Accelerating outflows from bond funds in 2013 highlight investor nervousness over the prospect of rising interest rates. Investors may want to carefully assess the role of fixed-income investments in their portfolios, particularly in light of other types of income-producing vehicles. Upon careful evaluation of their options, investors can make adjustments suitable to their objectives.

Running for the Exits

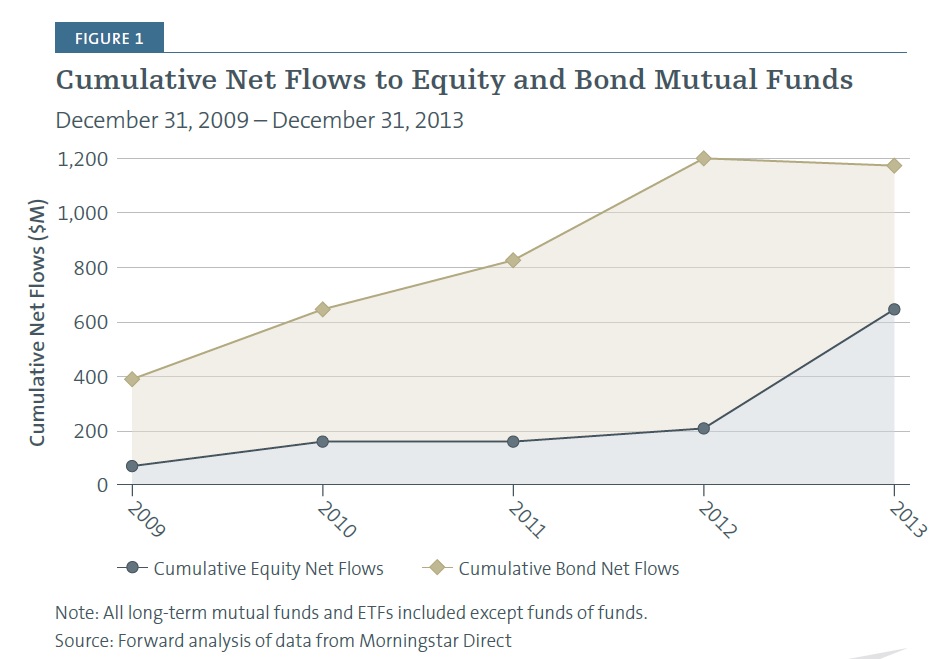

Traumatized by the plummeting equity markets that affected so many portfolios in late 2008 and early 2009, investors widely shunned stock funds in the ensuing years. Many investors moved into what they viewed as “safer” investments such as fixed-income strategies, despite their generally dismal yields. From 2009 through 2012, $1.2 trillion flowed into bond funds, more than four times the $280 billion directed toward equity funds during the same period (Figure 1). 2013 brought a different result as bond funds saw net outflows for the year while equity funds experienced net inflows.

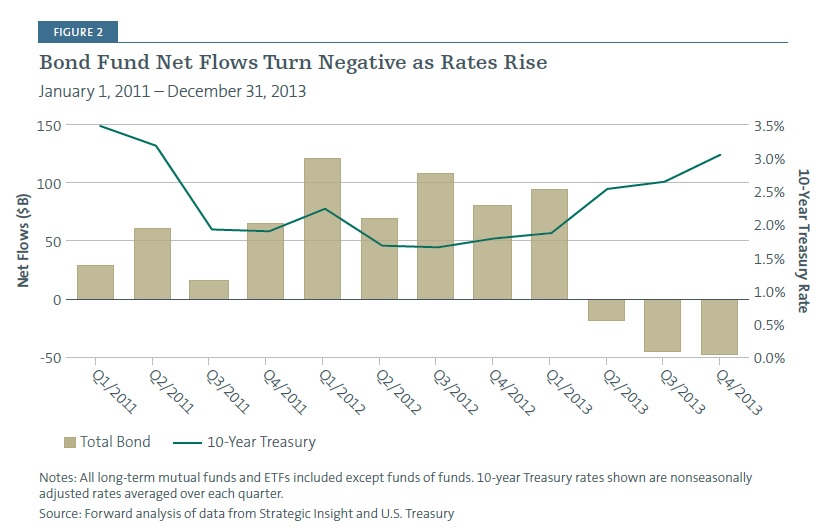

As mentioned previously, more recently, anxiety over the potential of higher interest rates had many bond fund investors heading for the exits as bond funds posted substantial redemptions in the last three quarters of 2013 (Figure 2).

