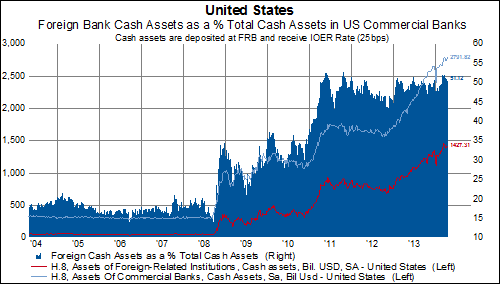

Many are shocked to learn that the Fed's payment of 25bps of interest on excess reserves (a clear banking subsidy) is available to foreign banks, and they have parked substantial sums with the Fed. In the chart below we show the total assets of foreign banks with branches in the US, their cash assets and the percent of assets represented by cash assets. Currently, foreign banks represent 51% of the excess reserves on deposit with the Fed.

To be clear, think of the mechanics this way:

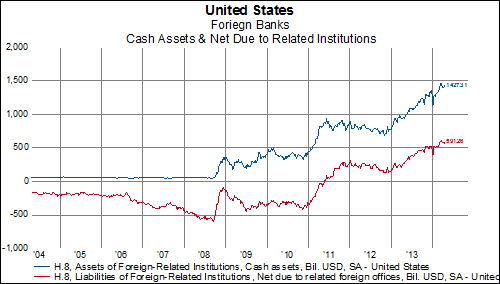

1) BNP in Paris shifts assets to BNP in New York, thereby creating a net debit position from the standpoint of BNP New York.

2) BNP New York takes these deposits and turns around to place them at the Fed to earn 25bps.

There has been an over $1 trillion shift in banking positions in the last six years since the GFC. in 2008, foreign banks had a net debit position vis-a-vis their US branches of around $500 billion. That has since shifted to the point where now foreign banks have a $600 billion credit position vis-a-vis their US branches.

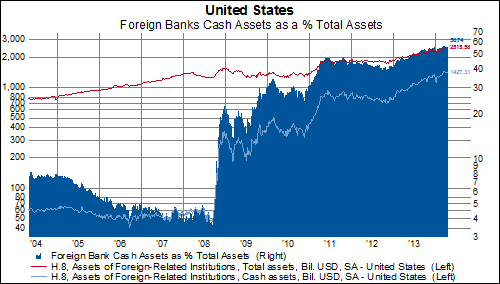

Foreign banks (with US branches) have shifted so much capital to their US branches to take advantage of the 25bps remuneration on excess reserves, that now cash assets are almost 57% of foreign bank assets.

The obvious reason why foreign banks (primarily European) have shifted so much capital to their US branches is because the ECB does not pay any interest on excess reserves.

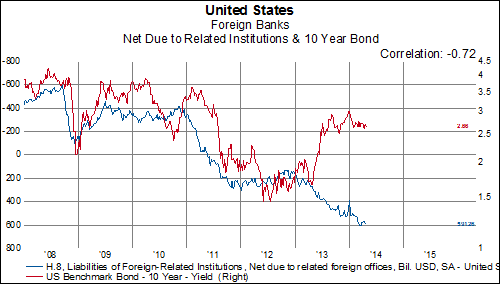

It is interesting to note that this sequence of events has been well correlated with falling US bond rates, though a divergence has appeared over the last year. Foreign banks are continuing to plow capital into their US branches. Will this continued capital shift result in lower bond yields?

(c) GaveKal Capital