Interest rate risk is one of most pressing topics being discussed among advisors, consultants and investors. As of March 2014, we have been through five and a half years of extraordinarily aggressive monetary policy and outright intervention in the capital markets by the U.S. Federal Reserve.

At long last it seems like the healing process is working, which means eventual inflation, and normalization of monetary policy and interest rates. The challenge for real estate securities investors is determining how the normalization process will affect prices and investment performance.

Key Considerations

How interest rate movements impact real estate securities is complex and difficult to predict. After studying the historical performance of these securities, our findings indicate that, despite common perceptions to the contrary:

· Not all interest rates move together

· Real estate securities have had surprisingly low correlations to interest rates

· More often than not, real estate securities have generated positive performance during periods of rising interest rates

In our opinion, these observations indicate that growth in earnings, cash flow and dividends clearly differentiate real estate equities from fixed-income investments that have more pronounced interest rate risk.

With respect to preferred stocks issued by real estate investment trusts (REITs), we believe credit quality, yield spreads and underlying fundamentals together play an equal or more important role in driving investment returns than interest rates alone.

Which interest rates are changing and why?

When discussing the impact of interest rates on real estate securities, one must consider which interest rates are moving and why.

When one speaks of “interest rates,” are they describing:

· Corporate bond yields moving in response to investor concerns about business credit?

· A spike in long-term government bond rates due to inflationary pressures?

· A rise in short-term rates causing an inverted yield curve?

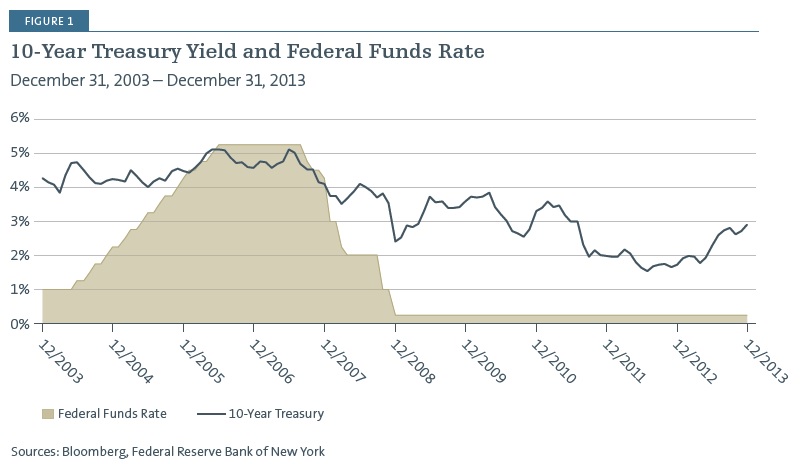

Not all interest rates move together. Short-term (overnight interbank lending) rates can fall or rise without a commensurate change in rates on long-term government bonds. In recent years, any causal relationship between the two rates appears tenuous at best (Figure 1).

How have real estate securities historically been impacted by increasing rates?

Real estate companies, such as REITs, issue common shares, preferred shares, corporate bonds and secured mortgages. Each has a different claim on the company’s cash flow and assets. Some have fixed payment streams while others participate in the earnings and dividend growth of the company. Each security type will react differently to changing economic conditions.

Why have real estate securities shown low correlation to interest rates and positive performance during periods of rising rates?

A linkage exists between interest rates and real estate fundamentals that mitigates the influence of interest rates on these securities. The dynamics that drive interest rates up— inflationary pressures from economic growth—tend to cause real estate fundamentals to improve, potentially offsetting some of the impact of rising rates through accelerated earnings, dividend growth and improved credit quality.

Macro Outlook

The near-term outlook for rates across the curve seems stable. Strong central bank support for robust liquidity is clear and makes intuitive sense given the gravity of our recent economic upheaval. We think inflationary concerns are presently well-balanced by disinflationary pressures (including high unemployment and even higher underemployment).

Longer term we see an increase in shorter-term rates being part of—and reflective of—a systemic recovery. This would also imply an improvement in credit quality.