This phenomenon is not new. Bond fund flows have historically been sensitive to changes in interest rates, often falling as rates rise and vice versa. Still, the accelerating pace of redemptions is particularly striking this time around. A reviving economy and statements from the Federal Reserve have many people fearing that rising rates will reduce the value of their fixed-income investments.

Given their unsustainable low levels, we believe it is virtually inevitable that interest rates will rise.

Even a modest increase could have profound effects on bond-heavy portfolios, but the fact remains that nobody knows when, how quickly or to what extent rates will rise. Given this uncertainty, investors and their advisors may want to consider the following steps:

1. Review rationale for holding bonds and expected outcomes

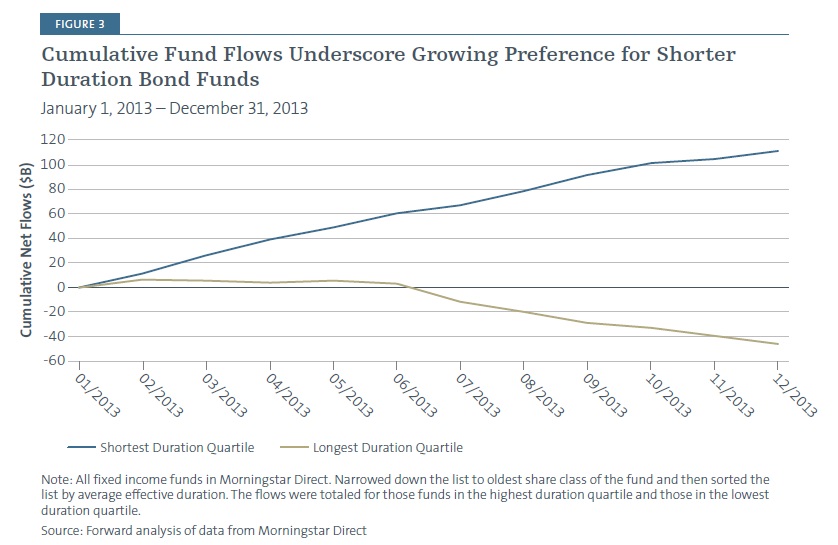

2. Assess how rising rates may affect existing fixed-income investments (Figure 3)

3. Evaluate alternative income-producing investments and how they may perform in a rising rate environment.

4. Select the best income-producing options based on goals and market environment.

Why the Concern?

Interest rates have been kept artificially low by the Fed to help stimulate the U.S. economy. As rates were already low in the aftermath of the recent financial crisis, the Fed more recently pursued a less common form of expansionary policy known as quantitative easing (QE). This bond buying program came in three stages, with the last one (QE3) announced in September 2012. As the economy tentatively grew stronger in 2013, Fed Chairman Ben Bernanke announced in the spring of 2013 that these asset purchases would be scaled back if the recovery continued to gain pace. The prospect of “tapering” had an immediate effect, with U.S. stock markets dropping almost 5% in the week following the announcement.

The Fed has since made it clear that tapering is not imminent, and equity markets recovered and even reached record highs. Fixed-income markets, on the other hand, are in turmoil. As rates fluctuate, bond investors face the very real possibility of interest rates rising above levels to which they’ve become accustomed.

Rates are still extremely low by historical standards, and the Fed is not likely to change its policy until they see signs of strong and sustainable economic growth. Even then, change is likely to come slowly. Nevertheless, investors should be prepared because even a moderate rate increase could significantly erode portfolio performance in coming years. While reallocating away from bonds altogether may be inappropriate, a thoughtful, measured approach may result in a more flexible and durable portfolio that is better positioned to meet performance objectives on a risk-managed basis.

In considering the changing environment, investors should familiarize themselves with other income-producing options available to them, and also understand the risks and what effect they may have on overall portfolio diversification and volatility.

What Are the Options?

Diversify Bond Holdings

Rather than divesting bond holdings, investors may want to shift exposure to other types of fixed-income instruments.

