Going into the holiday weekend, equity markets ended the week up with the S&P 500 gaining 1.2%. The NASDAQ reversed the prior week’s losses, ending last week with a gain of roughly 2.3%. Of particular note, growth stocks continued their outperformance on the quarter relative to value stocks. The Russell 3000 Growth index was up 1.6%, exceeding the Russell 3000 Value index’s 1.0% gain. On the quarter, growth is up 1.3% while value is up 1.0%.

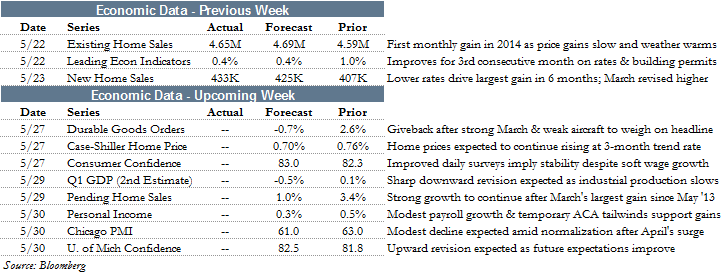

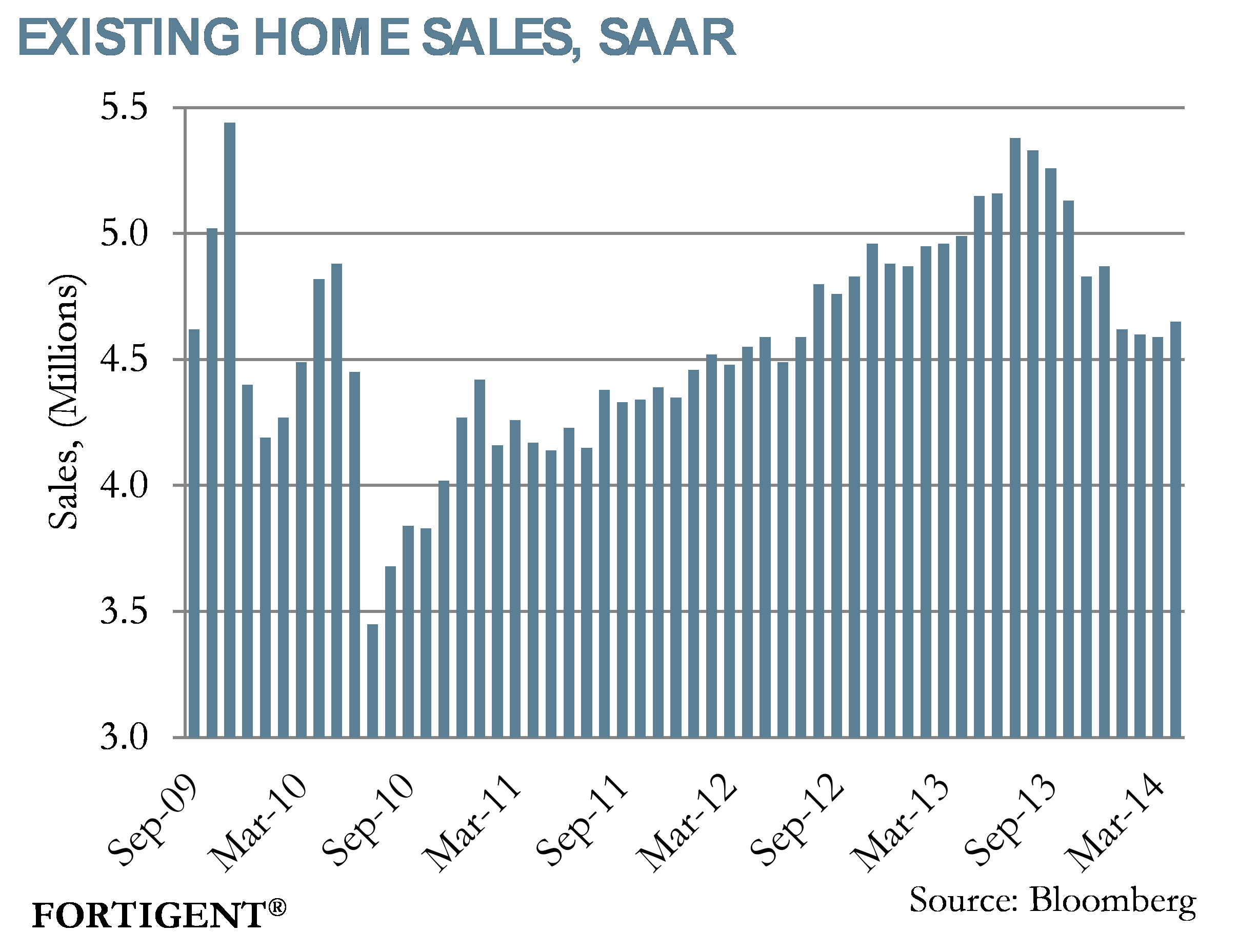

Housing data last week brought a bit more clarity to the direction of the housing market. Existing home sales increased 1.3% in April bringing the annualized growth rate to 4.65 million units. Despite the month-over-month jump in existing home sales, sales are still down over 13% from the July 2013 peak where the annualized growth rate stood at 5.38 million units.

