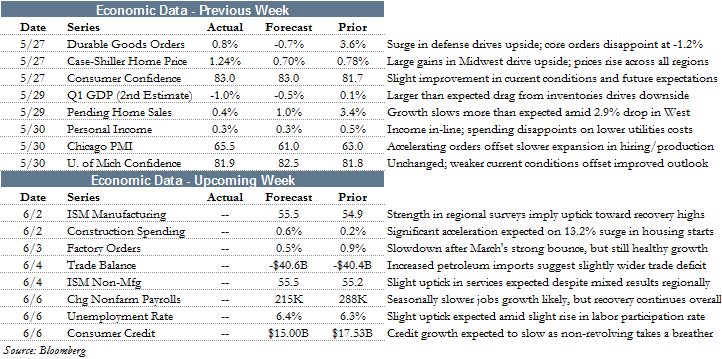

GDP Doesn't Disappoint?

Equity markets finished the month of May in positive territory with the S&P 500 gaining 1.2% on the week. Small cap stocks continued to lag large caps as the Russell 2000 finished the week up 0.8%. On the month, the S&P 500 gained 2.3% while the Russell 2000 gained 0.8%.

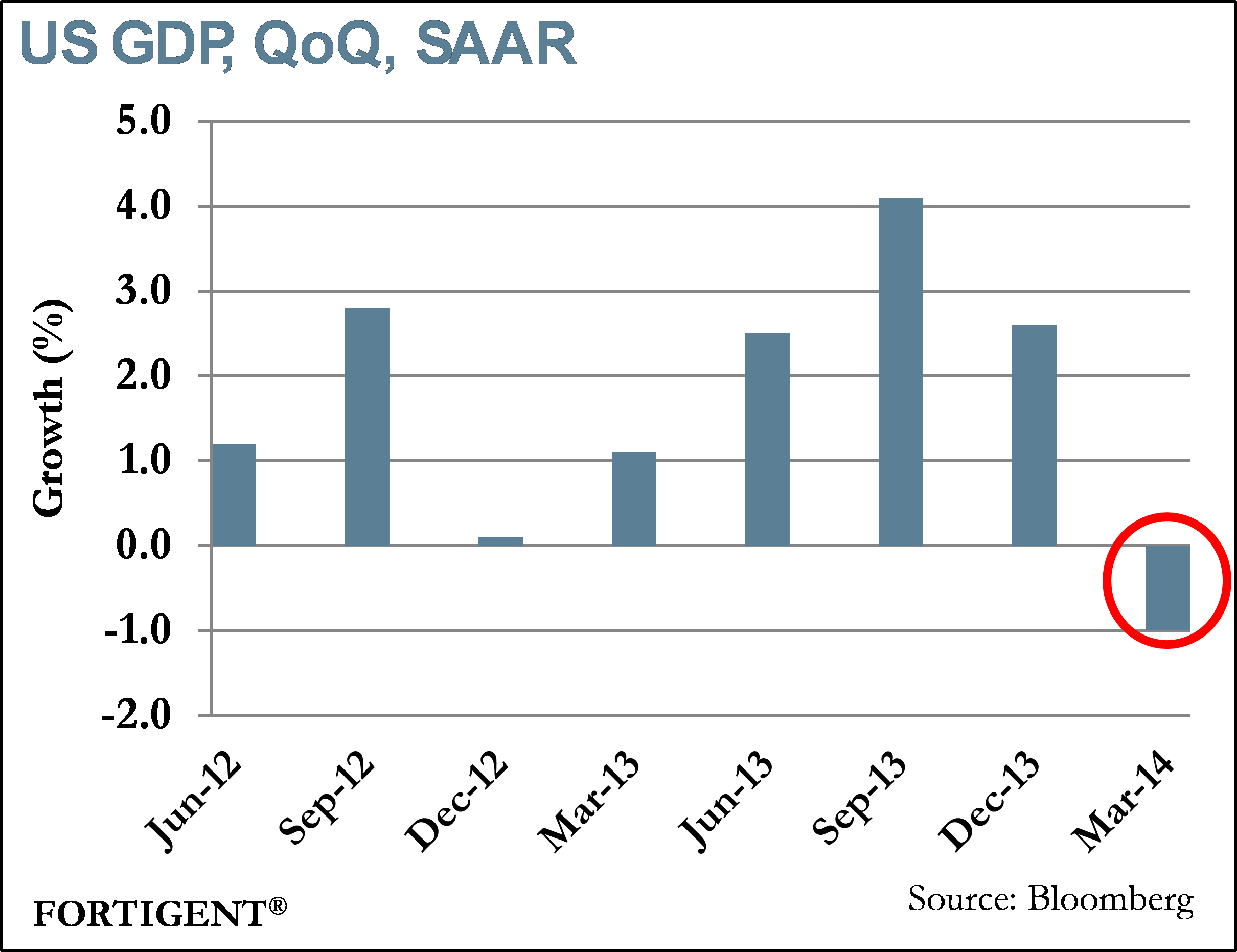

News last week was centered around the second estimate of first quarter GDP which showed the U.S. economy contracted by 1.0% quarter-over-quarter. This is a substantial fall relative to consensus forecasts of a 0.5% decline.

Investors did not seem overly concerned with the disappointing GDP revision as markets remained in positive territory. The primary reason the pronounced negative revision was due to the larger than previously estimated decline in private inventories. Private inventory investment declined due to the build up at the end of 2013 coupled with stalling economic activity during January and February. A wider than originally reported trade deficit also weighed on GDP growth as imports jumped. Stripping out trade numbers and inventories, GDP was revised up to 1.6% from 1.5%.

Economists remain confident in U.S. growth going forward as consumer spending (which accounts for 70% of GDP) remains strong. Given the downward revision to first quarter GDP growth, economists are calling for a significant bounce back in the second quarter on the back of an anticipated rise in private inventory investments.