Short duration bonds, for example, have lower interest rate risk relative to traditional bond categories, which can have their principal eroded over a longer period of time by rising rates. Floating rate bonds offer a similar advantage due to the fact that their rates adjust. Yields may be low and credit risk varies, but given recent developments, it is not surprising that recent fund flows indicate a clear and growing preference for shorter duration bond strategies (Figure 3).

High yield bonds are another option that investors may want to consider, particularly in tandem with short-term bonds. High yield bonds offer higher returns and less interest rate risk, while exposing investors to more credit risk. Combined with short duration bonds, an allocation to high yield bonds could theoretically result in a similar level of credit risk as a traditional bond portfolio while maintaining similar returns and a substantially lower level of interest rate risk.

Multisector bond strategies are another option, providing flexibility to investors as they seek to capitalize on differences in relative value among various types of fixed-income securities.

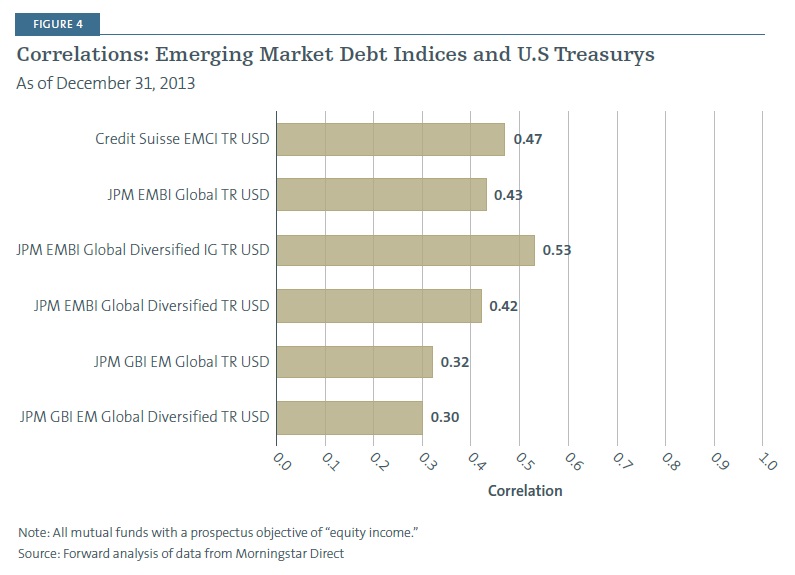

Emerging market debt may be another option for investors concerned about rising interest rates. Global fixed income in general is attractive because diversifying internationally provides exposure to different interest rate and inflation environments, not to mention economic cycles and political situations. Historical returns show that emerging market bond correlations to U.S. interest rates (Figure 4) are attractively low. While attractive for this reason, investors could still worry about credit risk. They may be happy to know that, despite the emerging market corporate default ticking up to 1.43% in 2012 (compared to 1.10% globally), this was only the fourth time in 16 years that the emerging market default rate was higher than the global default rate.1 Meanwhile, yields are comparable, making this a particularly attractive area of diversification for investors focused on income.

Dividend-Paying Stocks

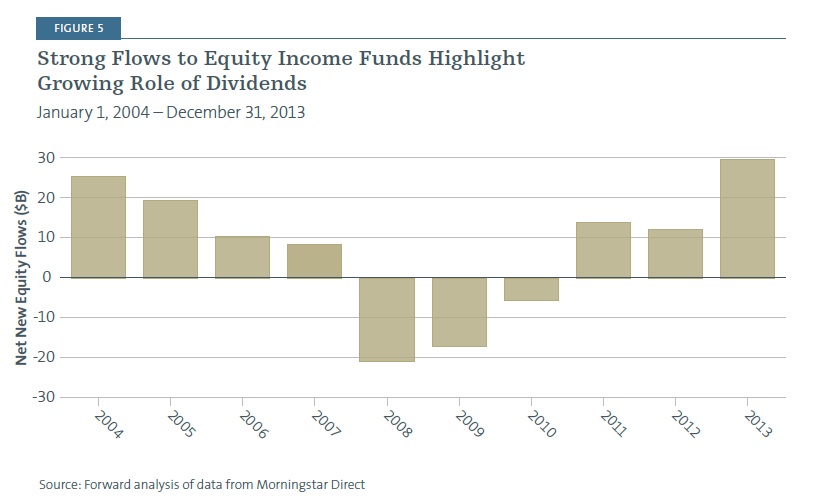

Some of the capital being withdrawn from bond funds has been redeployed into dividend-paying stocks. Strong flows to equity income strategies over the past few years are a testament to their attractiveness (Figure 5), even as flows to other types of equity funds languished. Some investors are willing to take on the additional risk associated with income-producing stocks to capture greater yield at the expense of potential for significant capital appreciation.