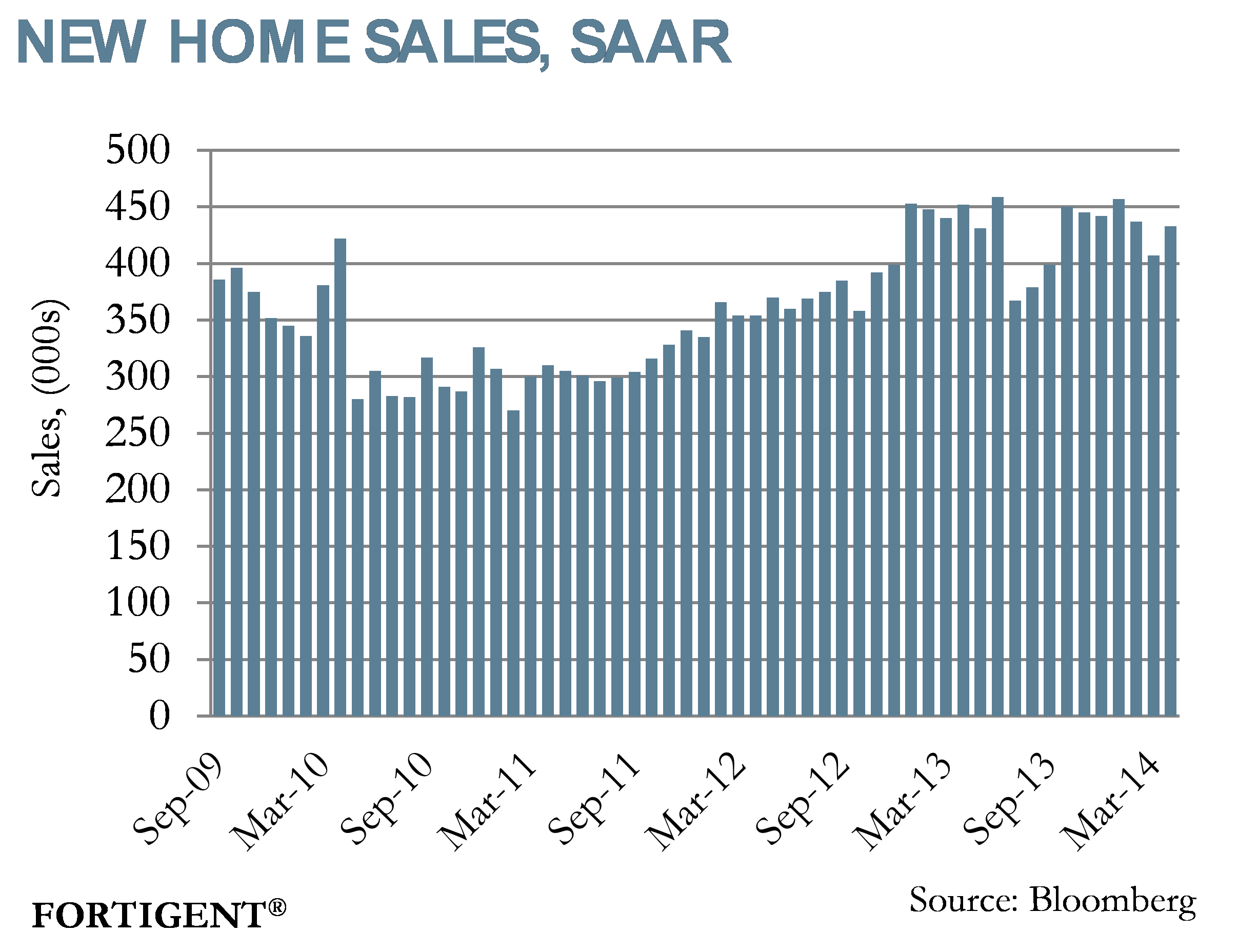

New home sales followed suit rising approximately 6.4% in April. The jump from 407,000 units to 433,000 units exceeded economists’ estimations, which were calling for an increase to 425,000 units. However, consistent with existing home sales data, new home sales data still lag their June 2013 peak of 459,000 units.

Despite recent bouts of positive housing data, many are concerned with the direction of the housing market over the next 6-12 months. Drop-offs in economic data coming out this year have been regularly rationalized as being the result of the unusually harsh winter weather in January and February. Despite the recent uptick in April’s housing numbers, data dropped off months prior to the unanticipated severe winter weather.

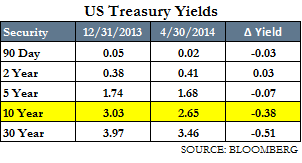

Housing economists have cited a number of factors that have contributed to the slowdown within the housing market. Rising interest rates have been cited as a primary culprit over the preceding 18 months. But, the U.S. 10 year has unexpectedly trended down since the beginning of the year, touching as low as 2.50%. This has translated into less expensive home loans and, less talked about, improved psyche of underwriters and those alike who observe the movement in the 10-year rate when constructing home loans for potential homebuyers and, subsequently, further home sales growth.

Outsized housing price appreciation has also been cited as a reason for the slowdown as home prices have increased roughly 25% since its bottoming out in March 2012. Housing prices have recently slowed providing buyers with an attractive buying opportunity as evident by the recent jump in home sales.

Whatever the reason is for the recent slowdown in the housing market the consumer at large will be crucial for the health of the housing market going forward. As reported last week, confidence among homebuilders fell in May to its lowest level since May 2013 as measured by the NAHB/Wells Fargo Housing Market index. Consumer confidence was cited as the biggest drag on homebuilder confidence as “builders are waiting for consumers to feel more secure about their financial situation.” Personal income growth, which comes out this week, will provide further insight behind the direction of the housing market.

The Week Ahead

This week is full of economic data with the Case-Shiller Home Price index coming out. Also coming out is data on durable goods orders and consumer confidence. On tap for later in the week is the second estimate of Q1 GDP, pending home sales, and personal income growth.

Notable central bank meetings this week include the Central Bank of Brazil and the Central Bank of Egypt.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value