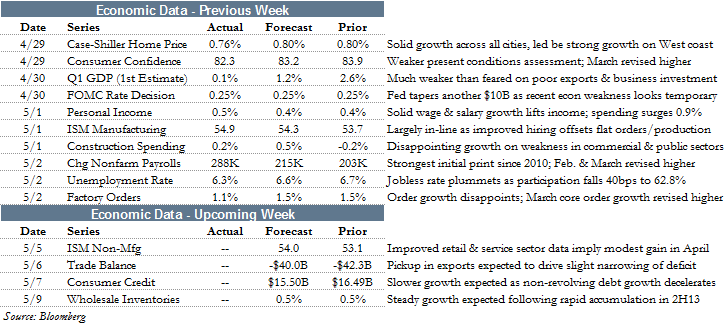

STOCKS DIGEST BIG WEEK OF DATA

Stock markets ticked up last week after digesting a number of economic surveys and indicators. The S&P 500 and Russell 3000 both gained roughly 1.0% on the week.

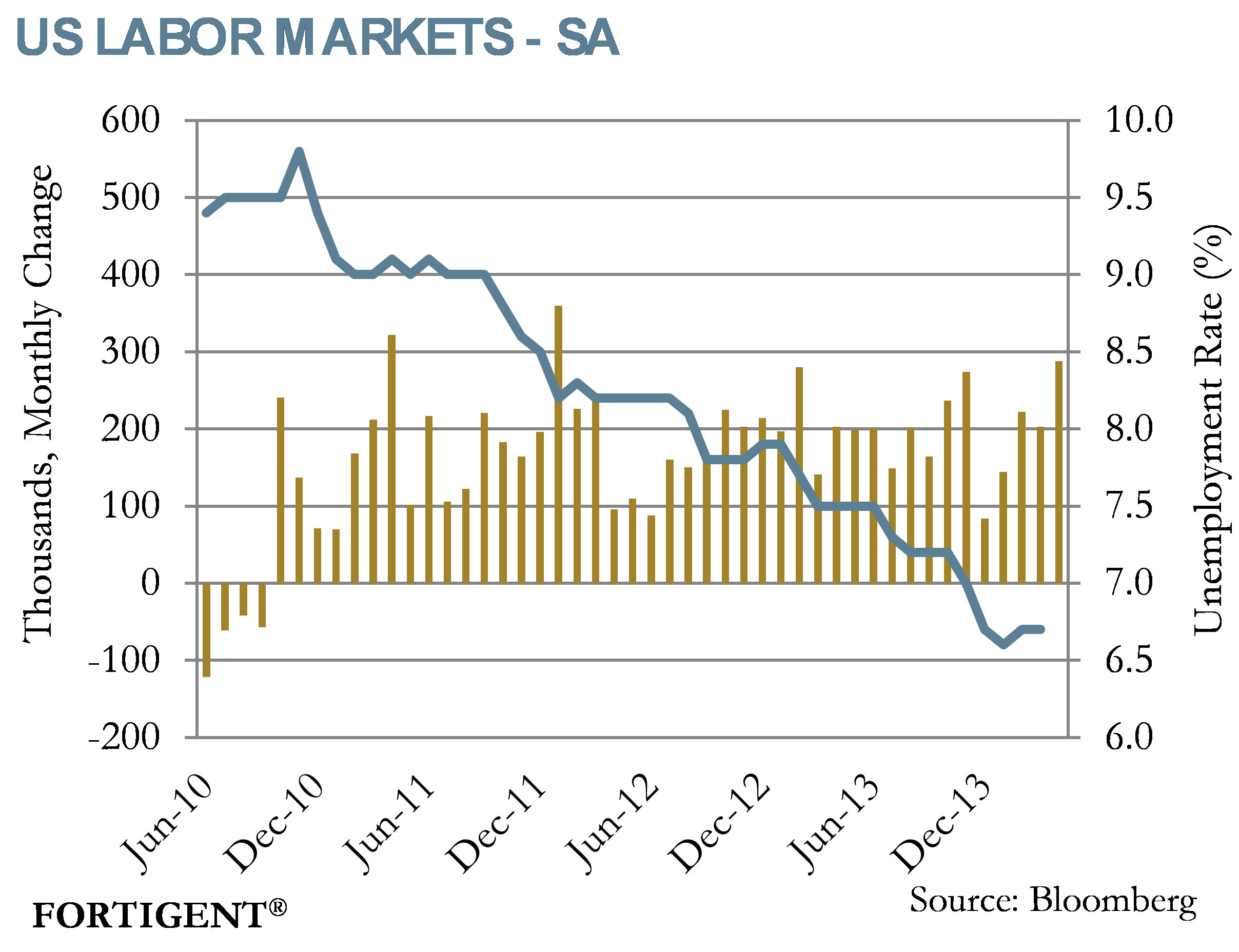

At the forefront of data was April employment and Q1 GDP growth figures. The monthly jobs report showed that unemployment had dropped dramatically. U.S. April non-farm payrolls rose 288,000 resulting in a fall in the unemployment rate from 6.7% to 6.3%. Debate surrounding the overall health of the labor market still remains as labor market participation continues to fall.

