“There are a terrible lot of lies going about the world, and the worst of it is that half of them are true.”

- Winston Churchill

After the Financial Crisis and the resulting Dodd-Frank Act and Affordable Health Care Act, we knew there was no way we would go back to normal, whatever normal really was. Our world changed and we still continue to feel the uncomfortable mutations after the crisis. The management of Citigroup showed another disconnect with regulators as its 2014 capital plan was rejected. After several attempts to launch its healthcare website, the Obama administration announced that over 8 million people had signed up for health care insurance through the government exchange. This undoubtedly will go down as the worst software rollout since Microsoft Vista. Russia invaded Crimea as if the Cold War still exists and ignoring any established foreign relations. And, the National Labor Relations Board allowed players at Northwestern University to form a union. No longer are there student-athletes; now there are athlete-students.

Let’s put this into context: we survived the worst financial crisis of our time in 2008, yet we are experiencing meager economic activity. In fact, this is the weakest recovery at this point in the business cycle since World War II. Most everyone’s personal retirement account balances have returned to pre-crisis levels. Consumer spending, housing, and the employment picture have all improved. We can list more signs of recovery but you probably get the idea. However, we still have massive government involvement in our capital markets that directly manipulates the level of interest rates, which in turn impacts the valuations of publicly traded securities. In the largest democracy in the world, we do not have free markets. Still, the stock market posted phenomenal performance last year with the S&P 500 up over 32%. We believe this is not repeatable given the underlying economic reality and muted global demand. There appears to be a disconnect between underlying fundamentals of companies and valuations in the market.

In our opinion, there are two critical issues to be addressed to move our economy toward sustained growth – job creation and private credit expansion. And, they are pretty much the same two issues we have harped on for the past five years. On the job creation front, U.S. businesses finally added enough cumulative jobs over the past four years to replace the 8.8 million people who lost their jobs during the recession. However, the economy is nowhere near the performance that economists would typically expect following an ordinary recession. That said, this was no ordinary recession.

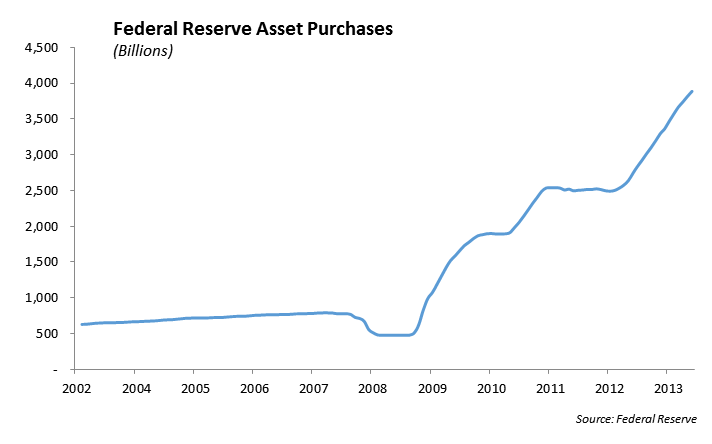

This past quarter, the markets weathered an important transition in leadership as Ben Bernanke retired and Janet Yellen assumed the role as the first Fed Chairwoman. Ben Bernanke did an outstanding job navigating the world’s largest economy through the biggest financial crisis since the Great Depression while carrying the dysfunction of Washington DC on his shoulders. Make no mistake, while the nuance of the Fed’s message may change slightly, the Fed wants to curtail its asset purchase program but will do whatever is necessary to insure that the economy continues to heal from the wounds of the Financial Crisis. For investors, this means easy money policies will remain in place for some time before the Fed will feel the need to tighten.

Structural problems in the economy resulting from the Financial Crisis, including the formation and implementation of the Dodd-Frank Act as well as the Healthcare Reform Act have impaired job creation, fixed investment, and private credit expansion. As a result, the economy continues to grow below its potential. We expect that, with the uncertainty surrounding much of this legislation behind us, more clarity will help businesses increase investment in property plant and equipment.