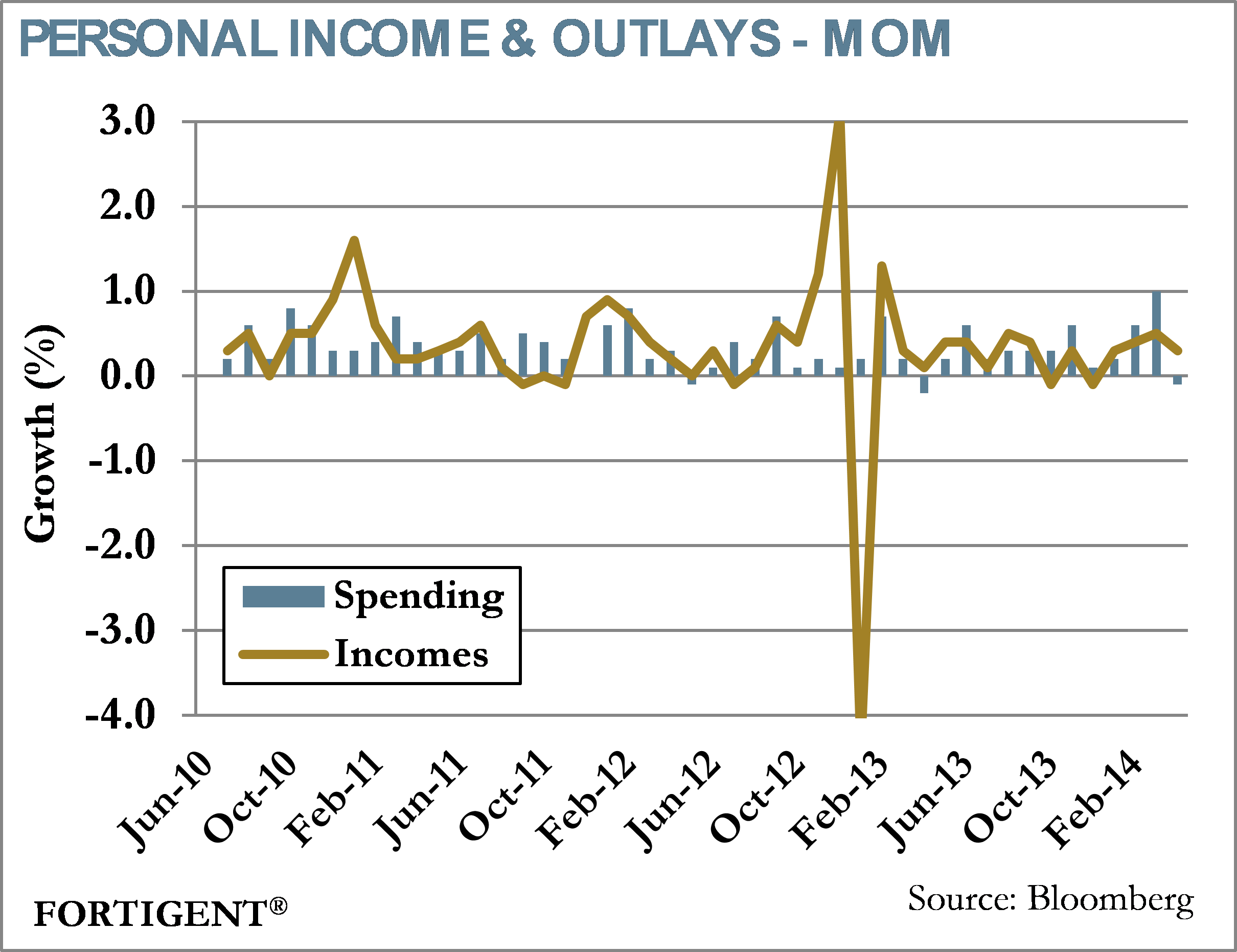

As alluded to above, personal income is one area of the economy that continues to show improvement. Personal income growth was in line with expectations of 0.3% month-over-month in April. Personal expenditures, however, decreased 0.1%. Despite slower consumer spending in April, positive income growth coupled with an increased savings rate is broadly interpreted as positive for consumer health. As a percentage of disposable income, the personal savings rate jumped 4.0% in April, relative to 3.6% in March.

