Tax-Exempt Securities Confounding the Consensus in 2014

- Blame the central banks

- Six factors supporting the tax-exempt market

- Beware of the "de minimis" tax threat

- Update on municipal credits in the news

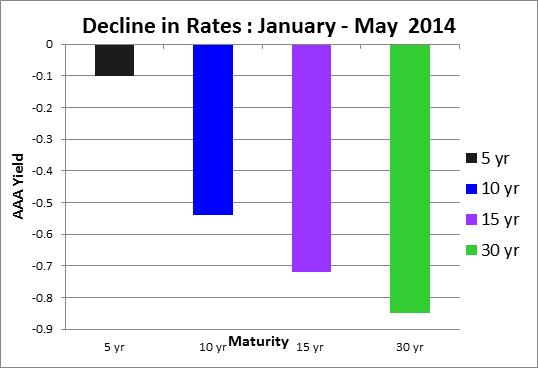

Rarely do the financial markets provide the double treat of simultaneously rising equity valuations and falling bond yields. Almost midway through the second quarter of 2014, key stock indices reached new all-time highs while global bond yields have retreated to levels not seen in over six months. Something has to give: either stock prices retreat or yields rise. Right? At least this is the popular assumption supported by classic economic rationale for a normal investment environment.

But all is not normal according to the markets. If it were, then stocks should continue their ascent and bond yields should be on an upward trajectory due to strengthening global economies, just as the consensus predicted at the start of the year. Why is this not happening? The heavy hand of global central banks continues to play the leading role in the economic recovery story. Assurances by the Fed's chair that the U.S. central bank will "remain accommodative" for an unspecified period has buoyed both domestic equity and fixed income markets. Persistent low inflation and an uneven labor market recovery are worrisome. Internationally, the picture is equally cloudy. The precipitous decline in Eurozone bond yields is likely a reflection of even greater economic recovery skepticism in Europe than in the U.S. Sluggish growth in Japan and many emerging economies (i.e., China) will likely sustain accommodative monetary policies around the world. A significant rise in global interest rates appears unlikely any time soon in our view.

We have identified a number of factors likely to be supportive of the tax-exempt market over the near-term.

1. Municipal bond yields are attractive based on historical relationships relative to U.S. Treasuries. The comparative "cheapness" broadens the potential investor base on a taxable- equivalent basis. Sustained investor demand for government debt could be a market prop going forward.

2. Municipal bond new-issuance is contracting. Net supply is estimated to be $24 billion (8%) lower by street estimates versus 2013.

3. Retail demand is increasing. According to Lipper Analytics, $1.78 billion of inflows have gone into tax-exempt funds YTD (through May 7), with most of the purchasing occurring in recent weeks.

4. The "capitulation" trade might be unfolding. Dramatic declines in global bond yields since the beginning of the month suggest investors might be throwing in the towel on the expectation for both rising rates and stock prices. While still too early to tell, the old stock adage, "sell in May and go away" might be unfolding once again in 2014.

5. The peak municipal market reinvestment period is approaching. Historically, the largest reinvestment of coupons and maturing bonds occurs in the months of June-August. According to JP Morgan, $10 billion will need to be reinvested this summer, equivalent to two-months of new tax-exempt issuance.

6. Property and casualty insurers will likely increase buying of tax-exempt debt due to the roll-off of tax loss carry forwards incurred during the financial crisis and the need to reinvest the maturity proceeds of significant bond purchases made between 2004 and 2008.

The move to lower tax-exempt rates over the past several months has initiated a move by new-issue underwriters to issue bonds bearing lower coupons. Potentially, this could impact liquidity and adversely impact the pricing of these securities should they become subject to the "de minimis" tax. Investors should be cognizant. We prefer the purchase of premium to discount bonds.

