“The combination of an ownership mentality, long-term perspective, and disciplined capital allocation

– along with Jarden’s portfolio of strong brands – should continue to reward investors.”

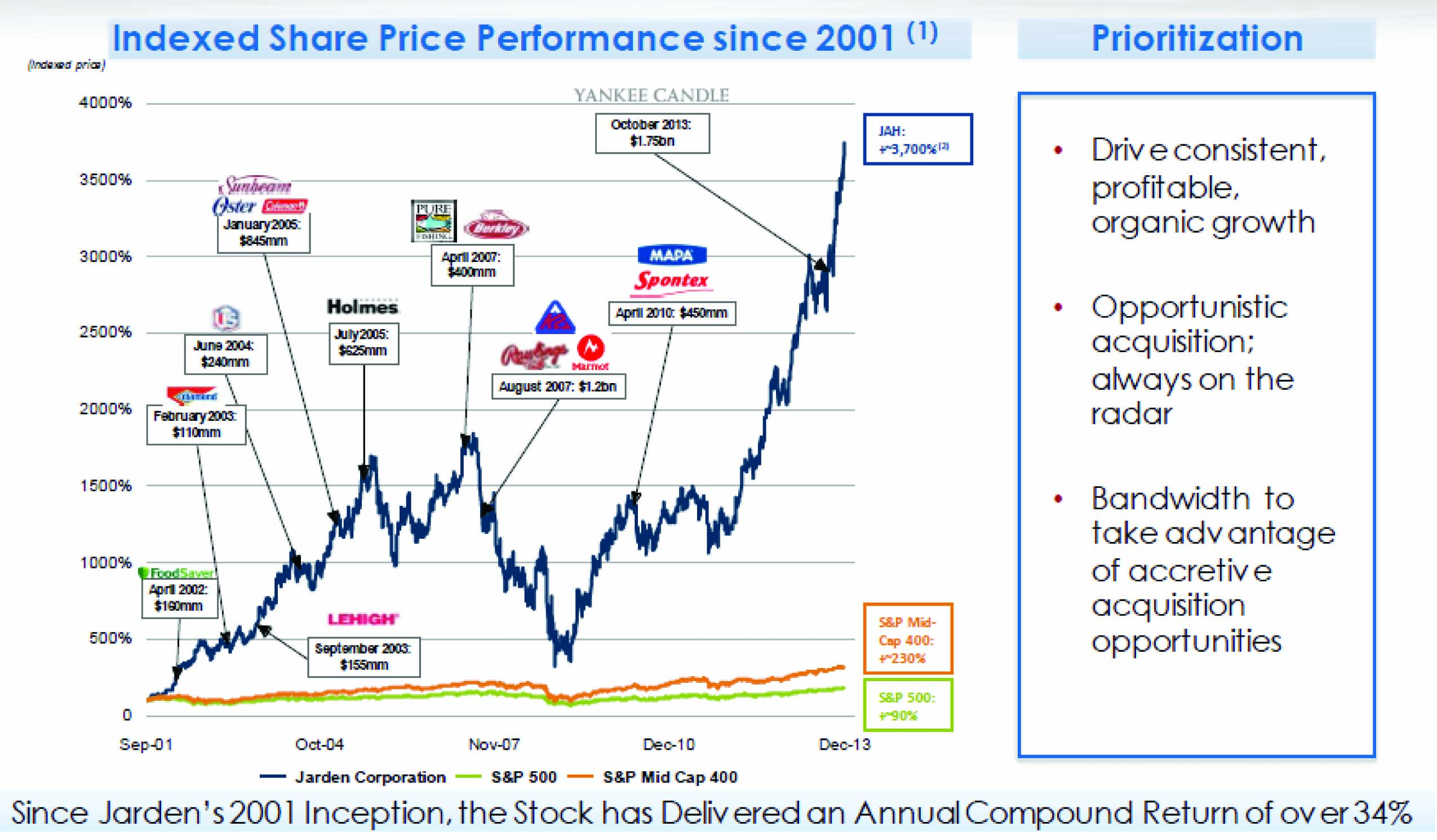

An ownership mentality, long-term perspective, and disciplined capital allocation are characteristics we look for in all management teams but find in few. Through its commitment to these attributes, Jarden Corp. (JAH) has driven significant outperformance for long-term investors and compiled an attractive portfolio of niche brands that are leaders in their respective markets. From September 2001, when Martin Franklin and Ian Ashken were appointed to senior management, through year-end 2013, Jarden has produced a total return of 3,784.36% relative to a cumulative return of 144.40% for the S&P 500 Index and 261.30% for the Russell 2000 Index (See chart below). We believe Jarden continues to be well positioned to achieve top tier results because of its optimal combination of strong leadership – guided by the right incentives and temperament – and a diverse portfolio of strong consumer brands that are well entrenched in their respective categories.

Jarden acquired many of these businesses through opportunistic purchases that met its internal criteria. Management focused on the acquisition of market leading brands that possessed annuity like revenue streams, defensible moats, and strong cash conversion characteristics at attractive valuations. Once acquired, Jarden’s team integrated these companies into its established distribution, manufacturing, and back office infrastructure, leveraging their scale to organically grow the top line and improve the businesses’ economics.

Jarden's Track Record of Organic Performance Has Been Enhanced by Disciplined Acquisitions