Not all dividend strategies are created equal, however, and investors pursuing these strategies will want to proceed with caution. Overly mechanical strategies or a preoccupation with yield rates, for example, may not produce the highest total returns.

Equities in general also bring their own challenges. Capital preservation is not guaranteed, income streams are not necessarily predictable and returns are often more volatile. All of these factors could prove to be incompatible with the objectives of some investors.

Still, there is correlation risk to consider. Bonds have historically demonstrated low correlations to equity returns, making them effective tools to diversify portfolios in order to lower overall risk. If an investor already has significant equity exposure, shifting bond assets to stocks is likely to increase overall portfolio risk. Investors pursuing this strategy will therefore want to pay close attention to the interplay of their equity holdings, aiming to construct a diversified stock portfolio that is less likely to react en masse in the event of a market correction. They will also want to keep in mind which sectors of the equity market are likely to be sensitive to interest rates. Higher rates could, for example, dampen the nascent recovery in the housing and retail sectors.

Hedging Strategies

Both dividend-paying stocks and alternative fixed-income investments are options for investors seeking income. If real income is not a major objective and fixed-income holdings are primarily used as diversification vehicles, investors may want to consider several additional strategies in their quest to reduce their exposure to rising rates.

Real estate investment trusts (REITs) are sometimes thought to be sensitive to interest rates, and their recent performance could be construed as validation for that perspective, with the Dow Jones Equity All REIT Index falling 13.8% from its high in May 2013 to the end of December 2013 while the S&P 500 Index bounced back and posted a 12.2% gain during the same period.2 Appearances can be deceiving. Despite regularly suffering short-term losses in the face of rate increases, REITs have historically exhibited low correlations to both equities and bonds over longer time horizons.3 Their performance is much more likely to be driven by gross domestic product (GDP) growth as well as supply and demand dynamics in the commercial real estate market. In addition to providing a source of less-correlated returns, REITs can generate significant income, as they are required to pay out at least 90% of taxable income as dividends.

Market neutral strategies may be less likely to be viewed as a fixed-income substitute than a way to diversify equity exposure. Many of the same advantages apply, however, making them worthy of consideration. The most obvious benefit of market neutral funds is the fact that they are designed to minimize correlations with the broader equity and fixed-income markets. They also tend to demonstrate risk/reward characteristics similar to fixed income. Most importantly for investors specifically concerned with rising rates is the fact that higher interest rates increase the yield on cash held in market neutral funds, boosting overall returns. Depending on how the investment vehicle is structured, liquidity risk may be a concern for some investors.

Unconstrained strategies are another option in an environment characterized by uncertainty over the timing and extent of rate increases. Managers of these funds can make use of every weapon in their arsenal to seek to deliver absolute returns. Combining a wide variety of bond types with hedging strategies and the skilled application of leverage can potentially drive returns in any market environment. The success of this type of strategy depends entirely on the ability of the manager to implement a repeatable process that incorporates appropriate risk controls. While interest rate risk might effectively be neutralized, unconstrained strategies may be subject to other types of risk, including credit risk, geographic risk and liquidity risk.

Principal protected products may be a good option for investors who are primarily concerned with capital preservation. Subject to the credit risk of the issuer, these funds guarantee a return of at least the principal invested. Often relying heavily on zero-coupon bonds as a means to protecting capital, these funds are very likely to miss out on equity market gains during the investment period. Liquidity is also a potential issue, as these types of structured notes must be held to maturity. Relatively high costs may also erode any potential gains.

