Scarce Growth - Can the Tortoises Continue to Outpace the Hares?

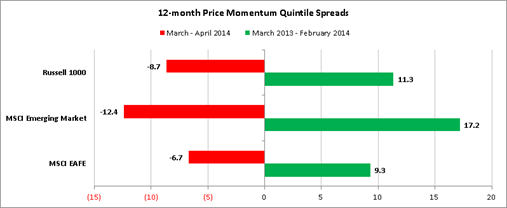

For some time we have suggested that in a world slowly recovering from the 2008 financial crisis, aggregate global growth would be sub-par and that investors would benefit from seeking scarce growth, so long as that growth did not become wildly overvalued. Recent market action has tested that stance severely. Beginning in March we have seen a violent style rotation featuring the selloff of stocks with high price momentum and high growth characteristics. This was not solely a phenomenon within the U.S. equity markets (Exhibit 1). There is significant evidence that the hedge fund community has been particularly hard hit in this reversal, exacerbating the issue as levered portfolios have been forced to liquidate assets, fueling ongoing pressure on many “growthier” segments. So, where do we go from here? Is it time to seek market shelter, or has this sell-off created opportunity?

Exhibit 1: Price momentum performance, one-year prior vs. March-April selloff

Source: Columbia Management Investment Advisers, LLC. Note: Factor returns are represented by the quintile spreads (not sector neutral, top 20% - bottom 20%, √Benchmark Weights weighted, in USD).

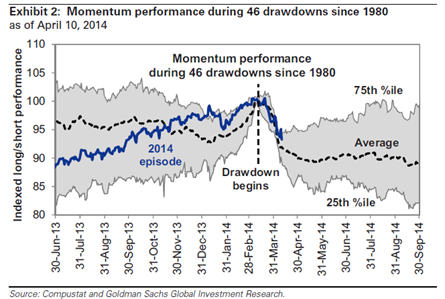

Given the pain this reversal has caused, there has been a scramble for strategists and market commentators to isolate a root cause. Generally, the diagnosis has centered on concerns of 1) slowing global growth, 2) “crowdedness” in the higher growth sectors and 3) valuation. In considering the potential duration of this flight to safety, let me briefly address each of these issues. While we have already felt a significant shift, these sorts of factor regime shifts can be quite persistent (Exhibit 2). However, we appear to be moving into a “sorting out” stage where investors begin to more granularly assess both the fundamentals and the incremental opportunities.

Global growth concerns: There have been data points of concern regarding global growth of late with 1Q U.S. gross domestic product (GDP) extremely anemic, a continued slowdown in Chinese growth and generally uninspiring revenue reports from 1Q earnings in the U.S. and even more so in Europe. However, we continue to see a slow, steady improvement in U.S. growth (evidenced more clearly by the employment data) and a continuation of enough growth in the rest of the developed world to maintain forward progress, but not so much that we lose the support of central bank stimulus. All in all, an environment that continues to support not a “rising tide lifts all boats” outlook, but a world in which organic growers and innovators can stand out and trade over time at reasonable premiums.

“Crowdedness”: In short, if there was crowded trade in higher growth sectors, that ship has sailed. The recent performance pain and related hedge fund liquidations would appear to have significantly reduced that concern. Also, where we had seen modest evidence of market “froth” in the form of frenetic IPO issuance in certain sectors, the pullback seems to have slowed the calendar and applied a higher quality hurdle.

Valuation: Trading at a P/E ratio of around 15X current earnings, the market is in-line with historic averages and does not appear overvalued. However, considering the historically low interest rate environment, equities look remarkably inexpensive compared to fixed income alternatives (including even debt from the same issuer). As for the valuations of premium growers relative to the rest of the market, our work suggests that statistically, the top growers have given back most of their P/E expansion relative to the broader market in this sell-off. So, we do not see overall valuations or the specific valuations of high growers in general as a major issue.

Finally, I would note two things about growth investing. First, exciting things are happening around innovative software, cloud computing applications, industrial automation and biotechnology; these areas are gaining significant share of their broader global industries with real advances in productivity and effectiveness. These are nothing like the “all hype, no substance” companies and concepts we saw during the internet bubble. We don’t see anything broadly in 1Q results to dissuade us from this view; particularly in biotechnology, we have been encouraged by the ground level results, despite the market action. Ultimately, earnings growth is still a powerful driver of longer term investment results and in a world where overall growth appears as if it may remain modest for some time to come, share-gaining innovation remains attractive. Second, not all “growth” names are created equal. As is usually the case in major factor reversals, after an initial surge that does not differentiate between individual stories, there is a “sorting out” period where more fundamental differences at the company by company level become discernable to the markets. Not all Internet and biotech names are created equal and the homogenous ill treatment of these sectors in the last two months creates stock-picking opportunities. Patience and tolerance for ongoing bouts of volatility are crucial in this period, but we believe that those disciplined enough to focus on the underlying fundamentals will ultimately be rewarded.

Disclosure

The views expressed are as of 5/19/14, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

The Russell 1000 Index tracks the performance of 1000 of the largest U.S. companies, based on market capitalization.

The MSCI Europe, Australasia, Far East (EAFE) Index is a capitalization-weighted index that tracks the total return of common stocks in 21 developed-market countries within Europe, Australasia and the Far East.

The MSCI Emerging Markets Index (EMI) is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets. As of June 2006, the MSCI Emerging Markets Index consisted of the following 25 emerging market country indices: Argentina, Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Israel, Jordan, Korea, Malaysia, Mexico, Morocco, Pakistan, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand and Turkey.

The Standard & Poor's (S&P) 500 Index tracks the performance of 500 widely held, large-capitalization U.S. stocks.

It is not possible to invest directly in an index.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2014 Columbia Management Investment Distributors, Inc. All rights reserved.

929613