US Treasury yields declined across the entire maturity spectrum last week, as renewed geopolitical risk more than outweighed a strong employment report. With inflation remaining well below the Fed’s target rate of 2%, long dated Treasury yields continued to decline at a faster rate than shorter dated yields, further flattening the yield curve. At 295 basis points, the yield differential between two year notes and thirty year bonds now rests at its flattest point since last June. Despite a GDP report last week showing that Q1 growth was a negligible +0.1%, we view the report as heavily influenced by extreme weather. Absent extreme escalation in Ukraine, we believe the pronounced yield curve flattening trend is tiring, as the Fed winds down their monthly purchases of long dated Treasuries and mortgage backed securities. Additionally, the Treasury department announced last week a reduction of $8 billion per month in two and three year note issuance, a result of higher tax receipts reducing the federal deficit.

Noting that we still have an uphill battle to sustained economic recovery, the Federal Reserve delivered few surprises at the conclusion of their two day meeting last week. As expected, the Fed kept their recently revised forward guidance unchanged, likely meaning that short term interest rate policy will remain near zero for the balance of 2014—and likely well into 2015. With only second tier economic data to wrestle with this week, markets will most likely key on Wednesday’s testimony by Federal Reserve Chair Janet Yellen to the Joint Economic Committee of Congress on monetary policy and the outlook for the US economy.

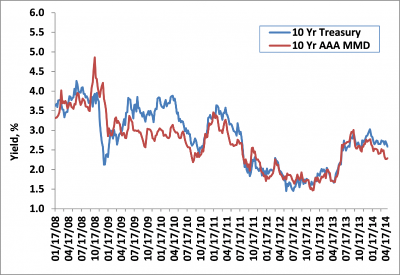

Weekly Change: 10Y Treasury Yields vs. 10Y AAA MMD

Source: Bloomberg, Thomson Reuters and Castleton Partners

Ratio of 10Y Muni Yield to 10Y Treasury Yield

Source: Bloomberg, Thomson Reuters and Castleton Partners

Tax-Exempt

Tax exempts ended the week in mixed fashion, as five and ten year benchmark yields increased 6 and 1 basis point to 1.26% and 2.29% respectively, while long end yields decreased by one basis point to 3.44%. Failing to match the rally in Treasury rates, the ratio of municipal yields relative to taxable yields—a key metric of relative value for non-traditional tax exempt investors—cheapened last week, with the five year ratio jumping the most: nearly seven percentage points, to 76%. The five year Muni/ Treasury ratio now sits 5 points above its 2014 average, while the ten year (89%) and thirty year (103%) are close to their 2014 averages. With tax exempt supply running 32% below 2013’s level, and combined with a resurgence in demand, we expect ratios to grind lower during the balance of 2014—further extending the year to date outperformance of municipals over taxable debt. According to the Bond Buyer, municipal issuance is trending at its lowest pace since 2002 ($288 billion).

One area of the tax exempt market that showed notable improvement last week was debt issued by the Commonwealth of Puerto Rico. For the first time in nearly two decades, Governor Padilla has proposed a balanced budget for FY2015. Pledging that the island’s debt was “sacrosanct”, the budget relies mostly on spending cuts and calls for no deficit financing. Rated Ba2/BB+, island debt rallied 2 to 3 points on the week. The record-setting $3.5b high yield P.R. general obligation loan, issued last March, continues to trade at its issuance price of $93. With fund flows of over $244 million last week, tax exempt high yield debt continues to outperform with returns of nearly +7.5%, as measured by the Barclays High Yield Municipal Bond Index.

The first full week of May brings one of the lightest non-holiday new issue supply weeks of the year, with less than $4 billion expected to price. The largest loan is a $450 million deal for Illinois Tollway Authority (Aa3/AA-).

AAA Municipal Market Data (MMD) Yield Curve

Source: Thomson Reuters

Weekly Municipal Mutual Fund Flow Data

Source: Lipper AMG Data

Taxable

In a very active week, corporate bond spreads maintained their recent tights in credit spreads, with most sectors tightening, on average, an additional basis point relative to Treasuries. Nearly 30 billion of new debt was priced, highlighted by Apple Inc.’s $12 billion multi tranche loan. Somewhat surprising though, were investment grade mutual funds, which experienced their first redemption (-$74 million) of 2014—the first such instance for any week since October 2013. Despite those redemptions, the Apple loan was easily absorbed by the market—reportedly receiving nearly $40 billion in orders in what was the sixth biggest USD high grade transaction on record. The largest tranche in Apple’s loan was a $2.5b term due in 10 years, priced at a spread of +77bp over comparable maturity US Treasuries, to yield 3.45%.

Though not investment grade, also gathering investor attention last week was the long- awaited bankruptcy filing of Energy Future Holdings Corp of Texas. Formerly known as TXU Corp, and taken private in 2007 in the largest leveraged buyout in US history, Energy Future’s filing is the 7th largest bankruptcy ever, as it looks to extricate itself from its massive debt load. Not surprisingly, high yield mutual funds reacted in kind last week, with $631 million in outflows.

Despite the narrowing of credit spreads of late (and the potential for further narrowing), we reiterate our caution on corporate bonds, sensing that the risk-reward tradeoff is not sufficiently attractive. Merger and acquisition (M&A) activity has surged of late, with April being the second most active month since last September, following the Lehman crisis. With frustratingly slow macro-economic growth, we remain concerned that M&A activity will increase, as corporations take advantage of receptive funding markets and high cash balances to leverage their balance sheets and generate increased growth.

© 2014 Castleton Partners, LLC. All rights reserved.

THE FOLLOWING NOTES AND DISCLOSURES ARE AN INTEGRAL PART OF THIS REPORT: Past performance is not a guarantee of future results. Different investments involve varying degrees of risk, including the risk of illiquidity and the risk that you could lose part or all of your investment. There can be no assurance that the future performance of any specific investment, investment strategy, or product (including those discussed herein or recommended or undertaken by Castleton Partners, LLC) will be profitable, equal any corresponding indicated historical performance, be suitable for your portfolio or individual situation, or prove successful. Charts, graphs and indices are included herein only for reference and do not constitute forecasts of the past or predicted future performance of any investment. Indices are not investments. Due to changing market conditions and other factors the content herein may no longer reflect Castleton Partners, LLC’s current opinions or positions. Nothing discussed herein is or is intended as tax, legal, accounting or personalized investment advice from Castleton Partners, LLC. Should you have any questions regarding the applicability of any specific issue discussed herein we encourage you to consult competent advisers of your choosing. Nothing herein is or is intended as an offer to sell or a solicitation of offers to buy any security. Castleton Partners, LLC’s current written disclosure statement including discussion of our advisory services and fees is available upon request.