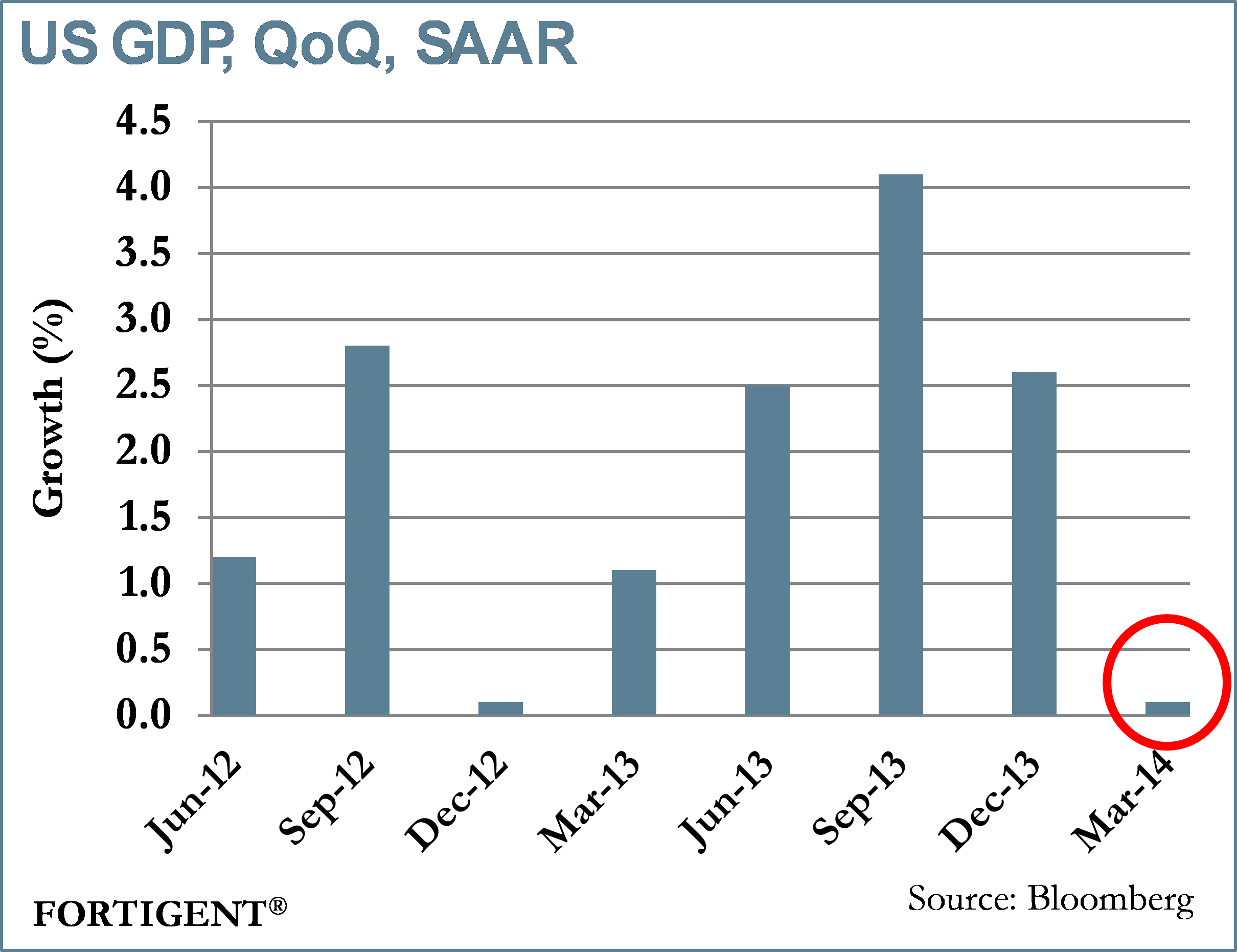

First quarter GDP showed the U.S. economy grew, but at very slow rate as the harsh winter weather was to blame. First quarter real GDP growth came in at 0.1%. This is significantly lower than fourth quarter 2013, which showed real U.S. GDP growth of 2.6%.

Economists were forecasting growth at around 1.1%. Most of the weakness came from a decline in trade and inventories, which are both expected to rebound in the second quarter.