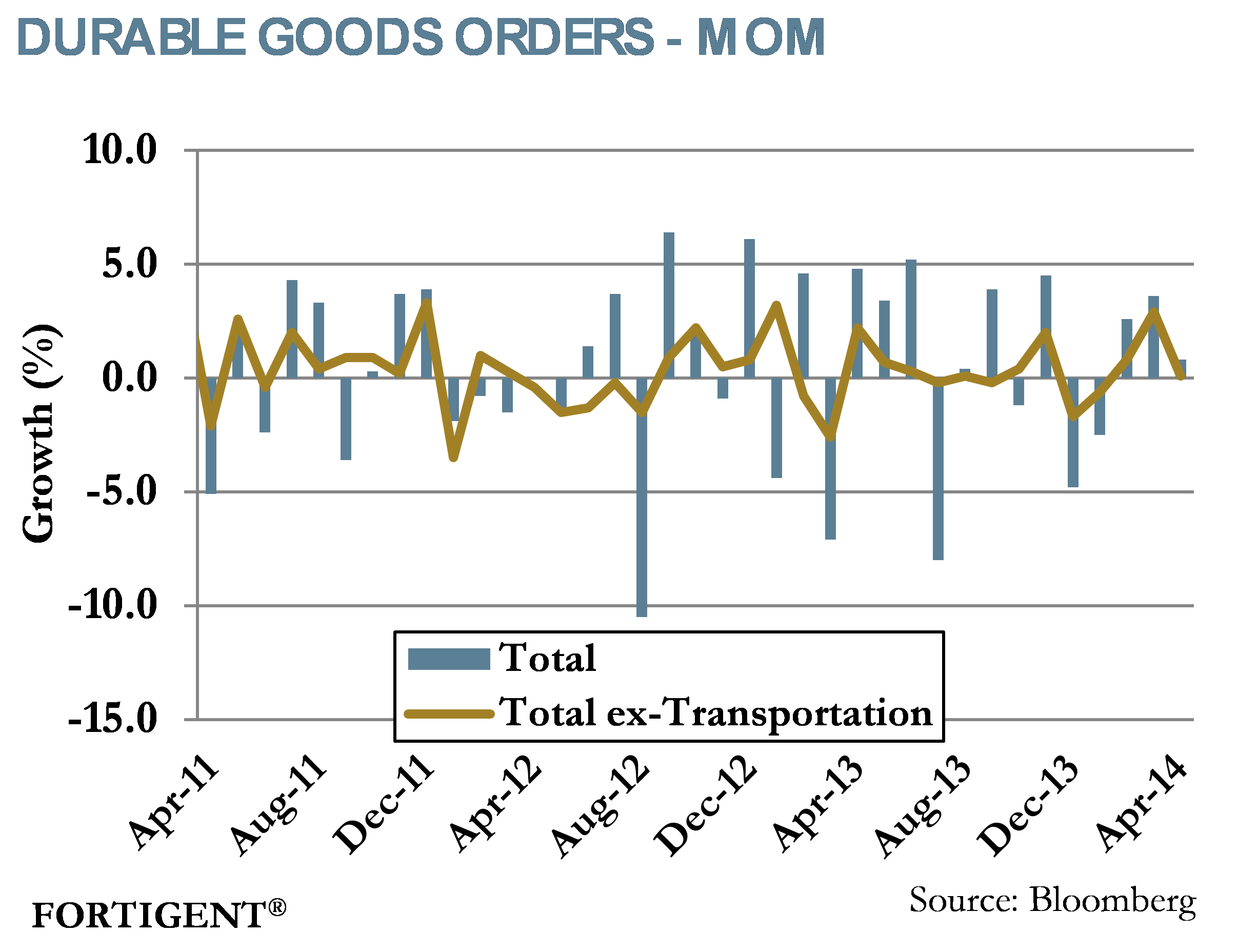

Durable goods orders unexpectedly increased in April by 0.8%. This came on the back of a surge in defense spending. However, excluding the defense component, orders would have declined 0.8%. Economists are calling for a significant rebound in the coming months given the pent up consumer demand from the winter months.

On the housing front, housing prices continued to climb, albeit, at a slowing rate. The S&P/Case-Shiller Home Price index increased roughly 1.2% month-over-month in March, exceeding expectations of a 0.7% increase. However, year-over-year growth slowed to 12.4% in March from 12.9% in February, a reflection of weaker homebuyer demand. This is confirmed by slower pending home sales growth. Pending home sales growth rose 0.4% month-over-month, coming in well below expectations of a 1.0% increase.

Mixed data coming out of the housing market continues to be the subject of debate by many economists as questions surround Fannie Mae and Freddie Mac’s roles moving forward. Debate surrounding the government-sponsored enterprises has grown more heated recently as the Fed continues to taper its asset-purchasing program and home loans grow more expensive.

Corporate Activity Flourishes

With the backdrop of low interest rates, and sluggish revenue growth, 2014 has been the year that M&A activity finally blossomed. Companies are growing more aggressive in their acquisition tactics, leading to many high profile mergers and numerous opportunities to improve profitability.

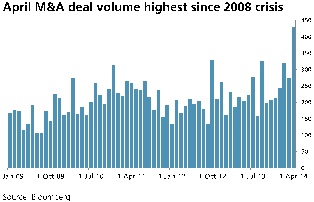

M&A activity was up 99% year-over-year in April, reaching its highest point since 2008. The announcement of very large potential deals such as Allergan’s bid for Valeant, and Lafarge’s bid of Holcim, led to a rapid uptick of activity during the month.

Source: UBS

Behind the uptick in activity is particularly robust interest in larger deals. There have already been 19 deals announced worth a value of $10 billion or more, with another 215 deals between $1 billion and $10 billion, according to Barron’s.

