With little escalation on the geopolitical front and no compelling data to shift broader economic expectations, interest rate markets were confined to narrow yield ranges in a rather tedious week. With intermediate and long dated Treasury rates failing to extend price gains from the prior week’s payrolls report, we suspect the path of least resistance this week for yields may be a gradual back up. By no means do we expect a material change in direction, but view the recent rally in interest rates to the low end of the yield range to stall, absent new critical insights from the Federal Reserve or escalation in Ukraine.

With stocks failing to repeat (so far) the outsized performance of 2013, bond market performance continues to defy expectations, handily outperforming equities. Investor demand, as measured by mutual fund flows, remains decisively towards fixed income. Continuing to deliver stable positive returns in contrast to equities, all fixed income sectors registered sizeable fund flows last week—the highest such level in aggregate since January.

The return of meaningful economic data returns this week, highlighted by Retail Sales tomorrow and followed by PPI and CPI on Wednesday and Thursday. Though all three will be closely watched by market participants and are expected to show gains relative to April, we don’t see any risk in the data that would bring forward a change in interest rate policy.

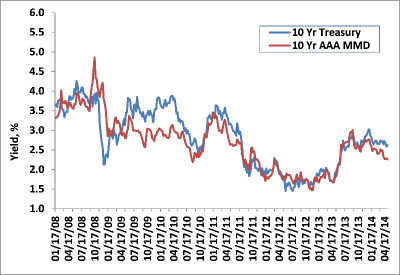

Weekly Change: 10Y Treasury Yields vs. 10Y AAA MMD

Source: Bloomberg, Thomson Reuters and Castleton Partners

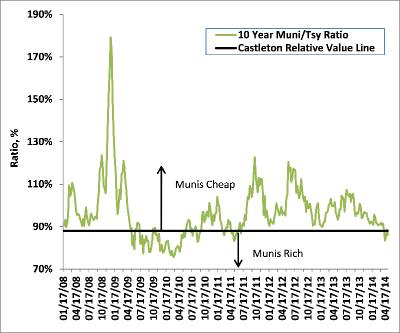

Ratio of 10Y Municipal Yield to 10Y Treasury Yield

Source: Bloomberg, Thomson Reuters and Castleton Partners

Tax-Exempt

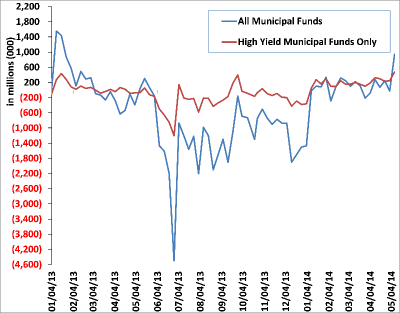

Following a 2014 theme of limited supply and increased demand, tax exempt prices were able to grind higher in a relatively lackluster week, outperforming taxable markets. Reversing the prior week’s mildly negative number, mutual fund flows jumped to +$943 million—the largest weekly inflow since January 2013. With yields at levels last seen in June 2013, fund flows remain heavily weighted to longer maturity and high yield funds, as investors seek additional income.

With new supply at only $4 billion last week, the issuance of new bonds so far in 2014 is 30% less than a year ago, which is a pace that would represent the lowest annual issuance since 2002. Despite improving balance sheets from the recovery of tax revenues and expense constraints, states remain reluctant to issue debt. With refunding volume as a percentage of new supply dropping, the ‘austerity’ mindset of the recent recession remains very much in vogue among state capitals. Thirty six gubernatorial elections are slated for this fall, and we suspect that the reluctance of incumbents to reflate balance sheets will remain the theme for the next six months. Traditional annual top issuers, California and New York have reduced supply by 21% and 45% respectively so far in 2014. Further supporting tax exempt prices in the near term: June, July, and August are shaping up to be one of the largest three month periods for coupon income, maturing bonds, and bond calls in recent years—only adding to increased demand.

Supply this week is expected to be $5 billion, led by the New Jersey Turnpike Authority (A3/A+/A) in the first billion dollar tax exempt loan since March. For high yield investors, a $450 million loan for Dulles (VA) Toll Road will highlight the calendar, as well. Rated Baa1/BBB+, the Dulles Toll Road is an eight lane tolled highway—approximately 13 miles in length—that is part of the Metropolitan Washington Airport Authority. With a thirty year operating history, we expect this loan to be well received.

