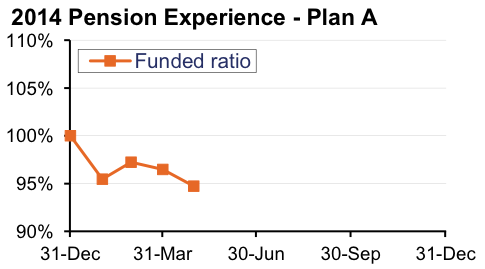

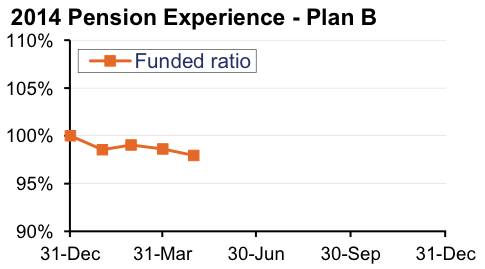

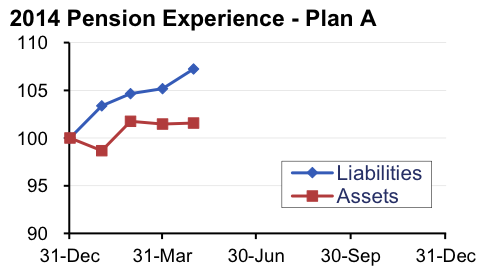

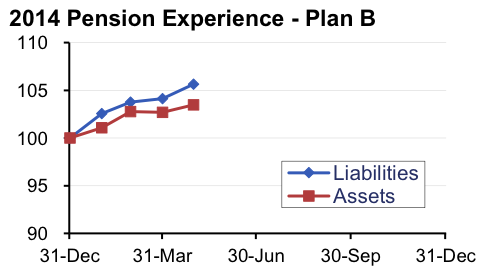

April was another down month for pension sponsors, marked by declining interest rates and sluggish stock markets. Both ‘model’ plans we track [1] lost ground last month, with our traditional ‘Plan A’ losing about 2% and the more conservative ‘Plan B’ dropping less than 1% during April. For the year, sponsors have now given back roughly one-fourth of 2013s ‘bounty’ – Plan A is now down 5% during 2014, and Plan B is down more than 2%.

Assets

For the second straight month, stocks were mixed – large cap and international stocks gained (S&P 500 up almost 1%, overseas EAFE index up almost 2%) while technology and smaller cap stocks fell (NASDAQ down 2%, small-cap Russell 2000 down more than almost 4%).

Year-to-date, the S&P 500 and EAFE are ahead more than 2%, while the NASDAQ has lost more than 1% and the Russell 2000 is down more than 2%.

A diversified stock portfolio was likely flat during April and remains up 1% through four months in 2014.

Interest rates continued their 2014 downward trend, which is good news for bond investors. Both Treasury and corporate bonds both enjoyed gains of almost 1% during April. For the year, bond funds have returned 2%-5%, with long duration bonds seeing the best results.

Overall, our traditional 60/40 portfolio was flat last month and remains 1%-2% ahead for the year, while a conservative 20/80 portfolio added 1% during April and is now up 3%-4% during 2014.

Liabilities

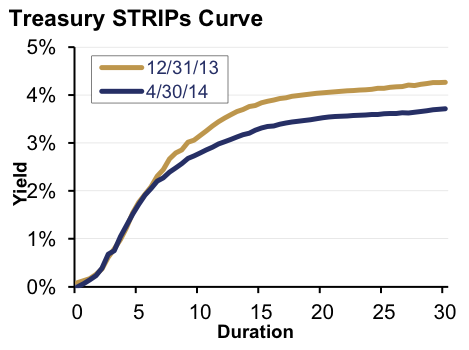

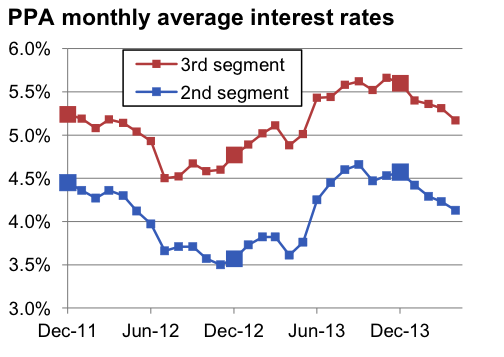

Both funding and accounting liabilities are now driven by market interest rates. The graph on the left compares Treasury STRIPs yields at December 31, 2013, and April 30, 2014, while the graph on the right charts the movement of PPA “2nd and 3rd segment rates” since December 2011 (April 2014 estimated). While these rates don’t strictly meet GAAP measurement requirements, we think they are a very good resource for understanding “rule of thumb” discount rates for plans:

Interest rates declined about 0.1% during April, continuing a ‘flattening’ trend this year that has seen rates drop by almost 0.5%. As the graph above shows, short term (1-5 year) rates are almost unchanged, while long-term (10 year+) rates are down by more than 0.5%. Credit spreads remain stable, so we are seeing similar behavior among corporate bond yields. As a result, pension liabilities increased 1%-2% during April and are now 5%-7% higher than at the end of 2013, with long-duration plans seeing the biggest increases.

Summary

An optimist might feel that pensions have weathered a storm (literally, given the winter) over the past few months. Funded ratios have declined this year, eroding some of the improvement of 2013. But interest rates driven in part by low realized and expected inflation, have pushed back down toward the record lows of 2012, and the stock market appears to be digesting the Fed’s phasing down of bond purchases without a significant correction.

The graphs below summarize the behavior of assets and liabilities for our two model plans so far in 2014:

Looking Ahead

As we discuss in our 2013 article MAP-21 and DB plan finance – Looking ahead to 2014, pension funding requirements over the next few years will not be significantly affected by changes in interest rates. So, from a cash perspective, required contributions for 2014 and 2015 will not be much affected by rate fluctuations.

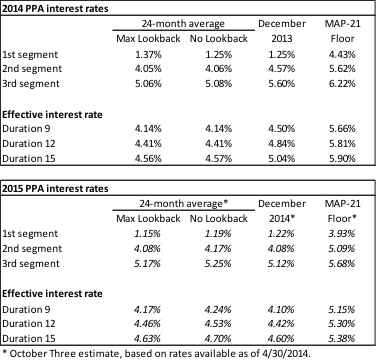

After climbing about 1% in 2013, rates have moved back down about 0.5% so far early 2014. Rates remain low by historical standards, with most sponsors using rates below 5% to measure pension liabilities for accounting purposes.

The table below summarizes rates that plan sponsors are required to use for IRS funding purposes for 2014, along with estimates for 2015. Pre-MAP-21 rates, both 24-month averages and December ‘spot’ rates, which are still required for some calculations, such as PBGC premiums, are also included.

October Three, LLC is a full service actuarial, consulting and technology firm that is a leading force behind the reemergence of defined benefit plans across the country. A primary focus of the consultants at October Three is the design and administration of comprehensive retirement benefits to employees that minimize the financial risks and volatility concerns employers face.

[1] Plan A is a traditional plan (duration 12 at 5.5%) with a 60/40 asset allocation, while Plan B is a cash balance plan (duration 9 at 5.5%) with a 20/80 allocation with a greater emphasis on corporate and long-duration bonds. For both plans, we assume the plan is 100% funded at the beginning of the year and ignore benefit accruals, contributions and benefit payments in order to isolate the financial performance of plan assets versus liabilities.