Rethinking Portfolio Construction

All of the approaches laid out in this paper are potentially useful strategies for investors seeking to insulate their portfolio from rising rates. In evaluating the best options, investors need to refocus on their investment objectives and determine the specific outcomes they wish to achieve. This may be capital preservation or an ongoing stream of real income, while total returns or liquidity will be a priority for others. The key is to develop a diversification plan that reflects individual goals and can be implemented before interest rates actually rise, at which point it may already be too late. Repositioning your portfolio sooner rather than later could provide the peace of mind of being indifferent to the impact of interest rate changes.

You should consider the investment objectives, risks, charges and expenses of the Forward Funds carefully before investing. A prospectus with this and other information may be obtained by calling (800) 999-6809 or by downloading one from www.forwardinvesting.com. It should be read carefully before investing.

RISKS

There are risks involved with investing, including loss of principal. Past performance does not guarantee future results, share prices will fluctuate and you may have a gain or loss when you redeem shares.

Debt securities are subject to interest rate risk. If interest rates increase, the value of debt securities generally declines. Debt securities with longer durations tend to be more sensitive to changes in interest rates and more volatile than securities with shorter durations.

Alternative strategies typically are subject to increased risk and loss of principal. Consequently, investments such as mutual funds which focus on alternative strategies are not suitable for all investors.

Diversification does not assure profit or protect against risk.

Definition of Terms

Correlation is a statistical measure of how two securities move in relation to each other.

Credit Suisse Emerging Market Corporate Bond Index (EMCI) consists of U.S. dollar-denominated fixed-income issues from Latin America, Eastern Europe and Asia.

Dow Jones Equity All REIT Index represents an index of all publicly traded real estate investment trusts (REITs) in the Dow Jones U.S. stock index classified as an equity REIT. These companies are REITs that primarily own and operate income-producing real estate.

Duration is a measure of the sensitivity of the price of a fixed-income investment to a change in interest rates and is expressed as a number of years.

Interest rate risk is the risk that an investment’s value will change due to a change in interest rates.

J.P. Morgan Emerging Markets Bond Index (EMBI) Global Diversified Investment Grade Total Return represents local bond price return, interest and returnattributable to currency translation to U.S. dollars.

J.P. Morgan Emerging Markets Bond Index (EMBI) Global Diversified Total Return limits the weights of index countries with larger debt issuance by only including a specific portion of the eligible debt outstanding.

J.P. Morgan Emerging Markets Bond Index (EMBI) Global Total Return tracks total returns for USD denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities, including Brady bonds, loans and eurobonds with an outstanding face value of at least $500 million.

J.P. Morgan Global Bond Index (GBI) Emerging Markets Global Diversified Total Return is a comprehensive emerging market debt benchmark that tracks local currency bonds issued by emerging market governments in Asia, Europe, Latin America and the Middle East/Africa. The index consists of regularly traded, fixed-rate, domestic currency government bonds which international investors can readily access.

J.P. Morgan Global Bond Index (GBI) Emerging Markets Global Total Return consists of regularly traded, fixed-rate, domestic currency government bonds. The maximum weight to any country in the index is capped at 10%.

Liquidity risk refers to the risk stemming from the lack of marketability of an investment that cannot be bought or sold quickly enough to prevent or minimize a loss.

Market neutral strategy is a strategy undertaken by an investor or an investment manager that seeks to profit from both increasing and decreasing prices in either a single or numerous markets.

Quantitative easing refers to a form of monetary policy used to stimulate an economy where interest rates are either at, or close to, zero.

S&P 500 Index is an unmanaged index of 500 common stocks chosen to reflect the industries in the U.S. economy.

Volatility is a statistical measure of the dispersion of returns for a given security or market index.

One cannot invest directly in an index.

The new direction of investing

The world has changed, leading investors to seek new strategies that better fit an evolving global climate. Forward’s investment solutions are built around the outcomes we believe investors need to be pursuing – non-correlated return, investment income, global exposure and diversification. With a propensity for unbounded thinking, we focus especially on developing innovative alternative strategies that may help investors build all-weather portfolios. An independent, privately held firm founded in 1998, Forward (Forward Management, LLC) is the advisor to the Forward Funds. As of December 31, 2013, we manage $5.2 billion in a diverse product set offered to individual investors, financial advisors and institutions.

Forward Funds are distributed by Forward Securities, LLC.

Not FDIC Insured. No Bank Guarantee. May Lose Value.

©2014 Forward Management, LLC. All rights reserved.