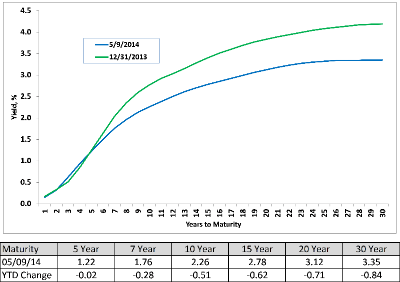

AAA Municipal Market Data (MMD) Yield Curve

Source: Thomson Reuters

Weekly Municipal Mutual Fund Flow Data

Source: Lipper AMG Data

Taxable

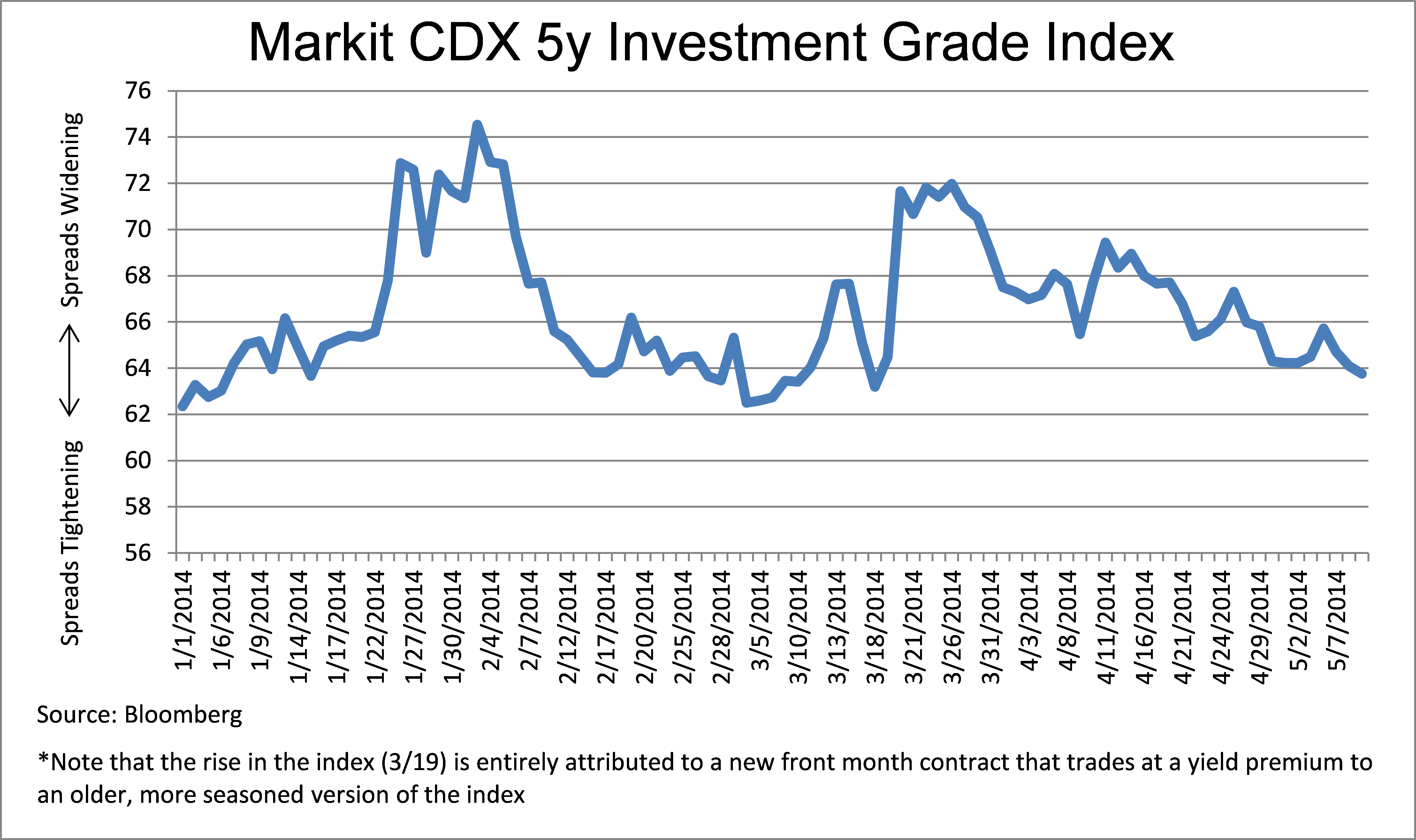

Investment grade corporate bond spreads were little changed last week, continuing their recent theme of low spreads and low yields. With only $21 billion of debt supply last week, issuers continue to take advantage of low long term yields by issuing long term debt at the expense of shorted dated issuance. Caterpillar Inc. (A2/A) priced a new $500 million 50 year loan at 4.76%, +137.5 over thirty year US Treasuries. Other notable offerings last week: a $2 billion ten year note from JP Morgan (A3/A) at +110 over the ten year Treasury, and a $350 million loan from Waste Management (Baa3/A-) at +92 to ten year Treasuries.

Charts of the Week

Volatility, as measured via the MOVE Index (Treasuries) at left and the VIX Index (equities) below, remains nonexistent in financial markets.

(Source: Bloomberg)

© 2014 Castleton Partners, LLC. All rights reserved.

THE FOLLOWING NOTES AND DISCLOSURES ARE AN INTEGRAL PART OF THIS REPORT: Past performance is not a guarantee of future results. Different investments involve varying degrees of risk, including the risk of illiquidity and the risk that you could lose part or all of your investment. There can be no assurance that the future performance of any specific investment, investment strategy, or product (including those discussed herein or recommended or undertaken by Castleton Partners, LLC) will be profitable, equal any corresponding indicated historical performance, be suitable for your portfolio or individual situation, or prove successful. Charts, graphs and indices are included herein only for reference and do not constitute forecasts of the past or predicted future performance of any investment. Indices are not investments. Due to changing market conditions and other factors the content herein may no longer reflect Castleton Partners, LLC’s current opinions or positions. Nothing discussed herein is or is intended as tax, legal, accounting or personalized investment advice from Castleton Partners, LLC. Should you have any questions regarding the applicability of any specific issue discussed herein we encourage you to consult competent advisers of your choosing. Nothing herein is or is intended as an offer to sell or a solicitation of offers to buy any security. Castleton Partners, LLC’s current written disclosure statement including discussion of our advisory services and fees is available upon request.