Source: Jarden Corp. Investor Presentation, March 2014

1 Acquisitions shown reflect transactions that contributed more than 10% of revenue at the time of the acquisition.

2 Performance reflects total stock appreciation from Jarden’s inception, defined as market close 9/21/2001 as Martin E. Franklin and Ian G.H. Ashken were officially appointed as senior management on 9/24/01, through 12/31/2013.

By recycling cash into organic opportunities and disciplined acquisitions, Jarden has grown its three main divisions – Outdoor Solutions, Branded Consumables, and Consumer Solutions – which comprise 95% of the company’s net sales or over $7B in revenue. Each division has multiple market leading brands within its respective product categories. Jarden has leveraged its network of retail relationships and broad geographic presence to consistently grow these businesses over the long run, producing organic growth in-line with its 3%-5% target and far exceeding that level including acquisitions. Outdoor Solutions, the largest division by sales, is the world’s largest sports equipment company with familiar brands such as Rawlings (baseball gloves and balls), Coleman (outdoor equipment), Shakespeare (fishing), and K2 (skiing). The Branded Consumables division holds the largest market share across many diverse categories with brand names like Diamond (plastic cutlery, matches, toothpicks), Ball (preserving), Bee and Bicycle (playing cards), Yankee Candle (premium scented candles), and First Alert (smoke and CO alarms). The Consumer Solutions portfolio contains everyday home appliance brands with leading market shares like Sunbeam, Oster, CrockPot, Mr. Coffee, and FoodSaver. These businesses all benefit from being part of the larger Jarden platform.