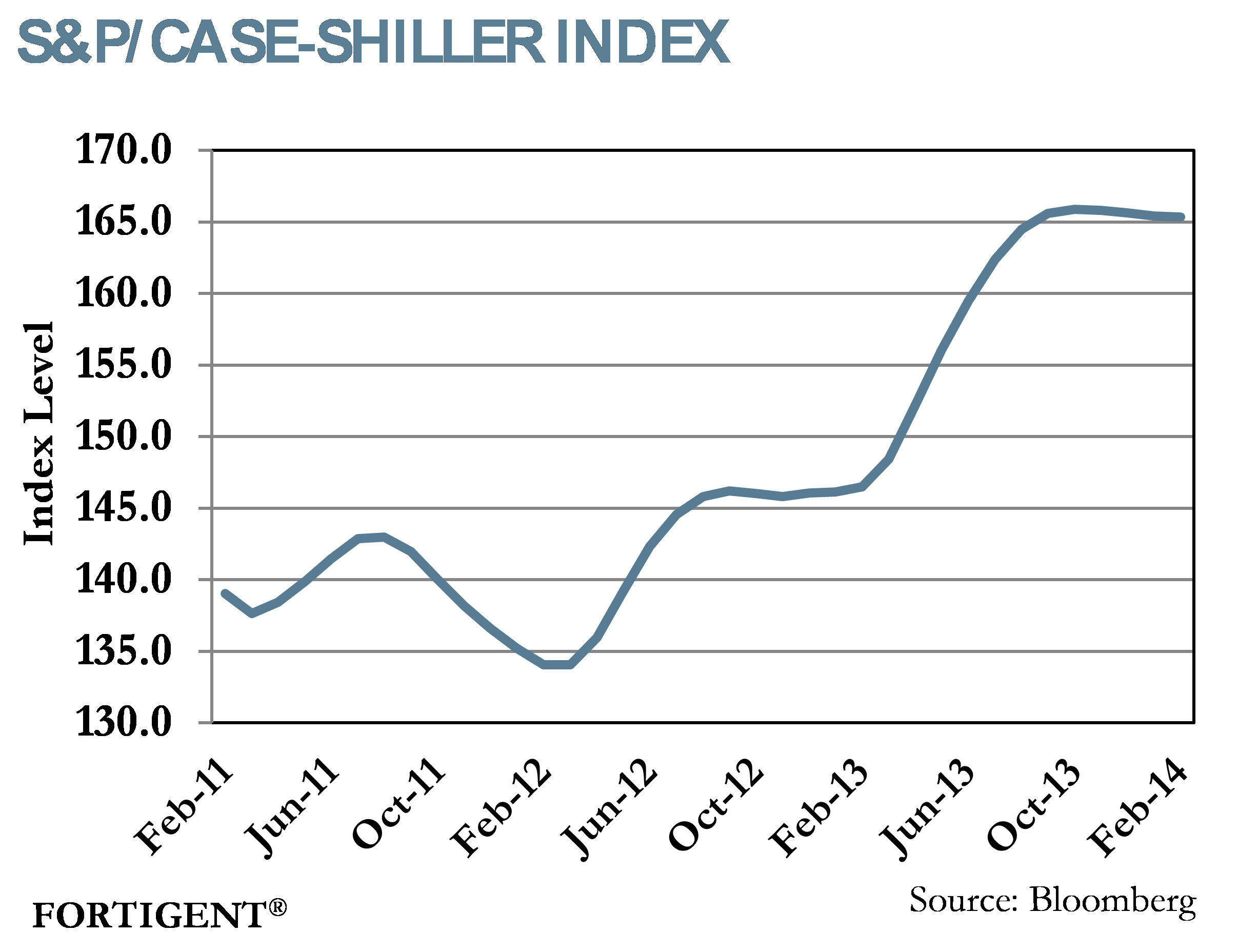

The S&P/Case-Shiller Home Price index showed signs of slowing within the housing sector as home price appreciation seems to be losing momentum. However, it remains to be determined how much impact the winter weather had on recent price slowdown. The 20-city index rose by 0.8%, up from 0.7% the prior month. Home prices continue to rise, but at a slowing rate. The index increased 12.9% year-over-year from February 2013. This is down from a 13.2% year-over-year increase in January.

Of the 20 cities the index covers, 13 cities posted lower annual rates of growth while only five cities experienced price appreciation. Home price gains were widely distributed throughout the U.S. with the majority of home price gains coming from the West coast.

On the manufacturing front, the ISM Manufacturing index showed signs of the manufacturing sector emerging from the harsh winter weather. The index increased to 54.9 from 53.7 in March, exceeding consensus forecasts of 54.4. The index moved higher as 17 of the 18 industries the ISM report tracks grew in April. The index is still below its 12-month peak of 57, hit in November 2013.

On the consumer side, the Consumer Confidence index dipped in April coming in at 82.3 as consumers became concerned over hiring and business conditions. Despite coming in lower than the March reading of 83.9, consumer sentiment continues to march higher. The Consumer Sentiment index came in at 84.1 in April. This is a considerable jump from its March reading of 80.