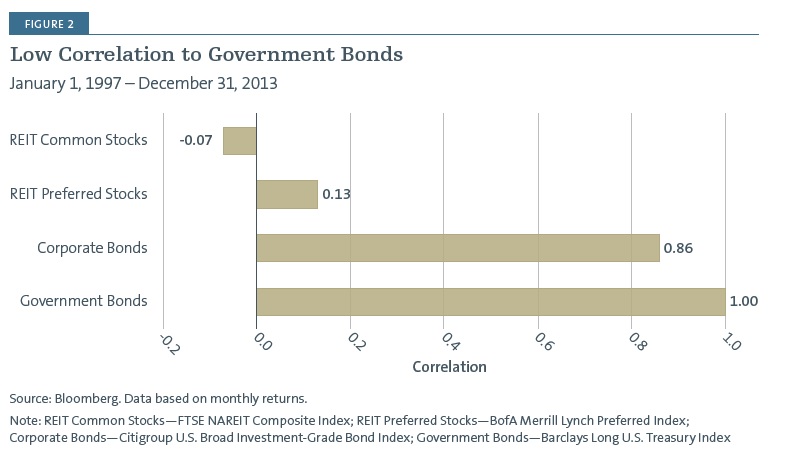

It is also worth noting that increases in shortterm rates do not necessarily mean increases in long-term rates as shown in our example (Figure 1). A rise in short-term rates might, in fact, be well received by longer-term bond investors as a preemptive inflation fighting measure. Notably, REIT common shares and REIT preferreds have both historically shown low correlations to interest rates (Figure 2).

Positive performance

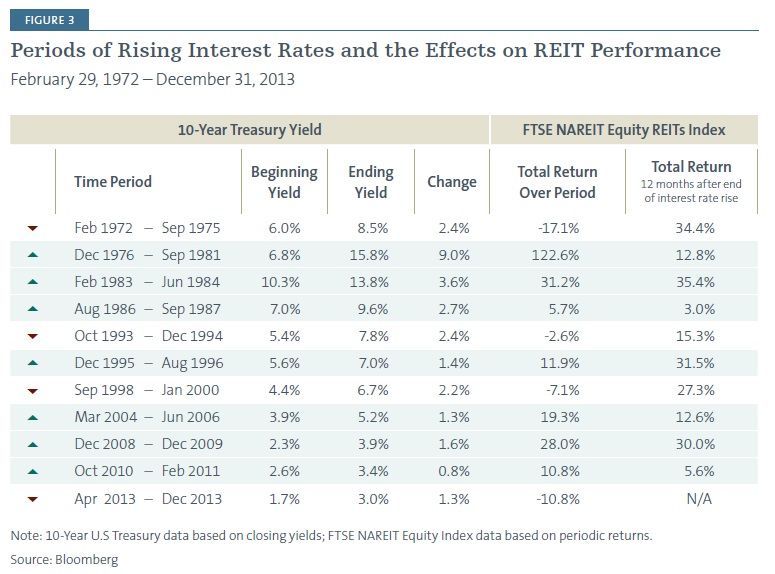

In general, declining rates are viewed as advantageous for stock prices while increasing rates are unfavorable; however, studies show that equity REIT performance does not necessarily follow this pattern. Since 1972, there have been eleven periods of rising long-term interest rates—seven were marked by positive performance in REIT common shares (Figure 3)

Investment Strategy

REIT preferred stocks

We think real estate preferred stocks represent a compelling value given their overall risk profile and their high current yields. We feel these securities offer potential price improvement as well as an attractive cash yield. We think a modest rise in long-term rates would likely be offset by improved credit quality and therefore remain quite constructive on the space for our income-focused accounts.

REIT common stocks

We believe REIT common stocks are very well positioned to perform in an environment where long-term rates may move up in a stable fashion. REITs generally do an excellent job of managing the maturity of their long-term liabilities and the breadth and diversity of their leases and underlying tenant credit provide for growing income and dividends to shareholders.