Gregory J. Hahn, CFA

Chief Investment Officer

The Economy

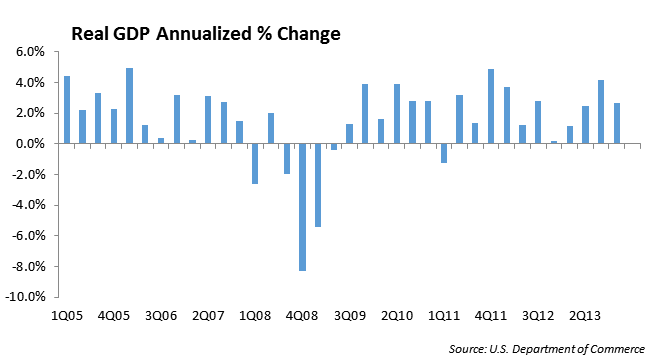

The U.S. economy grew by a revised 2.4% for the fourth quarter of last year. We expect muted growth to continue through the first quarter as harsh weather across the Midwest and Northeast impacted consumption and investment. However, with continued accommodative Federal Reserve policies, increased bank lending and a strong housing market, we expect economic growth to pick up through the year.

A continued recovery in the housing sector is important to economic growth because of its positive impact on consumer spending. For example, when people buy new homes, they spend more money at the hardware store buying things like paint, door knobs and patio furniture. This helps to fuels growth beyond just the new home purchase. Adding to this, we expect the banks to be more accommodative to support residential lending.

Business spending was a bright spot last year as companies invested more in equipment, software and infrastructure. Overall non-residential fixed investment grew by 7.3% in the fourth quarter. While we expect fixed investment to slow this quarter, we still see it as bright spot in 2014. The diminished fiscal drag from last years’ tax increase and government spending cuts, as well as the strong likelihood that investment in equipment will increase later this year will be additional catalysts for growth.

Largely as a result of the U.S government shutdown last October, federal spending and investment declined 12.8% in the fourth quarter. However, with a budget in place, the government should be a net contributor to growth through increased spending. Overall, while we expect GDP growth for 2014 could exceed 3.4%, this expansion is still noticeably slower over this business cycle than previous expansions.

Inflation

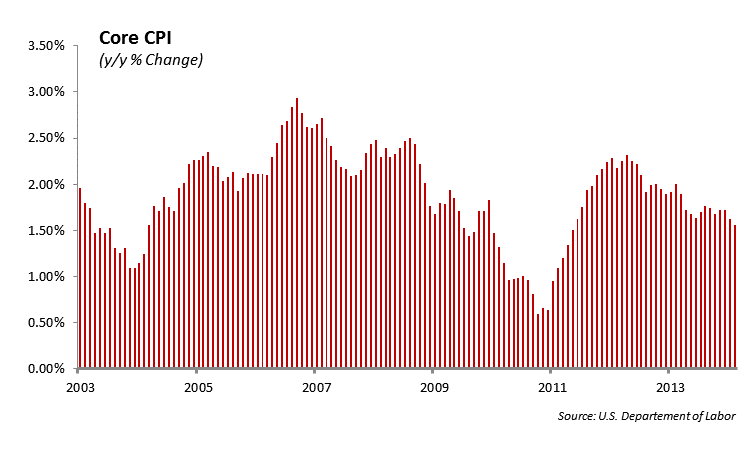

At this point in the recovery, we believe there is a higher risk of global deflation than there is of inflation. The lack of wage and job growth has contributed to suppress demand across the globe. The spiral of falling demand, excess capacity.

The Japanese central bank has been waging war on deflation for the past two decades and the European Central Bank recently articulated plans to address its growing concern with deflation in the Eurozone region. While the Fed has targeted inflation near 2.0%, the CPI has been trending closer to 1.8%.

However, this deflationary scenario could change quickly. The key factor that will affect the rate of inflation is how the Federal Reserve chooses to deal with the $2.6 trillion in excess reserves on deposit at the Federal Reserve Bank. As we’ve written before, if the Fed pushes the banks to move their excess reserves off of the central bank’s balance sheet, the rapid redeployment of reserves into making loans may accelerate inflation. Right now, the banks are more concerned with shoring up their capital levels than making loans. However, at some point, the banks will increase their lending and private credit expansion will accelerate. Ultimately, inflation is always a monetary phenomenon and an increase in lending will result in an increase in the velocity of money and available dollars in the system.