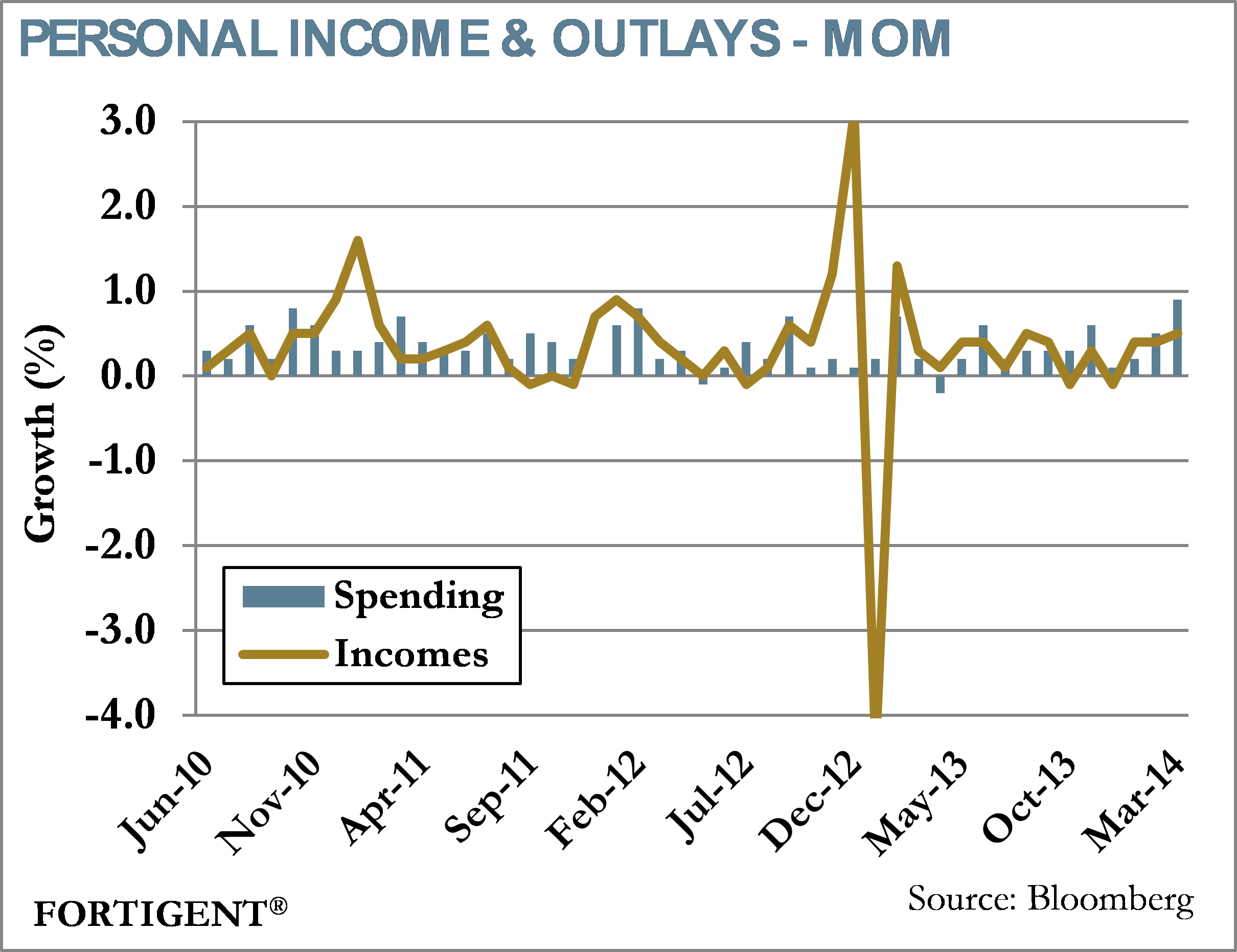

U.S. personal income and spending came in positive as both rose more than expected in the month of March. Personal income increased 0.5% following an upwardly revised 0.4% in February. Personal spending followed suit as the index jumped 0.9% following an upwardly revised 0.5% rise in February. Personal income and spending were expected to rise 0.4% and 0.6%, respectively. The increase in personal spending is particularly positive for the U.S. economy as it makes up approximately two-thirds of economic activity.

LABOR MARKETS BOUNCE BACK FROM WINTER HIBERNATION

In a less than surprising development, U.S. non-farm payrolls grew by 288,000 in April. While some are loathe admitting the positive nature of April’s report, there was plenty to be happy about in the latest release, suggesting the economy continues to move towards a more favorable footing. As always in the post-2008 world, caveats remain and the trend in the months ahead will provide a clearer picture into the pace of recovery.

Refreshing the data, nonfarm payrolls expanded 288,000 in April and the unemployment rate declined sharply from 6.7% to 6.3%. Initial data on February and March was also revised higher by a combined 36,000.

Job gains were broadly dispersed, but the service sector was the clear winner, adding 220,000 jobs in April. At the industry level, job growth was relatively strong in professional and business services, temporary help, retail trade, restaurants, construction, healthcare, and mining.

