Earnings have been supportive and merger activity has skyrocketed these past couple weeks. Stock markets have remained firm as a result despite money coming out of the previous hot sectors of social media (Amazon) & the biotech industry (despite great fundamentals).

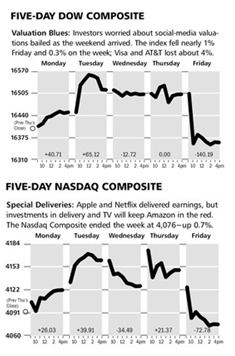

As the charts illustrate, last week was inconclusive overall with both the Dow Jones Industrial Average (led by our shares in Boeing and Caterpillar) and the NASDAQ Composite falling fractionally - although money is really moving around and not out of the stock market.

The Markets & Economy

The macro picture remains the same.

· We have a slow-growth global economy pressured by deflationary concerns in Europe (which will elicit a response from the European Central Bank)

· Combined with geo-political concerns in Europe via Ukraine and in Asia as China continues to press the limits of what it can do in regard to various historical territorial claims.

· This has caused issues in Japan and in South Korea being compounded as the world simply no longer regards the USA as a reliable ally.

In addition, the mid-east peace process (an oxy-moron if I have ever heard one) ended last week when the PLO announced an agreement with Hamas. The latter, of course, is committed to the destruction of Israel. Hard to negotiate under those circumstances. In addition, the Syrian uprising has seen the return of the use of chemical weapons even as Assad has announced his intention to run for a third term. Anyone think that he won’t win? The media refuses to cover this story as our President only wants to talk about such non-issues as raising the minimum wage. It has been many decades since America has appeared to be so inept on the World Stage.

Amazingly, the markets have continued to see this background as being half full. Clearly, concerns about rising interest rates, which exist even to this day, have thrown most investors a curve ball. A slow-growth economy is just what the markets crave and what they are getting. While individual companies may be impacted, the overall market just rotates to the beneficiaries. Thus, energy and its related infrastructure (see Caterpillar comments below) along with utilities have benefitted. Dividend paying companies are similarly being rewarded, and now we have merger mania popping up all over the world but being led by America’s greatest international companies.

This latest trend to merge is a result of two things:

· The slow growth economy is now putting a focus on firms concentrating on their areas of advantage or in creating them. This is what the Pharma industry is now focusing upon (see our comments below).

· This factor is combining with an emphasis on financial engineering due to zero interest rates and few growth opportunities.

· For example Apple last week announced a dividend increase, increased stock buybacks and a 7-for-1 stock split. All in attempt to get shareholders back on board even as the Company’s growth spurt is over for now. It is also the case that Apple split its stock so it could then be placed into the Dow Jones Industrial Average later this year.

Equally important though, and as commented upon this morning by the CEO of Pfizer is that America’s tax code is forcing these deals. American companies have trillions in cash much of which is overseas. A solution to avoid confiscatory taxes and yet to invest the cash is to buy foreign companies with overseas money. This lowers the cost of the transaction to the point that it is compelling.

This is another indication that corporate chieftains do not see organic growth opportunities, but instead see more of the same and thus the focus on financial engineering. This implies cost cutting as well. Of course the biggest costs are employment. So one can see that the politicians have created this slow-growth economy with increasing percentages of people reliant upon a bankrupt government which then spends its time calling for more anti-growth measures such as minimum wage hikes. Companies though will always do what is in their best interests. While this background is good for investors, it is frustrating for society. That is why this country just doesn’t have its confidence back some five years into a recovery.

What to Expect This Week

Two economic reports of consequence. On Wednesday, the estimate of GDP growth for the first quarter will be announced. Currently, the expectation is just above one percent. You heard that correctly. One percent, and yet the media would have you think the economy is doing fine.

Later in the week on Friday will come the April jobs report. With its usual caveats of estimations and revisions, the expectation is for 190,000 non-farm payroll jobs to be created. The weekly low initial jobless claims would imply a better month, but the data on housing and car sales etc… would imply another disappointing month given the strong seasonal adjustments which accompany the number.

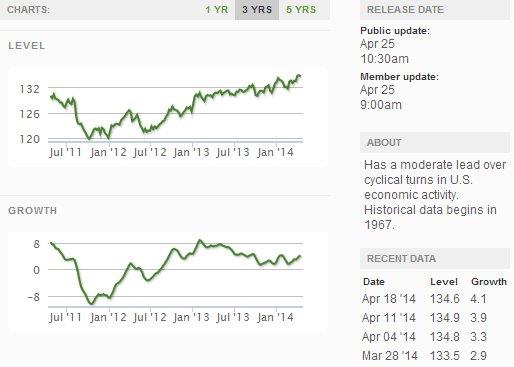

Finally, the weekly look at the Economic Cycle Research Institute leading economic indicators show that the recent uptick (within a flat range) has once again lost some steam. There remains very little to be optimistic about concerning a spurt in economic growth over the remainder of the year. My guess and hope is that by the end of the year the growth rate will have amounted to over 2%, but after the 1st quarter is announced we will need a better pace simply to achieve that.

The pharmaceutical sector was jolted last week as two of our companies, NOVARTIS and GLAXOSMITHKLINE announced they will be exchanging certain assets. NOVARTIS will acquire GLAXO’s oncology products division for $14.5 billion. In exchange, NOVARTIS will divest its Vaccines business to GLAXO for $7.1-billion. The deal is expected to close by the first half of 2015. Separately, NOVARTIS also entered into a definitive agreement with ELI LILLY to divest its Animal Health Division for $5.4 billion. The move will allow NVS to focus on its core portfolio of Pharmaceuticals, eye care and generics. The deal with LLY is also expected to close in the first half of next year.

For GLAXO, its acquisition from NOVARTIS will increase earnings per share, strengthen the Company’s competitive position in growth markets, and reduce the risks in its business. Shares of both companies rose on the news. We will continue to hold both in our portfolios for the foreseeable future.

![]()

SYMBOL: CAT

Shares of CATERPILLAR hit a new 52-week high last week after a strong first-quarter earnings report beat analysts’ expectations. CAT’s profits came in at $1.41 per share, a healthy increase from the $1.31 achieved in the first quarter of 2013. Shares are up more than 16% this year. CAT Chairman & CEO Doug Oberhelman said cutting costs and continued deployment of lean manufacturing initiatives are clearly working. The Company believes construction sales will increase 10% year over year, up from the previous expectation of 5%. CATERPILLAR projects world economic growth to improve from 2% last year to about 3% in 2014. The Company should benefit from an increased share in the Chinese excavator market, recovery in the U.S. construction sector, its cost saving programs and share repurchases.

![]()

SYMBOL: BX

BLACKSTONE GROUP continues to impress. Profits were up +30% for the private equity and real estate giant in the first quarter as the carrying value of its holdings increased and it collected more fees. BLACKSTONE earned $0.70 cents a share, $813 million for the quarter, up from $0.55 cents and $628.2 million a year earlier. The Company says its private-equity funds rose +7% in value in the first three months of the year. BLACKSTONE has been the most active alternative-asset manager so far this year deploying $7.2 billion of equity to transactions. We believe BLACKSTONE is strategically well-positioned to take advantage of a worldwide increase in private-equity deals for the rest of 2014. The Company will pay a $.35 cent dividend on May 5th, a dividend yield of 4.51%.

(c) McIntyre, Freedman, & Flynn