Employment

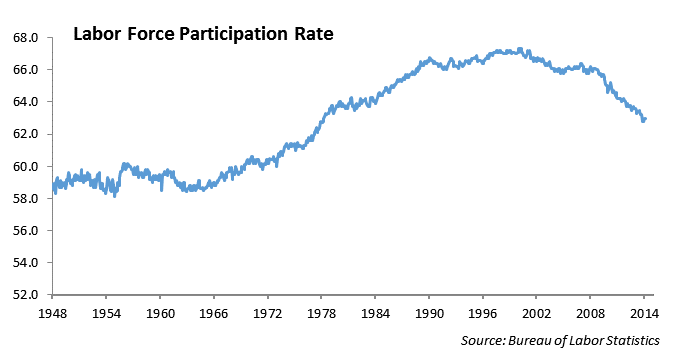

One of the critical elements impacting the economy is the lack of meaningful job growth and corresponding increased wage growth. During the financial crisis, the economy lost over 8 million jobs. Through this past month, the economy has finally produced a cumulative amount of jobs that were displaced during the crisis. However, the numbers do not tell the complete story of how dismal the employment picture is in the United States today. There are serious structural problems in the economy that act to inhibit the growth in quality jobs with an above average level of compensation. The majority of the jobs that are being created are in the retail and service industries which are associated with lower levels of compensation. In addition, a larger portion of the jobs created are considered to be temporary. The employment report from the Bureau of Labor Statistics for March is revealing in this area; of the 192,000 jobs created in the month of March, 15% were classified as temporary. The number of persons employed part time for economic reasons (sometimes referred to as involuntary part-time workers) was little changed at 7.4 million in March. These individuals were working part time because their hours were cut or because they were unable to find full-time work. At the same time, the labor force participation rate (the measure of the labor force as a percent of the population) changed little from prior months at 63.2 percent. The declining trend in the labor force participation rate over the past decade underscores the erosion in job creation in the labor market. We are at levels we haven’t experienced since 1978.

Why the economy is not producing more jobs is a topic being debated by economists and policy makers. Unfortunately, by the time they figure out the answer and develop policy initiatives to help spur hiring, another two years will have passed by. Until we have another election and a new administration, we expect little help from policy makers in Washington DC. In order for the U.S. economy to experience a higher rate of growth, fiscal policy must be aligned with monetary policy and Congress has lacked the political will to initiate fiscal policies that businesses can embrace. We will not experience a sustained economic recovery until we have consistent job growth. Investment Strategy

We expect two things from this earnings season: core earnings will be flat to deteriorating and volatility should increase. We define real earnings as earnings a company would produce without financial gimmicks or manipulation from management. With demand flat, revenue will likely be flat as expense management has been maximized. Companies benefited from the low interest rate environment and refinanced every bit of debt possible, helping to lower interest expense and term out maturities. For the most part, fixed investment and headcount has been flat. In other words, we have seen the best operating margins that Corporate America will be posting. From here on out, increases in costs supporting healthcare and compliance are just the beginning of margin erosion. Last quarter, the consumer discretionary sector was hit hard after the disappointing holiday season, particularly retail. We believe there is value in some of the beaten down stocks including Target and General Motors.

Looking ahead, we expect to see an increase in market volatility as the Fed withdraws its stimulus money and earnings produce challenges for investors. Actual volatility has come in sharply below our projections, which underscores our belief that equity investors have not been adequately compensated for the risk. We believe the volatility has been masked (in both the equity and fixed income markets) by the Federal Reserve’s asset purchase programs which have acted like an anesthetic in the capital markets. The expected increase in volatility may be a welcomed opportunity for investors to average into the equity market.

We have increased our allocation to European equities as the Eurozone economy raises slowly from a severe five year recession. The European Union has cobbled together a central unified bank regulator which will help with investor confidence and credit growth through the region. The primary source of credit to the emerging markets comes from European banks and we expect some improvement in credit flows as a result of improvements in the banking sector. Overall growth in the BRIC countries, which include Brazil, Russia, China and India are showing disappointing economic growth and we see few signs that would change this view near term.

This past quarter, the yield on the ten year U.S. Treasury note declined from a high of 3.0% to a low of 2.6% as a result of the uncertainty caused by Russia’s invasion of Crimea and the perception of an economic slowdown given the harsh winter economic data. Don’t be fooled; most every flight-to-quality rally ends with reversion back to prior levels. We expect interest rates to trend higher over the year and peak near 3.5%. We remain short our duration targets across our fixed income strategies and are overweight the risk sectors in the short to intermediate part of the yield curve. Even though spreads are tight in credit and structured securities, we believe that overweighting the risk sectors in the one to five year duration cells will produce incremental return if spread levels remain constant. The municipal bond sector remains our favorite area for bond investors.

We have been active buyers of Puerto Rico debt that matures before 2017 and is insured by either Assured Guaranty Corporation (AGC) or National Public Finance Corporation (NPF). On March 18, AGC was upgraded to AA from AA- and NPF was upgraded to AA- from A by Standard & Poor’s rating service. Meanwhile, the underlying debt of Puerto Rico was recently downgraded from Baa3/BBB- to Ba2/BB+ in the face of its huge $3.5 billion refinancing.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2014 Winthrop Capital Management