover is more costly if it is caused by replacing a stock rather than trading a stock back to its target weight. This finding lends the fundamental strategy a further advantage, because stock selection by fundamental score is more stable than it is by market capitalization.

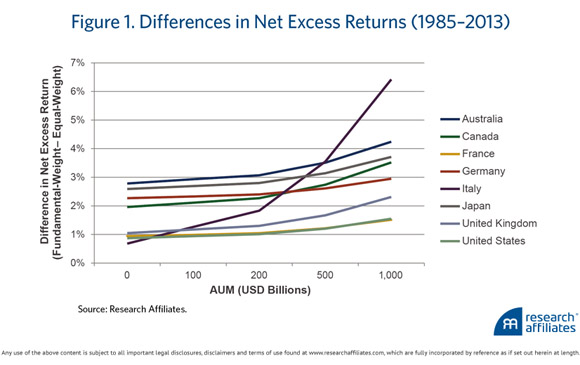

Of course, if the total size of the assets invested in a strategy is very small, the market impact at rebalance is not a concern. To obtain an estimate of the costs, then, we need to specify the amount of assets. Figure 1 shows the differences in simulated excess returns, net of costs, after adjustment for various amounts of assets under management.4 The lines slope upward, demonstrating the progressively superior results of the fundamentally weighted indices, because the net-of-cost performance of the equal-weight strategy falls off with asset size much faster than does that of the corresponding fundamental-weight strategy.

In Closing

Explicit transaction costs are much lower today than they were when Wells Fargo first experimented with index investing. Nonetheless, equal weighting still entails high turnover, often in less liquid stocks. Our study of the market impact of index rebalancing demonstrates that portfolio construction methods potentially make a big difference in investment results. Equal weighting is simple—easy to grasp and easy to explain—but its simplicity comes at a price. Over the long term, and over a very wide range of global AUM, fundamentally weighted smart beta strategies are likely to outperform the equal-weight approach. The prospective performance advantage results in part from the selection effect and in part from the implicit cost of trading. In smart beta investing, as elsewhere, implementation matters.

Endnotes

1. Clowes (2000), pp. 85–86; Fox (2009), p. 125.

2. A portfolio whose top three stocks account for 60% of the weight can be greatly improved by reducing the concentration by half. A portfolio where the top three stocks account for 10% of the weight is already well-diversified, and reducing the concentration by half has little if any impact.

3. For a complete description of Research Affiliates’ market impact model, see Aked and Moroz (2013).

4. In Figure 1, assets are allocated to the countries in proportion to market capitalization in order to create a meaningful cross-country comparison of costs. Because the Research Affiliates market impact model has to be calibrated to a specific index, we standardize all results to correspond to a 50 bps market impact for the $2 trillion in the U.S. market cap-weighted strategies.

References

Aked, Michael, and Max Moroz. 2013. “The Market Impact of Index Rebalancing.” Research Affiliates White Paper.

Clowes, Michael J. 2000. The Money Flood: How Pension Funds Revolutionized Investing. New York: John Wiley & Sons, Inc.

Eisenach, Jeffrey A., and James C. Miller III. 1981. “Price Competition on the NYSE.” Regulation, vol. 5, no. 1 (January):16-19.

Fox, Justin. 2009. The Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall Street. New York: HarperCollins.