Conclusion

Investors have a wide range of real estate securities from which to choose. REITs may issue common stock, preferred stock and debt securities. Each company may invest in distinct property sectors or geographic regions and employ varying business strategies. Investors need to be skilled in identifying the best risk-adjusted returns among the available options at any point in the business cycle.

We believe the historical performance of real estate securities, in addition to credit quality and yield spreads, provides some comfort that these securities warrant a position in investor portfolios. The key for investors is to allocate for the right reasons—as a long-term investment designed to provide a combination of current yield and growth potential through changing business environments.

Definition of Terms

10-Year U.S. Treasury is a debt obligation issued by the U.S. Treasury that has a term of more than one year, but not more than 10 years.

Barclays Long U.S. Treasury Index measures the performance of public obligations of the U.S. Treasury that have a remaining maturity of 10 or more years.

BofA Merrill Lynch Preferred Index is a capitalization weighted index of preferred stock issues that is generally representative of the market for preferred securities.

Cash flow is a revenue or expense stream that changes a cash account over a given period.

Citigroup U.S. Broad Investment-Grade Bond Index is an unmanaged index generally representative of the performance of investment-grade corporate and U.S. government bonds.

Correlation is a statistical measure of how two securities move in relation to each other.

Credit quality informs investors of a bond or bond portfolio’s credit worthiness, or risk of default.

Federal funds rate is the interest rate at which a depository institution lends funds maintained at the Federal Reserve to another depository institution overnight.

FTSE NAREIT Composite Index is an unmanaged index consisting of approximately 200 real estate investment trust stocks.

FTSE NAREIT Equity REITs Index is representative of the tax-qualified REITs listed on the New York Stock Exchange, the American Stock Exchange and the NASDAQ National Market.

Interest rate risk is the risk that an investment's value will change due to a change in interest rates.

Liquidity is the degree to which an asset or security can be bought or sold in the market without affecting the asset’s price.

Preferred stock is a class of ownership in a corporation that has a higher claim on the assets and earnings than common stock.

Preferred stock generally has a dividend that must be paid out before dividends to common stockholders and the shares usually do not have voting rights.

Yield curve is a line that plots the interest rates, at a set point in time, of bonds having equal credit quality, but differing maturity dates.

Yield spread is the difference between yields on differing debt instruments, calculated by deducting the yield of one instrument from another.

One cannot invest directly in an index.

You should consider the investment objectives, risks, charges and expenses of the Forward Funds carefully before investing. A prospectus with this and other information may be obtained by calling (800) 999-6809 or by downloading one from www.forwardinvesting.com. It should be read carefully before investing.

RISKS

There are risks involved with investing, including loss of principal. Past performance does not guarantee future results, share prices will fluctuate and you may have a gain or loss when you redeem shares.

Debt securities are subject to interest rate risk. If interest rates increase, the value of debt securities generally declines. Debt securities with longer durations tend to be more sensitive to changes in interest rates and more volatile than securities with shorter durations.

Investing in the real estate industry or in real estate-related securities involves the risks associated with direct ownership of real estate which include, among other things, changes in economic conditions (e.g., interest rates), the macro real estate development market, government intervention (e.g., property taxes) or environmental disasters. These risks may also affect the value of equities that service the real estate sector.

The new direction of investing

The world has changed, leading investors to seek new strategies that better fit an evolving global climate. Forward’s investment solutions are built around the outcomes we believe investors need to be pursuing – non-correlated return, investment income, global exposure and diversification. With a propensity for unbounded thinking, we focus especially on developing innovative alternative strategies that may help investors build all-weather portfolios. An independent, privately held firm founded in 1998, Forward (Forward Management, LLC) is the advisor to the Forward Funds. As of December 31, 2013, we manage $5.2 billion in a diverse product set offered to individual investors, financial advisors and institutions.

Forward Funds are distributed by Forward Securities, LLC.

Not FDIC Insured. No Bank Guarantee. May Lose Value.

©2014 Forward Management, LLC. All rights reserved.