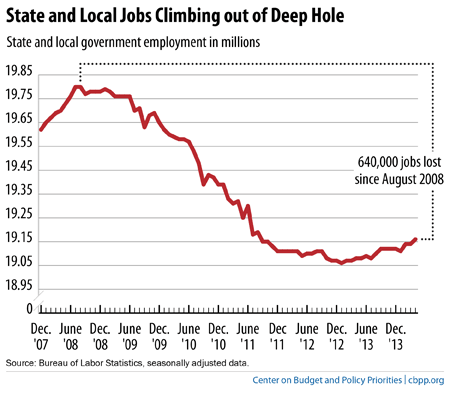

After several years of aggressively cutting jobs, state and local governments are experiencing something of a renaissance since the start of 2014. In April, there were 18,000 jobs added by state and local governments, bringing the 2014 total to 43,000. It is encouraging to see governments turning the corner and acting as a tailwind to the economy, but there have still been 640,000 jobs lost since August 2008.

Source: Center on Budget and Policy Priorities

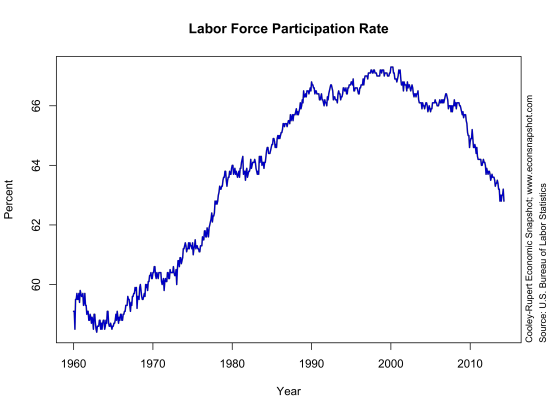

As noted previously, the unemployment rate dropped rather substantially in April, returning to September 2008 levels. But, the household survey, which drives the unemployment figure, revealed that the number of workers declined 73,000, and the overall labor force shed an outsized 806,000 individuals.

The labor force continues to suffer from people unable to find employment and simply choosing to no longer search for a job. Goldman Sachs (GS) believes that more people are starting retirement earlier or electing to go back to school due to a lack of quality jobs. In its opinion, GS thinks that slack in the labor market makes it difficult for the Fed to raise interest rates, and it could be some time before the participation rate begins to reverse.

Source: U.S. Economic Snapshot

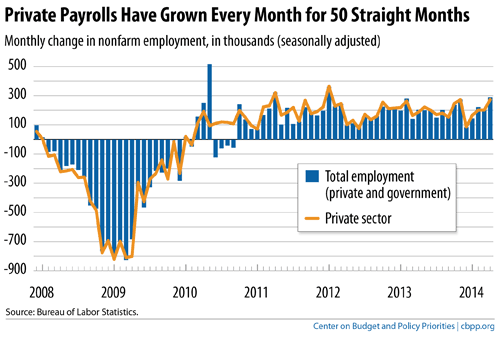

Weakness in numbers such as the participation rate makes it easy to discount the overall recovery, but it is difficult to ignore that private payrolls have now grown for 50 consecutive months. Labor markets remain in a tenuous position, consistently showing signs of strength and weakness. Until there is near certainty, the Federal Reserve will be hard pressed to move aggressively and risk setting the economy back. The period of easy monetary conditions will continue for the foreseeable future, to the expected benefit of equity investors.

Source: Center on Budget and Policy Priorities

THE WEEK AHEAD

Looking forward to the week ahead, markets will be attuned to ISM Non-Manufacturing data, consumer credit, and wholesale inventories.

Investors will also be watching U.S. trade figures and Janet Yellen’s remarks in front of the Joint Economic Committee on Wednesday in order to gain further insight on the pace of the recovery.

On the policy front, central bank meetings in Australia, the Euro area, and UK will be the most closely followed.

ABOUT FORTIGENT

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value