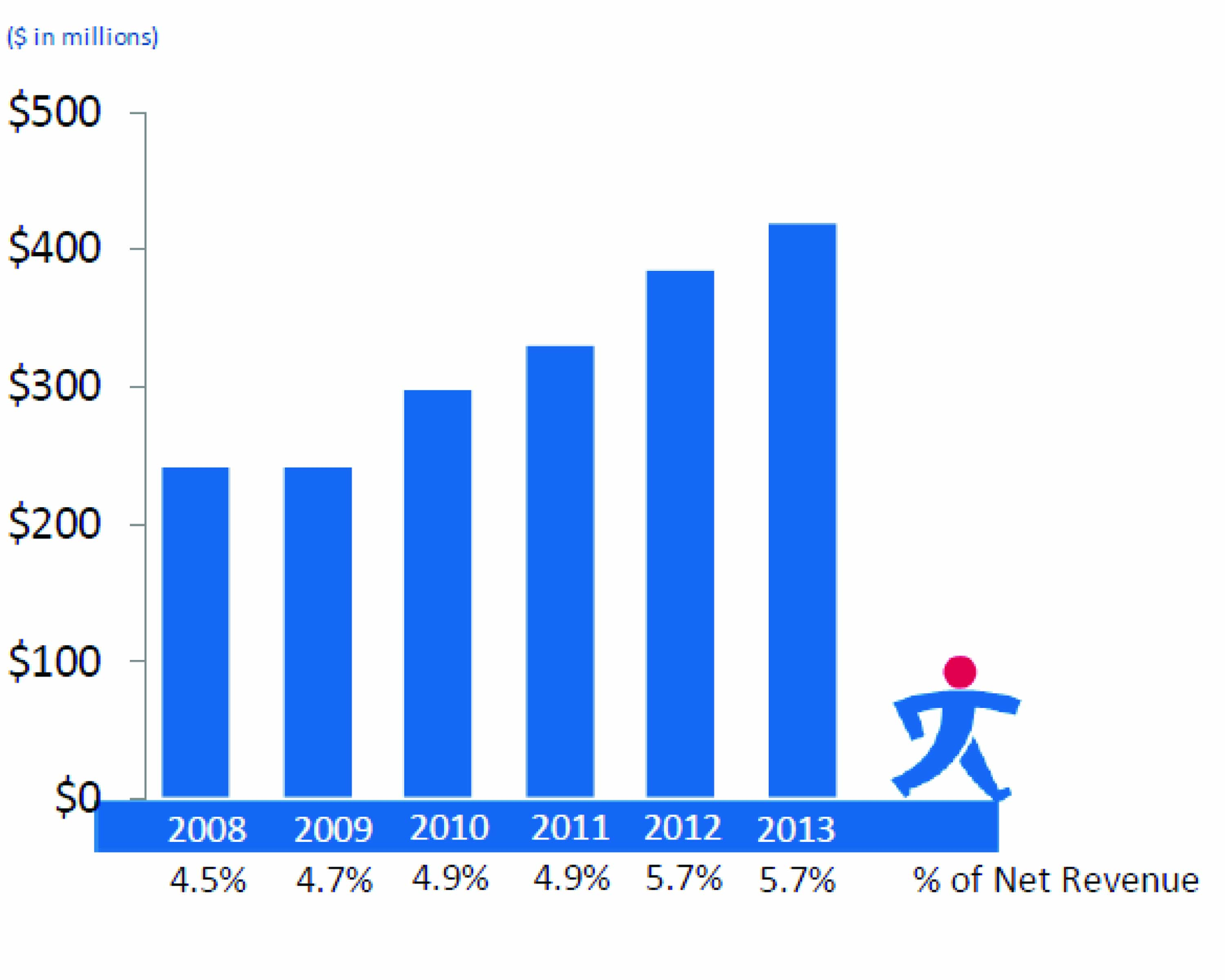

Strong alignment of management’s incentives with shareholders’ interests supports optimal, long-term capital allocation decisions. Jarden’s management, for example, has always maintained a high ownership stake in the company with the top three management team members collectively owning 6%, as of the last public disclosure. Further, each senior management team member has a substantial portion of compensation in restricted shares with a vesting hurdle tied to achieving Jarden’s five-year objective. This ownership mentality is demonstrated by management’s willingness to sacrifice short-term profitability by aggressively increasing investment in the company’s brands and product innovation, which we believe should lead to sustained and above average returns on invested capital (See chart below). One great example of how high insider ownership and well-structured incentives promote good stewardship of capital is Jarden’s suspension of the dividend in January 2012 in favor of a ‘modified Dutch tender’, repurchasing 13.2% of the company at roughly 10x trailing earnings. Jarden’s share price has since more than doubled.

Jarden has Supported Organic Growth through Significant Brand Equity Investment

Source: Jarden Corp. Investor Presentation, March 2014

Note: Excludes Yankee Candle pre 2013. Figures above include marketing and R&D expenses.

Undoubtedly, Jarden’s management has an excellent track record and has delivered on its growth and return objectives. They have also provided clear guidance and visibility for investors, executing plans to double earnings twice in the last ten years. In a recent investor presentation, management highlighted its goal of increasing earnings per share another 70% over the ensuing five years. In our opinion, the combination of an ownership mentality, long-term perspective, and disciplined capital allocation – along with Jarden’s portfolio of strong brands – should continue to reward investors over the long-term.

The views expressed are those of the research analyst as of May 2014, are subject to change, and may differ from the views of other research analysts, portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. DIAMOND HILL® is a registered trademark of Diamond Hill Investment Group, Inc.

© 2014 Diamond Hill Capital Management, Inc. All Rights Reserved.

© Diamond Hill Capital Management