The nature of M&A has undergone a shift this year, however. Previously, companies were shy about more aggressively pursuing acquisitions due to fears of shareholder resistance, but this year aggressive tactics are all the rage. The Wall Street Journal reports that unsolicited takeover bids hit $97.3 billion this year, accounting for 7% of all global bids, the highest point since 2007.

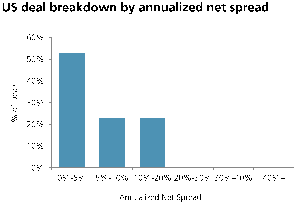

Increased M&A activity typically should be beneficial for merger arbitrage investors, but it is actually proving to be more beneficial for activists. With massive amounts of liquidity moving about the world, opportunities to capitalize on announced deals are severely limited. UBS estimates that the annualized spread on announced deals is 5.5% at the end of April.

Source: UBS

Announced deals may not make a ton of sense in the current environment, but M&A activity is likely to remain high, acting as a tailwind for activist, special situations, and broader long-only investment strategies. During 2013, the average acquisition premium was 18%, suggesting that it pays to be invested ahead of the announcement. Investors should also exhibit caution, though, as any sign that M&A activity is accelerating uncontrollably could be an indication that all caution is being thrown to the wind. That is not the case for now, but could happen with very short notice.

The Week Ahead

Economic data continues to pour in this week with both manufacturing and service data coming out. Also on tap is the monthly jobs report where unemployment is expected to rise to 6.4% on an increase in labor participation.

Notable central bank meetings this week include Australia, India, the UK, and the ECB. Policy decisions coming out of the Euro Area will be heavily watched as investors are expecting the ECB to cut rates across the board.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value