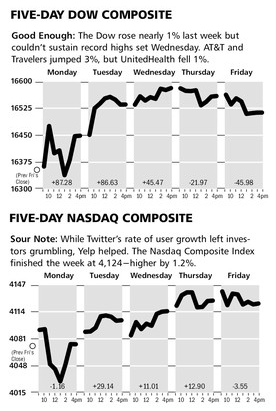

Another stable week for stock prices as deal making, solid earnings and dividend growth offset the conflicting signals on the economy as well as the uncertainties stemming from various global hot spots.

As the charts above illustrate, both the Dow Jones Industrial Average as well as the NASDAQ Composite moved higher by about 1% last week, but both remain slightly underwater so far in 2014.

The Markets & Economy

Last Monday, I warned to brace yourself for a lousy 1st quarter GDP report, but I was not prepared for the truly lousy report that was released. The estimated first quarter growth rate came in at just one-tenth of ONE percent. The only reason it was positive at all was because of the additional health-care spending going on in conjunction with Obamacare. Accordingly, the actual economy is flat lining, and while many want you to believe it is the weather they are just whistling past the graveyard.

Exports have rolled over and the consumer is getting hit with higher gasoline bills as well as healthcare expenses. Thus the two critical industries of housing and autos are not leading the economy any longer as the money is not there. All of this happy talk about a catch up in the remaining months of 2014 will soon be replaced with concern that the economy is running out of steam. Let me tell you something - there is no steam and hasn’t been for years. Zero percent interest rates and trillion dollar deficits have created zero momentum. The reason is because of the never-ending assault in this and other countries towards those who create wealth. In short, the incentive machine in America for taking risk (which means hiring) has simply been suppressed.

As a result, corporations are fixated on financial engineering due to government policy concerning taxes, energy and regulation of all kinds. We are very lucky that America is experiencing a renaissance in the energy arena. This, though, was done by the private sector and in spite of government policies concerning such issues as off-shore drilling or the much ballyhooed pipeline decisions being delayed hurting jobs and energy independence.

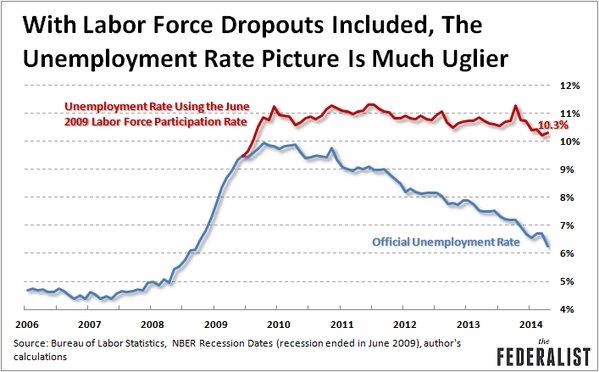

The news is not terrible though. The employment report last Friday showed the unemployment rate falling to 6.3%. This despite over 800,000 people falling out of the labor force. As the following chart shows, the falling participation rate is artificially depressing the unemployment rate. These people still exist and need to live, but are not counted by the government bureaucrats as being. The chart below shows a double digit unemployment rate if the participation rate was the same today as it was when the recovery began some 5 years ago.

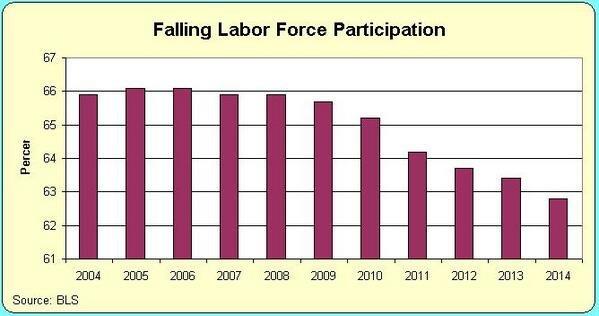

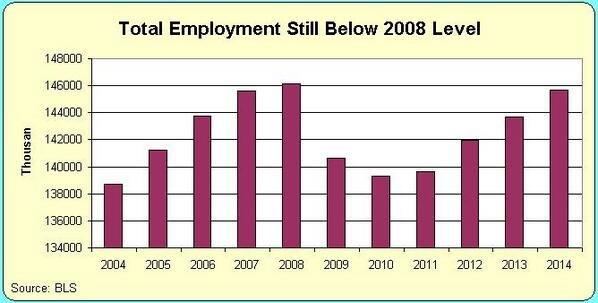

This is more easily understood by looking at the following two graphs. The first shows the falling participation rate mentioned above. The second shows that the number of jobs in America today is still below the number reached in 2008. Given population growth and the trend for people to work later into life puts the lie to the notion that the economy is gathering momentum. It has been stuck in the mud and remains so today.