Source: SMC FIM and Thomson Reuters

Credit update:

Puerto Rico and Detroit

The news out of Puerto Rico continues to be mixed. On the positive side, the unemployment rate on the island continues to decline. Governor Padilla has announced a $6.9 billion balanced budget proposal for 2015 that calls for $1.4 billion in spending cuts and no deficit financing. While the proposal is light on specifics, a combination of economic growth initiatives and austerity measures are proposed. No layoffs or new taxes are anticipated. Notably absent from the plan is any discussion of a possible restructuring of the Commonwealth or any of its agencies, although the government announced that it had recently hired a restructuring specialist.

Negative news has come from the Puerto Rico Supreme Court, which struck down many cost-saving reforms legislated last year to address the high pension costs embedded in the Teachers' Retirement System. In addition, the Commonwealth reported an anemic 0.1% growth rate in the first quarter. Although the economy is still contracting, it is doing so at a decelerating rate. Adding to the negative news, the government's revenues were 4.4% below projections through April. By comparison, revenues through March had been 1.25% above projections.

In recent weeks Detroit has made progress toward an exit from bankruptcy by striking deals with pensioners and unlimited-tax general obligation bondholders (UTGO). The feasibility and final outcome of Detroit's bankruptcy plan remains highly debatable. To address this question, the presiding bankruptcy judge has engaged a municipal finance expert witness and a court consultant. A trial on the final plan is now scheduled to begin in late July.

The tentative settlement with the UTGO bondholders would have the City pay 74 cents on the dollar or approximately $388 million on allowed aggregate claims. The judge has ordered mediation sessions between the City and its creditors to continue. If the City is unable to settle with its remaining creditors, it could consider asking the court for a "cram down". A cram down would allow for confirmation of a plan of adjustment without the agreement of creditors.

Disclosures

The information provided in this commentary is not intended to be a complete summary of all available data. Certain information contained herein has been obtained from published sources and/or prepared by sources outside SMC Fixed Income Management (“SMC FIM”), a division of Spring Mountain Capital, LP, and certain information contained herein may not be updated through the date hereof. While such sources are believed to be reliable, no representations are made as to the accuracy or completeness thereof by SMC FIM or any of their respective affiliates, directors, officers, employees, partners, members or shareholders, and none of the former assumes any responsibility for the accuracy or completeness of such information. Nothing contained herein shall be relied upon as a promise or representation as to past or future performance.

This commentary does not constitute an offer to sell or a solicitation of an offer to purchase securities, or any other product sponsored or advised by SMC FIM or its affiliates, nor does it constitute an offer or a solicitation to otherwise provide investment advisory services. It should not be assumed that any of the security transactions listed were or will prove to be profitable, or that the investment recommendations we make in the future will be profitable.

Statements contained in this commentary that are not historic facts are based on current expectations, estimates, projections, opinions and beliefs of SMC FIM. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Unless specified, any views reflected herein are those of SMC FIM and are subject to change without notice. SMC FIM is not under any obligation to update or keep current the information contained herein.

This commentary does not take into account any particular investor's investment objectives or tolerance for risk. The information contained in this commentary is presented solely with respect to the date of its preparation, or as of such earlier date specified in it, and may be changed or updated at any time without notice to any of the recipients of it (whether or not some other recipients receive changes or updates to the information in it).

No assurances can be made that any aims, assumptions, expectations, and/or objectives described in this commentary will be realized. None of the authors, SMC FIM, or any shareholders, partners, members, managers, directors, principals, personnel, trustees, or agents of any of the foregoing shall be liable for any errors (to the fullest extent permitted by law and in the absence of willful misconduct) in the information, beliefs, and/or opinions included in this commentary or for the consequences of relying on such information, beliefs, or opinions.

Neither this commentary, nor any of the contents hereof, may be reproduced or used for any other purpose, or transmitted or disclosed in whole or in part to any third parties, in each case without the prior written consent of SMC FIM.

Copyright © 2014 Spring Mountain Capital, LP. All rights reserved.