What to Expect This Week

Much more debate about the global economy. The problem though is that the media thinks the recent weakness was all weather. The problem is that information for April is not showing a pick up. Even in Europe this morning the ECB lowered their growth expectation for the year, and once again expressed worries about deflation. China is floundering and Latin America is depressed. If the economy was doing better you could feel it. You wouldn’t have to have an economist explain it to you in some arcane manner.

The bond market agrees with me by the way. This morning the ten year Treasury note yielded below 2.60. Its yield has fallen all this year even with the removal of the “taper”. Quite simply the market is saying no-growth spurt in sight, and I will take that opinion over the White House guidance any day.

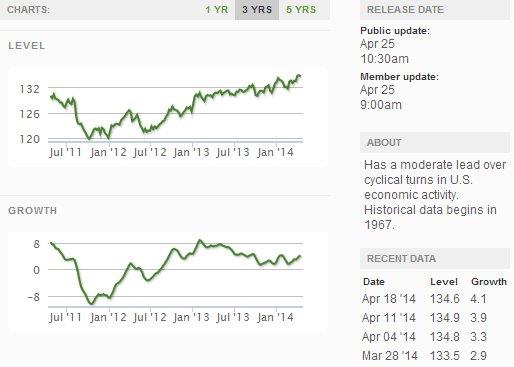

Finally, the weekly look at the Economic Cycle Research Institute’s weekly leading index of economic indicators shows a pull back within a trend which implies nothing is about to change.

When all is said and done, the year 2014 will see growth of around 2%, and that will be a victory under the current set of policy choices.

Shares of AKAMAI TECHNOLOGIES moved smartly higher last week after posting better than expected Q1 earnings. The Company reported EPS of .58 cents per share, solidly beating analysts’ projections. Profits rose 14% during the first 3 months of the year on revenue growth of 23% versus the previous quarter. Areas of strength for the Company were numerous: e-commerce, cybersecurity, IT outsourcing and content delivery, which continue to create demand for its network and web performance solutions.

CEO F. Thomson Leighton said “Our overachievement on the bottom line for the quarter came from better than expected traffic for our media delivery solutions”. AKAM has raised earnings and profit guidance for the second quarter.

SOUTHWESTERN ENERGY reported a record-setting first quarter thanks to a significant increase in production along with higher natural gas prices. SWN reported adjusted earnings of .66 cents per share, far exceeding last year’s Q1 earnings of .42 cents. Revenues also beat analysts’ predictions.

The Company’s average realized gas price, including hedges, rose 22.5% to $4.19 per thousand cubic feet, from $3.42 in the year-ago period. CEO Steve Mueller said quarterly records were set for production, adjusted earnings, cash flow and EBITDA. With natural gas prices expected to trade in the $4 - $5 range for the foreseeable future, Mueller says SWN is strategically well positioned to set even more production records for the upcoming quarter and the rest of 2014.

Shares of PIONEER ENERGY SERVICES also rallied on its earnings report last week. Net income was $2.6 million, $.04 cents per share, compared to the $1.3 million, or $0.02 cents per share reported during Q1 of 2013. Increased demand for PDC’s production services segment helped the Company earn $239 million, up 4% from revenues reported the previous year.

Revenues for PDC’s drilling services segment was slightly lower than the prior quarter, due to decreased utilization of certain operations in Columbia. The Company reduced interest expense going forward with the successful refinancing of some Senior debt. On the heels of PDC’s report several Wall Street analysts raised price targets for PIONEER to the $17-$18 range.

(c) McIntyre, Freedman & Flynn